Last Updated on June 10, 2026 by TMB

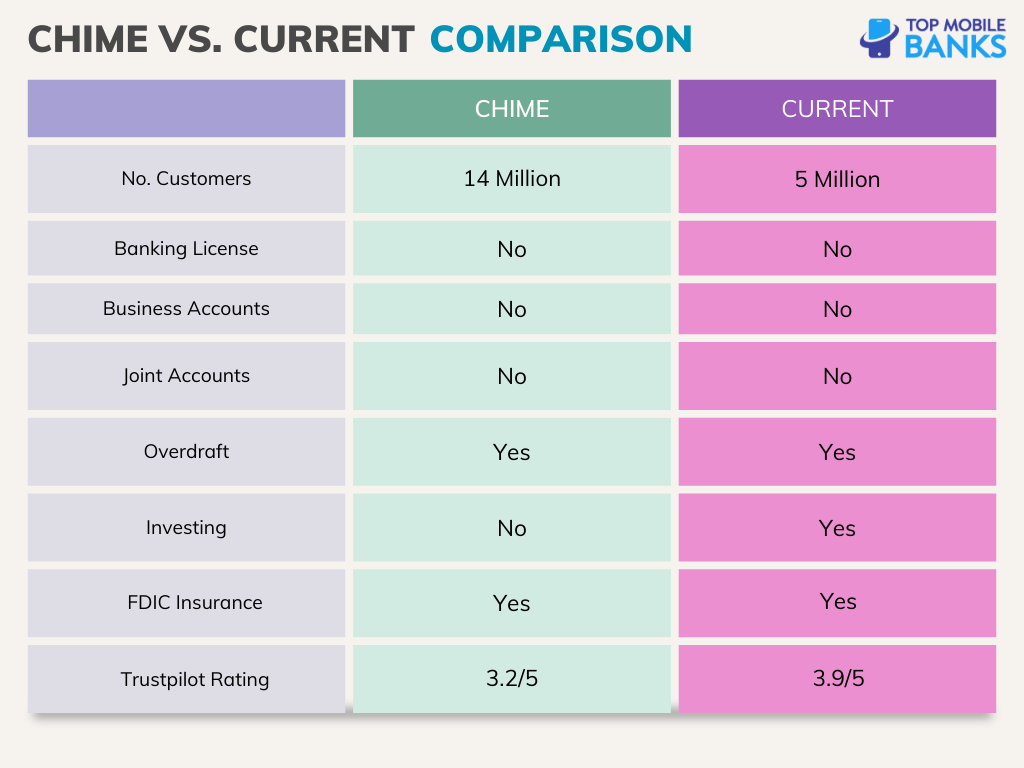

Chime and Current both offer features and benefits that traditional banks don’t, such as getting paid early with a direct deposit, fee-free overdrafts, and the ease of online-only banking overall.

Although both are similar, Current offers a few more features that make it a better digital banking account. Those are the 4.00% APY (versus Chime’s 2.00%), cash back rewards, and teen accounts.

Chime also has features that Current does not, like the Credit Builder account.

Also, keep in mind that both fintech companies are in the active stage of development. So their product offering is likely to expand.

[lasso rel=”pxf” id=”10713″]

About Chime

Chime is a fintech company from San Francisco that was founded in 2013 by Ryan King and Chris Britt. Its partner banks are The Bancorp Bank, N.A. and Stride Bank, N.A., both Members FDIC.

The company has received funding to the tune of $2.3 billion from 31 investors, including Tiger Global Management, Sequoia Capital, SoftBank Vision Fund, General Atlantic,

DST Global, and many other heavy hitters.

How to Open a Chime Account

To open a Chime account, head over to their website or download the Chime app on the Apple App Store or Google Play Store.

All you need is to be older than 18, have a US residential address, a Social Security Number, and a smartphone.

READ ALSO: 6 Payday Loans Apps that Accept Chime (How to Get)

About Current

Current was founded in 2015 in the Greater New York area by Stuart Sopp, who is still the company’s CEO.

The fintech challenger bank has raised more than $402 million in funding from 19 investors, including Tiger Global Management, Andreessen Horowitz, Elizabeth Street Ventures, Expa, and others. It now has between four and five million customers.

Because Current is a fintech and not a bank, it had to partner with a traditional bank – Choice Financial Group, Member FDIC. That means that deposits are also insured through Current’s partner bank.

How to Open a Current Account

To open a Current account, all you need is your US address, Social Security Number, and a smartphone. You also have to be older than 18. Otherwise, your parent or guardian can open an account for you.

You can sign up online or download the app from the Apple App Store or Google Play Store.

Neither of the two apps performs a credit check when you’re opening the account.

Pros & Cons

Pros

| Chime | Current |

| No monthly fees | No monthly fees |

| Early payday | Overdraft Protection up to $200 |

| Overdraft Protection up to $200 | 4.00% APY on Savings Pods |

| Peer-to-peer transfers to anybody | Early payday |

| Fee-free ATMs | FDIC insured up to $250,000 |

| Free debit card replacement | Offers a rewards program with cash back incentives |

| 2.00% APY on savings accounts | Gas hold refunds |

| FDIC insured up to $250,000 | Teen Accounts available |

| Credit Builder Card |

Cons

| Chime | Current |

| Limited services | $5 debit card replacement |

| Limited cash deposit locations | No joint accounts |

| No joint accounts |

READ NEXT: Chime Vs. Aspiration (Choosing Digital Banking App)

Fees

| Chime | Current |

| No monthly or annual fees | No monthly or annual fees |

| No minimum balance | No minimum balance |

| Free to open an account | Free to open an account |

| No fee for using debit card | No fee for using debit card |

| 60,000+ fee-free ATMs | 40,000+ fee-free ATMs |

| $2.50 out-of-network ATM fee | $2.50 out-of-network ATM fee |

As you can see, both apps are identical when it comes to main fees; namely, there aren’t any. Current did charge a monthly fee for its Premium account and for Teen accounts, but that is gone now, and all the features are consolidated under free accounts.

Accounts & Cards

Chime

Chime’s main account is a checking account that’s coupled with a Visa debit card. It comes with no monthly maintenance fees and no minimum balance.

Chime also offers a Credit Builder Credit Card, which adds a ton of value to your account. The Credit Builder card is a credit card that has no limit, no fees, and no security deposit. It also does not require a credit check to enroll.

You can transfer money between accounts to fund your credit account and only spend what you have available. Chime holds your money in a secured account for collateral and then uses that account to pay off your balance each month.

The company also reports your paid-off account each month to the three major credit bureaus, which positively impacts your payment history and can help boost your credit score.

Lastly, there’s the high-yield savings account with 2.00% APY without limitations on the interest you earn as long as the account has funds.

Current

Current similarly offers a spending account with a free Visa debit card. The account has no monthly fees, offers faster direct deposits from your employer, cash back, and overdrafts up to $200.

There’s also a free Teen Account that used to cost $36 per year. It has several great features, such as total parental control over spending limits, merchant blocking, and the ability to assign chores to complete.

This feature gives teens financial independence while ensuring their parents can keep them safe and monitor their spending. It’s an excellent feature for families looking to instill responsibility in their younger members.

Current’s overdraft protection program is called Overdrive. You can enable up to $200 of fee-free overdrafts with a qualifying direct deposit of $500 per month.

Credibility & Security

Security is one of the most critical features of any bank. Luckily, government regulations keep us pretty safe. However, we all still need the peace of mind that our money is protected.

In terms of account security, Chime and Current are each just as safe as a traditional bank and will protect your money from a disaster.

Both banks are FDIC-insured up to $250,000.

Both Chime and Current utilize EMV chip technology in their cards to safeguard your transactions and offer instant transaction alerts to your mobile device to keep you informed of all activity on your account.

Finally, both mobile banks utilize modern technology and encryption to protect your information.

READ NEXT: How Does Chime Make Money? | Over $200 Million Revenue

Saving

Both Chime and Current offer the option to put some of your money aside for a rainy day.

Chime

Chime’s Savings Account boasts an interest rate of 2.00%, and there are several ways to move money into your savings account. Within the Chime app, you can manually transfer money between your accounts.

You can also turn on automatic deposits with the option to “Save When I Get Paid.” You can select a dollar amount or percentage of each deposit to automatically divert to your savings account.

This method is an easy, stress-free way to ensure you are saving money without having to remember to make deposits.

Chime also has a Round-Ups feature, which allows you to save money every time you spend. When you swipe your card, Chime will round the final amount up to the next dollar and deposit the change directly into your savings account.

Current

Current’s savings feature is called Savings Pods. These are sort of like micro-savings accounts that you create for specific purposes that offer 4.00% APY on up to $2,000 per pod.

You can create up to three Savings Pods for an upcoming vacation, an emergency fund, a wedding, or anything you might need to set money aside for.

Current’s Savings Pods also allow you to redirect money through an automatic round-ups feature, which works the same way as Chime’s Round-Ups.

RELATED: How to Use Zelle with a Chime Account (Plus Alternative)

Investing

Chime has no investing platform to speak of. On the other hand, Current allows you to buy and sell crypto without trading fees.

You can start investing as little as $1 into 27 of the most popular crypto coins, including Bitcoin, Ethereum, and Dogecoin. Not all coins are available in every state. You can see the coins available to you by tapping the crypto icon in the app.

Why You Should Choose Chime

Overdrafts

Chime’s overdraft protection, called SpotMe, can be enabled with a qualifying direct deposit of at least $200 per month. It offers up to $200 in overdrafts.

Peer-to-Peer Instant Transfers

Chime allows you to search for your friends via their phone number, name, or Chime username. You can send funds instantly from the Chime app. If the recipient is not a Chime member, they can claim the funds using their debit card.

Checkbook

Chime offers a checkbook feature, which allows you to request they mail a paper check to anyone. This option is 100% free to all Chime members, and checks take 3-9 days to reach their recipient.

The checkbook is helpful if you need to pay a bill by check or if you would like to send checks for birthdays, wedding gifts, or any other occasion.

READ NEXT: The 7 Online Banks Like Chime (Chime Bank Alternatives)

Why You Should Choose Current

Rewards

Current offers a rewards system with its free account. The way that it works is by spending money using your Current debit card at participating locations.

There are over 14,000 merchants nationwide who participate in Current’s rewards program. You earn points for every dollar you spend at one of these locations.

You can find offers for points multipliers through the Current app – at times earning up to 15x the rewards points.

You can redeem the points for either cash or other items in the Current Store through the app.

High Yield Savings Account

Current gives all its customers a high yield of 4.00% APY. This rate is higher than most traditional and digital banks. You don’t have to lock in your funds for any period of time, and you can earn this high APY on up to $6,000.

Gas Station Holds Refunds

Current also offers a unique benefit to its account holders. As we all know, when we purchase gas at the pump, the gas station places a hold on our account. They pre-authorize up to $75 of our funds, which can take anywhere from 3-5 days to fall off.

Of course, this can put you in a distressing situation when you need access to your money, but it’s pending in this gas station hold.

Crypto investing

Crypto isn’t everyone’s cup of tea, but if you’re into that, you’ll be happy to know that you can buy and sell 27 cryptocurrencies with no trading fees.