South East Asia is at the forefront of the digital banking revolution. It all started in 2017 when the Hong Kong Monetary Authority (HKMA) started exploring how to accelerate the development of Fintech companies, especially digital or virtual banks, as they’re called in Hong Kong.

HKMA started granting virtual banking licenses in 2019, and since then, digital banking has begun thriving, not only in Hong Kong but also Singapore, Macau, and the Greater Bay Area.

Since 2016, I’ve researched hundreds of digital, online-only, mobile, and challenger banks (or whatever you want to call them) from the US, UK, EU, Asia, and other parts of the world, and have made a list of the best virtual banks in Hong Kong.

- Best Virtual Bank Overall – ZA Bank

- Best for Everyday Use – Mox

- Best for Savings Accounts – Airstar Bank

- Best for Businesses – Statrys

- Best for Freelancers – Airwallex

- Best for Company Registration – Neat

- Best for Loans – WeLab Bank

- Best for Buy Now, Pay Later – Ant Bank

- Best for Cash Back – livi

- Other Virtual HK Banks

Best Virtual Bank Overall – ZA Bank

| Pros | Cons |

|---|---|

| Personal and business accounts | No joint accounts |

| Savings in 3 currencies HKD, CNY & USD | No autopay |

| Time deposits with a minimum amount of HK$1 | |

| Loans | |

| Open banking | |

| No fees |

ZA Bank is one of the first virtual banks in Hong Kong. It now has more than 600,000 customers and offers a wealth of financial services.

That’s one of the main reasons why I chose ZA as the best bank overall. It simply has more services and products than any other virtual bank in HK right now. It’s a one-stop shop for personal but also for business customers.

HK residents, but also visitors from the mainland can open an account in five minutes. The account comes with a personalized Visa debit card that has discounts, rebates, and draws. You can also withdraw cash fee-free at more than 3,000 ATMs all over Hong Kong.

For international money transfers, ZA has partnered with Wise, the leading global money transfer service. For that reason, transfers are fast and cheap.

Next, there are personal loans of up to HKD1,000,000 with APR as low as 1.80% and extremely fast approval times.

If you have extra money lying around, you can use it to invest with ZA’s fund investment service or put it into multi-currency time deposits from 1 to 12 months.

And lastly, ZA offers all kinds of insurance products ranging from general life insurance to more narrow ones, covering heart attacks and strokes, cancer, or accidents.

Best for Everyday Use – Mox

| Pros | Cons |

|---|---|

| Free ATM withdrawals | Transaction and ATM fees when abroad |

| Unlimited cash back | |

| No monthly fees | |

| Easily flip between credit and debit accounts | |

| Instant loans |

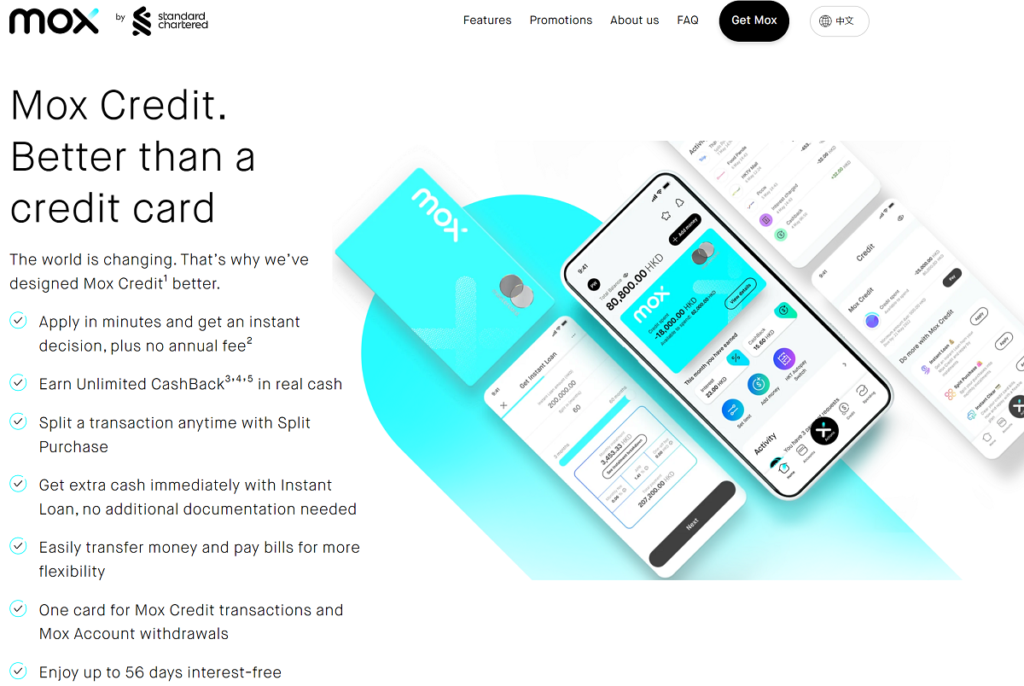

Mox is a digital bank that was launched in 2020 and has some well-known founders and partners. The Bank is a subsidiary of the famed Standard Chartered Bank (Hong Kong) Limited.

Other partners include a well-known telecom (HKT), a lifestyle leader (PCCW), and Asia’s largest online travel agency (Trip.com).

In just two years, the bank managed to get around 400,000 users onboard and still continues to grow strong.

I chose Mox as the best bank for everyday use mostly because it offers an all-in-one bank card. It’s, in fact, Asia’s first numberless card. With this card, you can easily switch between debit and credit spending.

It also comes with 3-5% cashback at selected retailers and 1% everywhere else. Additionally, you can split any Mox Credit purchase of $400 or more and choose between 3 and 60 monthly installments.

When it comes to saving money, there’s a 0.3% p.a. interest rate for regular deposits, 0.01% for foreign currency deposits, and 2.5% – 4.0% for term deposits.

Best for Savings Accounts – Airstar Bank

| Pros | Cons |

|---|---|

| High promotional interest rates | No debit card |

| Fast account opening times | No ATM withdrawals |

| No minimum balance required | Only three currencies supported |

| Personal loans | |

| 24 x 7 HKD & CNY instant transfers |

Airstar is the second virtual bank to be launched successfully in Hong Kong. It’s a joint venture between Xiaomi Corporation, a global IoT leader, and AMTD Group, Asia’s leading comprehensive financial services conglomerate.

These conglomerates decided to focus on savings accounts for both personal and business customers in Hong Kong. They are known for their high-interest rates that are part of continuous promotions developed to acquire more customers for this young startup.

The bank offers a high-interest savings deposit for the first HKD 20,000 saved. It also charges no extra fee for early uplift of time deposits and has a 24/7 FPS instant transfer.

Even though this virtual bank is only a couple of years old, we’re sure that it will grow at a rapid rate as long as they keep luring people with these outstanding and probably unsustainable interest rates.

To open an Airstar personal account, you have to be a non-US Hong Kong tax resident with a Hong Kong ID. And you have to be older than 18.

To open a streamlined corporate account, your company must be small to medium-sized and established in Hong Kong. It has to have less than 50 employees or an annual turnover of less than HKD800 million.

READ ALSO: 6 Best Banks in Qatar (Personal, Business Accounts)

Best for Businesses – Statrys

| Pros | Cons |

|---|---|

| Single and multi-currency accounts | Fee to send local payments |

| Low FX commissions | High fee to collect and send international payment |

| Multilingual client support | |

| Forex for SMEs | |

| Low monthly fee |

Statrys is a virtual bank from Hong Kong founded in 2018 by Bertrand Théaud and focusing on small and medium-sized businesses. You will have to have a business registered in Hong Kong, Singapore, or the British Virgin Islands to apply for an account with Statrys.

It’s easy to open a Statrys account as there are no account opening fees and no minimum deposits.

With this bank, you can open an HK business account that allows you to send, receive, and hold 11 currencies or a EUR IBAN account that lets you make and receive local payments in EUR to and from your European clients.

All customers get a dedicated account manager with multi-lingual support. You can also easily connect your account to marketplaces and payment processors to collect payments in one place.

If you don’t have a company opened in HK yet, Statrys has a service for you. For only HKD6,600, you get the whole package, and a company opened without you lifting a finger. You even get the bank account’s monthly fee waived.

Best for Freelancers – Airwallex

| Pros | Cons |

|---|---|

| No monthly fees | Company cards free, but employee cards $14/m |

| Domestic and foreign currency accounts | |

| Competitive transfer rates | |

| Integrates with global marketplaces | |

| No minimum balance |

Airwallex is a fintech company founded in 2015 in Australia by four Chinese friends Jacob Dai, Jack Zhang, Lucy Yueting Liu, and Max Li.

I found it to be the best for freelancers as it offers a global multi-currency account with the ability to hold more than 40 currencies, which I find really important as freelancers are often dealing with clients from around the world and can lose a lot of money on currency conversion.

Additionally, you get local bank accounts with account details in 12 currencies, including EUR, AUD, USD, GBP, CAD, CNY, and HKD.

To set up a freelance Airwallex account, you’ll have to have the HK Business Registration and your ID. The account is free, and the company card is too.

Airwallex integrates with global online marketplaces like Shopify, eBay, and PayPal, as well as Klarna and Afterpay.

Best for Company Registration – Neat

| Pros | Cons |

|---|---|

| Hassle-free incorporation | High monthly fee |

| Open a company in 15 minutes | No personal accounts anymore |

| Collect payments in multiple currencies | |

| Virtual and physical corporate cards | |

| Xero integration |

Neat has been around since 2015 with offices in Hong Kong and London. It has recently been acquired by Rapyd Financial Network, a global payments platform.

The company has stopped taking personal account applications and is fully focused on bringing the best business banking account for entrepreneurs, SMEs, and ambitious startups.

It’s a one-stop shop for opening a company and getting a bank account with corporate Visa cards.

It takes around 15 minutes to complete the online form, and then you have to wait a couple of days for the process to be finished.

Once the company is opened, you get the Business Registration Certificate, Registered address, and even a Company secretary, all of which are requirements in HK.

Of course, you get a Neat bank account with business cards for free, too.

I love the fact that the bank will automatically renew the Business Registration Certificate every year for me, as well as open, scan, and upload letters that arrive in the mailbox on the same day it is delivered.

Best for Loans – WeLab Bank

| Pros | Cons |

|---|---|

| Free accounts | Out-of-network ATM withdrawals HKD30 |

| Personal loans | |

| Numberless card design | |

| Time deposits with high p.a. | |

| Digital wealth advisory |

WeLab Bank was the fourth virtual bank in Hong Kong to get a license. It was also the first homegrown startup to accomplish this. It offers savings accounts, loans, and term deposits.

I found it to be the best virtual bank for loans. There are two types of loans:

- Personal Instalment Loans

- Debt Consolidation Loans

The Personal Instalment Loan comes with a very low APR and a high cash rebate. The best thing about it, you don’t have to submit any income proof. The whole process is quick and done inside the app.

You can get up to $1,500,000 or up to 18 times your monthly salary. Whichever is lower.

The Debt Consolidation Loan helps you to centralize your card debts and loan balances so you can pay off the debt in one payment. This way, you’re actually saving money as you’re paying less money for all the interest rates.

With this loan, you can save up to 97% of the interest expense and shorten the repayment period by a whopping 91%.

Best for Buy Now, Pay Later – Ant Bank

| Pros | Cons |

|---|---|

| No monthly fees | No debit card |

| Links to AlipayHK | Only savings accounts |

| No minimum balance | |

| Buy Now, Pay Later | |

| Personal Revolving Loan |

Ant Bank is part of the Ant Group’s Ant Financial and is one of the top virtual banks on the HK banking scene. The bank is naturally heavily connected to AlipayHK, and its future plans include an expansion into SME accounts.

It also works best if you already have and use AlipayHK. It integrates with your account through Ant Bank’s app, and you can use your funds in the bank account to spend on anything from clothes and entertainment to electronics.

However, I find Ant Bank to be the best for Buy Now, Pay Later in Hong Kong. You get this service for free, including interest-free installments, a revolving credit line, and a fast application turnaround time.

Best for Cash Back – livi

| Pros | Cons |

|---|---|

| No monthly fees | Can be difficult to verify account |

| Buy Now, Pay Later | No physical card |

| Personal loans | No ATM withdrawals |

| QR payments | Foreign transaction fee |

Livi bank is one of eight virtual banks present in the sprawling Hong Kong market. The fintech startup is backed by BOC Hong Kong (Holdings), Jingdong Digits Technology, and the Jardine Matheson Group.

In its short lifespan, livi has managed to attract more than 200,000 customers and over HKD3 billion in deposits. Most of its customers are between 25 and 40 years old, and their oldest one is 91!

By using your livi card, you’ll also be getting cash back on all your purchases. Cashback is composed of 1% cash back on all purchases, and an additional 8% for eligible online purchases will be deposited within the next calendar month.

8% cashback can only get you up to HKD300 per month, and at a 1% rate, you can net up to HKD500 per month.

Other Virtual Banks in Hong Kong

Fusion Bank

- Founded in 2018

- Pay, spend, and transfer funds with FPS

- Savings accounts in HKD, CNY, and USD

- Real-time exchange rates

- Move money directly to Mainland China

- Personal loans

Fusion Bank is another licensed digital bank and as a member of the Deposit Protection Scheme, all eligible deposits are protected for up to HKD 500,000.

It’s notable as the first HK virtual bank to facilitate money transfers to bank accounts in Mainland China, as well as accept funds from around the world through Fusion’s app.

The bank offers personal savings accounts and personal loans, as well as specific and exclusive loans to buy a Tesla.

PAO Bank

- Founded in 2015

- Fast account opening, lending, and FPS

- No minimum balance requirement

- No account maintenance fee

- No hidden charges

Ping An Bank, or PAObank or PAOB for short, got its virtual banking license in May 2019. The bank offers not only personal but also SME accounts and savings accounts. The accounts are free with no management fees or almost any other fees for that matter.

PAOB savings accounts have a low savings interest rate, but time deposit rates are in line with other virtual banks on the market. Regular savings accounts have no minimum deposit, and you can withdraw funds at any time.