Last Updated on June 7, 2023 by TMB

Digital banking, online banking, mobile banking, and internet banking are all terms used interchangeably in the world of modern banking. These terms confuse many of us — I mean, what’s the difference between digital and online banking anyways?

While they may seem similar, online banking and digital banking have some key differences. First, online banking refers to being able to do your normal in-person banking online while digital banking refers to new features only brought about by the internet.

Banking in person is pretty simple. You may head to your local branch because you need to write a check, open an account, or just check your balance. Online banking refers to these normal, in-person activities and their ability to be done online.

If you check your balance on your banks’ mobile app, or transfer money from your checking account to your savings account, you’re banking online.

Digital banking is a little different. If online banking refers to the capabilities you can normally do in a bank, now being done online, digital banking refers to the capabilities you can’t do in-person.

Banking is expanding more than ever digitally. As an ex-banker, the new features coming out from traditional banks and fintech companies alike amazes me.

When I was a banker, if you wanted to open a new checking account, you’d have to come in person and sit down for an hour-long appointment.

Nowadays, you can complete the entire process from start to finish online.

That’s what digital banking refers to — the new features that improve modern day banking that you can only do from home.

If you’ve sent money to a friend, reordered a debit card all from an app, or used an enhanced ATM, you’ve banked digitally.

I want to touch on mobile banking as well, as that’s a term I’ve heard used interchangeably with digital and online banking as well.

Mobile banking is the simplest of the three, as it mainly refers to the banking you can do on the go.

Mobile banking comes most popularly in the form of mobile bank apps, like an app for Chase Bank or Bank of America.

Their apps were made to give their customers even easier access to their own funds and accounts.

You get the most out of mobile banking through your everyday business: checking balances, going over your transaction history, and sending money between your own accounts are all examples of mobile banking, so long as they’re done on a mobile app.

Differences Between Mobile and Online Banking

There are actually more differences between mobile and online banking than you’d think.

Online banking and mobile banking seem to be relatively similar — offering in-person banking from the comfort of your couch — but they don’t offer the same products or services.

When I worked at Chase Bank, I thought that the Chase Bank Mobile App and Chase.com were the exact same thing. They’re both just versions of Chase’s digital footprint, right?

Wrong.

Chase.com and the app had a lot of the same features, but they also have a lot of key differences.

Sure, you can check your balance on either the Chase mobile app or the website, but did you know the Chase website goes much further into depth about investing and retirement funds?

The Chase mobile app has an investment section, but it’s much less detailed.

When I was at Chase, the only way you could open an account online was through the website.

Nowadays, you can open an entire account from the Chase mobile app too.

Things are changing quickly in both the digital and mobile spaces of online banking.

If you’re waiting for the latest innovation to improve your modern day banking experience, you won’t have to wait too long.

What are Some Examples of Digital Banking?

You can identify digital banking practices pretty easily.

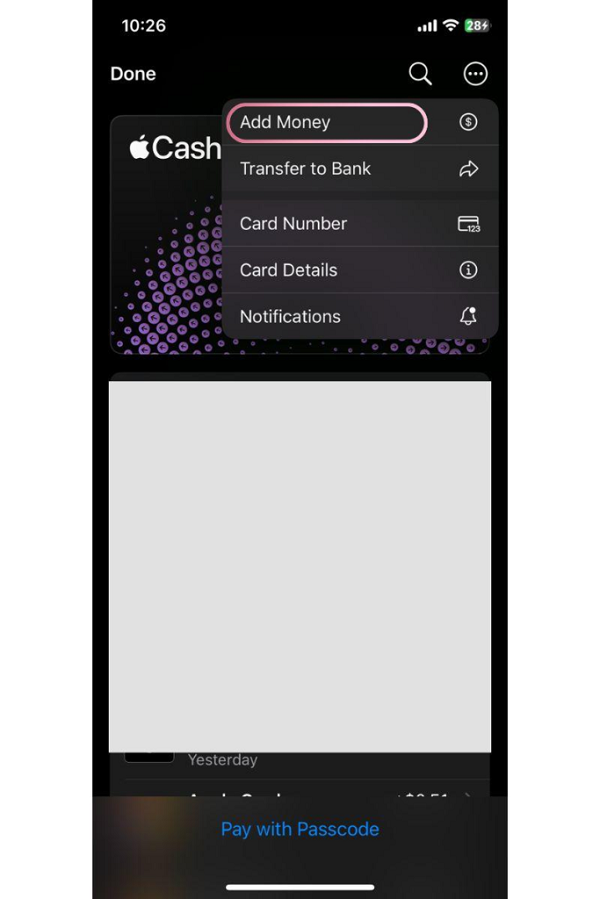

One of the most popular digital banking features to come out in the last couple of years is the digital wallet.

If you have a smartphone, you have a digital wallet. iPhones and Android users alike experience the convenience of digital wallets, either through their Apple Pay or Samsung/ Android Pay apps.

Digital wallets are a personal favorite of mine.

If you’re still unfamiliar, they’re a way to add your debit cards, identification cards, and passes to your phone so you can scan them over contactless card readers rather than using the physical version.

Losing cards is always a problem, especially when they’re easy to lose or very important.

Adding them to your digital wallet means you’ll have a version of them on your mobile device, something we’re all a lot less likely to lose.

Almost everyone accepts digital wallets.

I’ve used mine everywhere from Walmart to the gas station, and more places are adding their capabilities everyday.

I can add money to my balance with the touch of a button too, I’ll include an image below.

Another great example of digital banking is an enhanced ATM.

Most ATMs are simple; they’re designed to accept cash deposits and give out cash when a customer looks to make a withdrawal.

Enhanced ATMs give their users even more options. Once you insert your debit card into an enhanced ATM and enter your PIN, you have access to a whole new host of capabilities.

Sure, as the ATM is still an ATM you can go ahead and grab some cash, and you can now grab the cash in different denominations!

This may not seem like a big deal, but if you wanted to grab some cash 10 years ago it better had been in a denomination of $20.

Other than different bills, enhanced ATMs also give the ability to transfer money between your own accounts and review your recent transactions.

Again, if you wanted to do either of those things 10 years ago, you’d have to sit with a banker or talk to a teller after waiting in line.

Digital banking may be the most innovation banking has seen since the invention of the computer.

There are new changes coming everyday; who knows what digital banking could even look like 10 years from now.

Digital Banking Vs. Traditional Banking

Traditional banking, or heading to your local bank in person, has been the foundation of modern banking for some time.

With the advent of the internet and digital banking, however, its popularity is starting to fall.

I never used to like going to the bank.

When I had just turned 16 years old, I started my very first job at the local creamery.

I got paid by check every two weeks. Whenever I got my check, I dreaded the idea of having to go to the bank just to stand in line and deposit it.

Sure, I could’ve used the ATM but at the end of the day going to the bank is going to the bank, and I wanted no part in it.

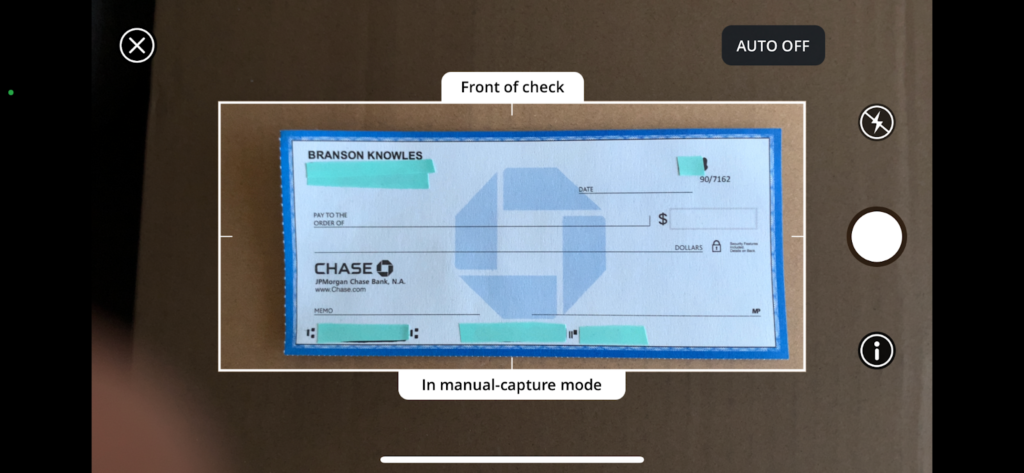

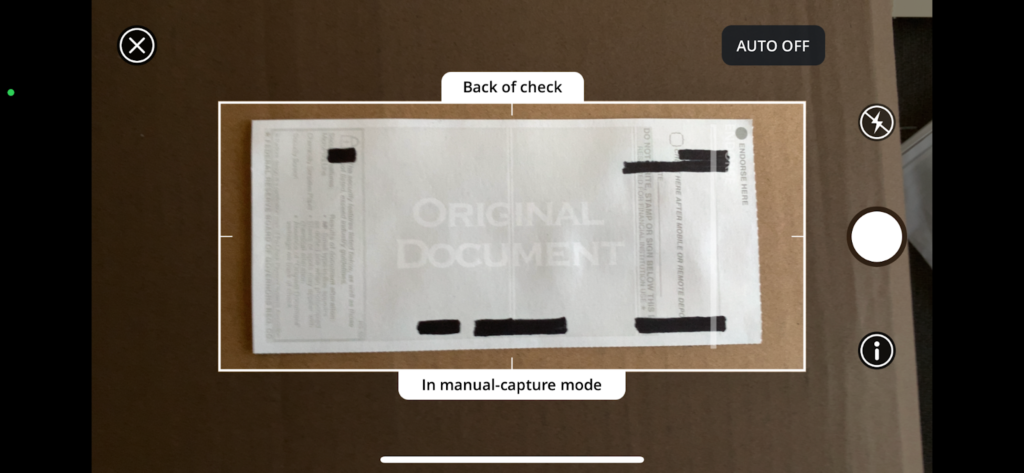

Luckily, I had started my job around the same time Chase had released their mobile check deposit feature, giving customers like me the ability to deposit checks from home!

And that’s exactly what I did.

I never went to the bank to deposit my checks again; the second I would get my paycheck I would run home, sign the back, and take a picture of the front and back of it.

Sure, it took Chase a little more time to process it than if I had gone in person but who cares, I got to save a whole trip to the bank!

If you can’t tell, I’m a huge fan of digital banking.

I love anything that empowers someone to do whatever it is they need on their own. That’s exactly what digital banking is good for; doing things on your own.

Now, while I like to be independent, I will be the first to admit when I need help. And that is the exact reason why traditional banks are here to stay for some time.

When you need help, traditional banks offer you service you just can’t beat over the phone.

Is there anything more frustrating than having a problem, calling customer support, and waiting on hold for hours just to be passed around from customer service rep to customer service rep?

That doesn’t happen when you go to a bank in person. You should be able to see your entire problem resolved from start to finish by the same branch employee.

Bank employees can help you beyond basic issues as well. If you have any questions about the bank’s products or services, bankers and other branch workers are usually some of the best people to ask.

Major banks are changing.

They are moving away from servicing areas to advice centers, hoping to imbue their customers with the confidence they need to do all of their banking on their own, either digitally or just online.

Banks in America only want the highest dollar amount of customers to come to their branches; they want everyone else to use the ATM or to use their mobile app.

If you need help in person though, traditional banking should offer you a branch to head to.

What Are Some of the Benefits of Digital Banking?

Digital banking is pretty new, so you could excuse yourself for not knowing all the ins and outs of it.

If you don’t know though, digital banking can offer you some cool features that once you start using, you won’t be able to imagine how you went without them.

One of the features I use the most when it comes to digital banking is my digital wallet.

I’ve added my most important and most used credit and debit cards to my digital wallet so I never really have to pull out my wallet again.

I almost always have my phone on me and have found it to be way faster to scan my phone over a contactless card reader than to pull out my wallet and insert the chip function on my card.

Adding cards to your digital wallet is a breeze too.

Once the card is added, you can use it forever, or until it expires and you need to get a new card. The feature is entirely free too; Apple doesn’t charge me and neither does my bank.

Another great feature to have come from digital banking is the rising popularity of opening your own account online.

As an ex-banker, opening accounts was my bread and butter. It used to be a long, arduous process that took at least an hour. Now, you can do it in 15 minutes, from home too.

Most banks won’t let you open their most expensive, highest quality accounts on your own, but if you’re just looking for a basic account you should be able to open it by simply heading to your bank’s website.

You might need your basic information but that’s about it. When I was opening accounts, we needed every piece of information we could get from a customer.

Now, requirements to open accounts are much more relaxed no matter where you want to open your account.

While online banks aren’t necessarily digital banks, they did come from it. Online banks are the new wave in modern day banking; an entire bank without a single physical location.

They have incredibly low requirements to open and maintain accounts and some fintech companies, like Cash App, don’t have any requirements to immediately start conducting business. Seriously unheard of stuff.

You can now open and fund an account all without going into a bank.

Fintech companies like Chime will even provide you with an account and routing number the same day you get an account so you can set up direct deposit right away.

They also offer a great savings account and credit builder credit card, gearing themselves up to be the perfect place for anyone new to banking to begin their financial journeys.

I’m a huge fan of digital banking (if me working for a digital banking site wasn’t a good enough clue), and I can’t wait to see what comes out of it over the next couple of years, as what’s already come out in the past couple has been astounding.

Is Digital Banking Safe?

If you know one thing about the internet, it’s that it’s rife with scammers.

There are people pretending to buy your things from online marketplaces, others pretending to be relatives looking to get some money, or the famous Nigerian Prince scam, where someone promises you that if you can send them a small amount of money, they can send you a much larger amount.

If you thought that doing your banking online was irresponsible, I couldn’t blame you too much.

Scammers are running amuck online; who knows how hackers can get into your accounts.

Even with all of that danger, it is safe to bank online, sometimes.

Banks understand that due to their very nature, they have targets on their backs. It’s why they don’t carry as much money in person as they do in the movies, or why some branches have bullet proof glass.

They have a form of bullet proof glass online too.

Banks, fintech companies, and online banks alike all use state of the art, top of the line cybersecurity software to keep their customers and themselves safe.

When I worked at Chase, I remember our app was protected by 128 bit encryption software, an industry leader at the time.

Nowadays, I can only imagine that their security has improved.

Remember when I said it’s not always safe to bank online?

Sometimes, it isn’t, but only in certain scenarios. The only time it’s generally a bad idea to do your banking online is when you’re using public wifi.

If you’re using an unsecured, public network, you can’t know exactly who else is on that network and what they may get from you.

While apps work hard to encrypt all the data you send them and they send you, they can’t get it perfect if someone is hacking your connection.

Hackers and scammers can tap into public wifi and steal your data without you ever knowing.

They could just look like another patron in the coffee shop you’re in, or another shopper at the mall you’re at whose wifi you’re using.

As a rule of thumb, never bank on public wifi. It’s too unsafe and you should always have time to pay your bills or transfer money when you get home and are back on a secure network.