By researching and using dozens and dozens of mobile challenger banks from the US and from around the world, I have come up with a list of the best digital-only banks in the country.

I’ll start with the best banks for each category and mention other notable challenger banks too.

When choosing a mobile, online, digital, challenger, neobank, or however you want to call them, always make sure to check websites such as TrustPilot and the Better Business Bureau to see what the existing users are saying and what are some of the pain points of these banking apps, if any.

- Best for Everyday use – Current

- Best for its Variety of Services – SoFi

- Best for Savings Accounts – Varo

- Best for Convenience – PayPal

- Best for Building Credit Score – Chime

- Best for Casual Use – Cash App

- Best for Metal Cards – Revolut

- Best for International use & Payments – Wise

- Best for Freelancers – Lili

- Best for Startups – Brex

- Best for the Environment – Aspiration

- Best for Social Payments – Venmo

- Best for Crypto Enthusiasts & Cashback – Juno

- Best for Cash Advances – MoneyLion

- Best Digital Wallet – Apple Pay

- More digital banks in the US

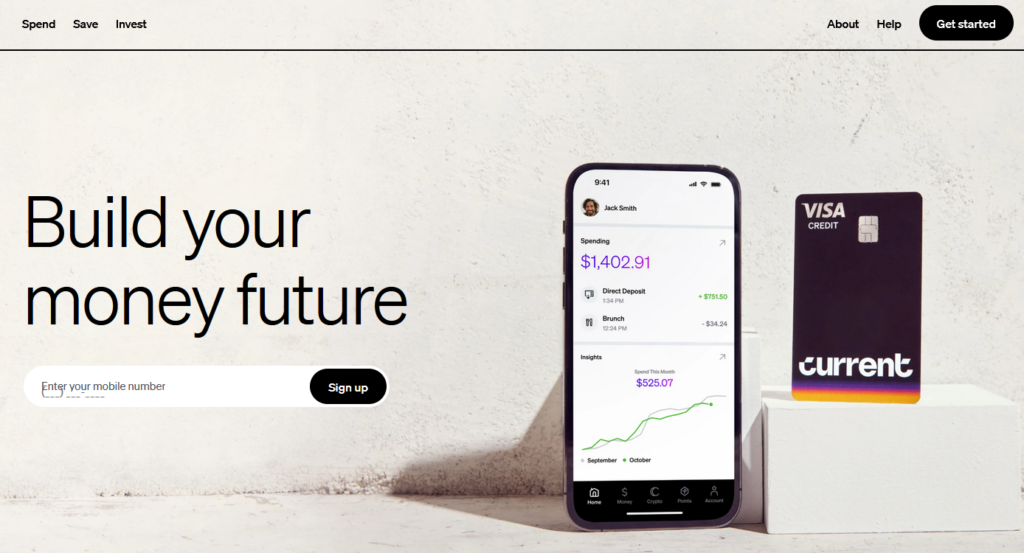

Best Digital Banking Account for Everyday use – Current

| Pros | Cons |

|---|---|

| No monthly fees | $5 card replacement fee |

| Overdraft Protection up to $200 | No joint accounts |

| 4.00% APY on Savings Pods | |

| Rewards program with cash back incentives | |

| Gas hold refunds | |

| Credit building |

Founded more than seven years ago, Current has seen real growth once the company started working with influencers on YouTube and other social media sites.

With more than 5 million customers, Current is one of the biggest payment apps and most popular digital banking accounts in general in the US.

I have reviewed it extensively over the years and found that although its focus is on the younger demographic, the account is actually quite good, and what it does, it does excellent. I now recommend it for everyday use.

For example, I’m sure you know of those annoying gas hold when you’re filling up your car. Current removes them instantly, making all the money available to spend again.

Not only that, but you get to save some money as well with one of the biggest APY interest rates of all banks, period.

If you’re not so good with money and you lose track of your spending, Current has one of the best money tracking and management tools, as well as spending insights right on the app’s homepage.

To open an account, all you need is 5 minutes of your time and your basic details like your name, US address, and Social Security Number. Of course, you’ll need a smartphone. If you’re younger than 18, your parent or guardian can open an account for you.

RELATED: Chime Vs. Current (Similar Accounts With a Few Differences)

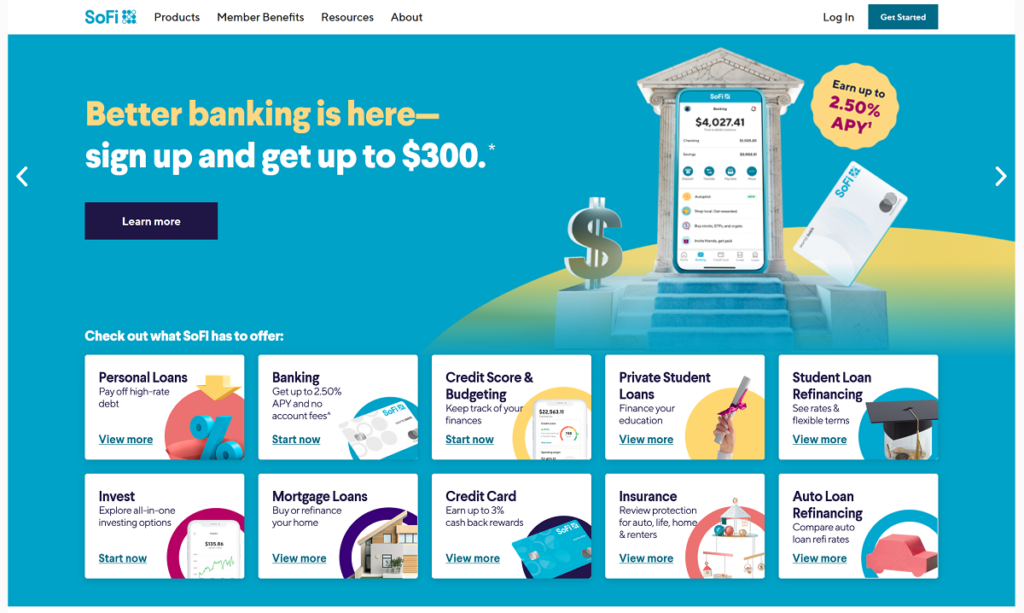

Best Digital Banking Account for its Variety of Services – SoFi

| Pros | Cons |

|---|---|

| No monthly fees | Pricey cash deposits |

| No overdraft fees | No standalone checking and savings accounts |

| Early payday | Highest APY only with direct deposit |

| High APY | |

| Debit and credit cards | |

| Investing | |

| Loans |

SoFi has made a major marketing push in recent years, and it has really paid off for the company as their user base has grown year-on-year. And once you look into their products, it’s easy to see why.

Not only does it have a free account coupled with a free debit card and money transfers, but it has a whole assortment of other financial products such as loans, credit cards, insurance, investments, and more. That’s something that most other digital banks don’t offer.

I love it because it has some of the highest interest rates on your balance, as well as up to 15% cash back at local establishments.

Others might love it because it’s free and offers early payday, no-fee overdrafts, savings vaults, roundups, and more.

But, most importantly, once you sign up for SoFi, you become a member of something bigger because the company organizes in-person and at-home events in which you can participate.

These can be anything from financial webinars and simple social events to career networking. For example, past events have included wine tasting, meditation and yoga, cooking, crafting, and painting, or dinners and happy hours.

Best Digital Banking Account for Savings – Varo

| Pros | Cons |

|---|---|

| No monthly fees | Limits on cash deposits |

| No overdraft or ATM fees | |

| No transfer or debit card replacement fees | |

| Overdraft protection | |

| High-yield savings account | |

| Highly-rated customer service |

Varo has more users than SoFi, Current, and MoneyLion and is notable for being the first digital bank to get a national banking license, thus being able to offer more financial products and services on its own. No need to partner with a traditional bank to offer services anymore.

For now, the bank is focusing on its core products:

- Bank account

- Savings account

- Credit builder program (Varo Believe)

- Cash advances (Varo Advance)

As most other digital banks, Varo is also easy to sign up for as there are no credit checks and you only need to give the most basic information like SSN, name, and address.

Now that it’s a fully-fledged bank, Varo uses Zelle for money transfers, and this works as intended.

Still, what I love the most about Varo, is the high APY that can go up to 5% if you jump through some hoops ($1,000 direct deposits per month and have a positive balance).

With this savings account, customers are allowed up to six withdrawals for every statement cycle to maintain the APY earnings.

Unlike some traditional banks, there is no minimum balance required for a Varo Savings Account. You need just $0.01 to start earning interest.

Varo’s APY is one of the highest of its kind, making this an excellent option for savers who meet the criteria.

READ ALSO: Varo Vs. Chime (Fully-Fledged Bank Vs. Fintech Company)

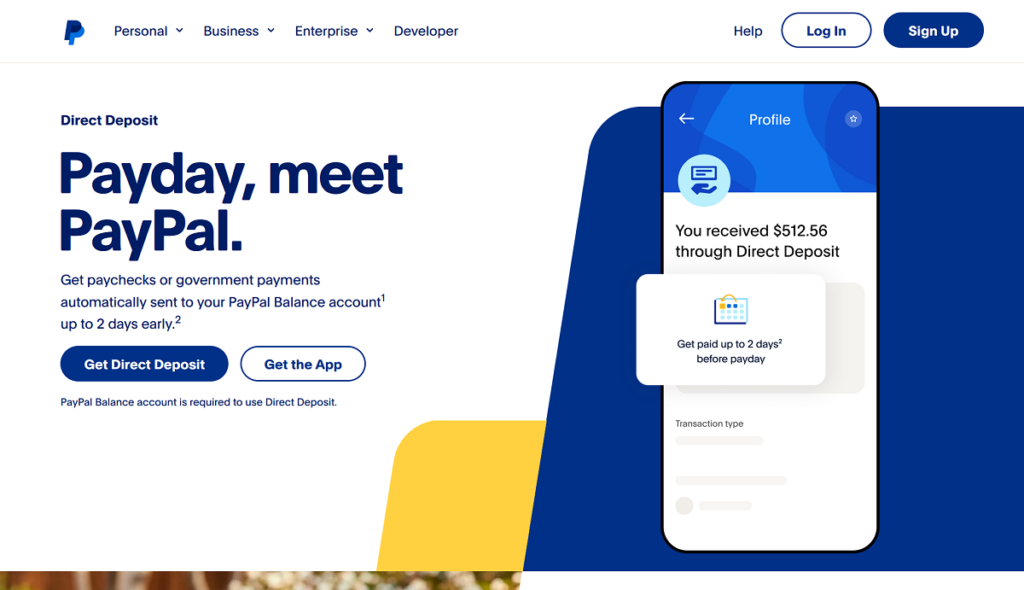

Best Digital Banking Account for Convenience – PayPal

| Pros | Cons |

|---|---|

| Widely accepted | Many fees |

| Free for many domestic transactions | High international costs |

| Convenient and easy to use | Expensive foreign exchange fees |

| Multi-currency accounts available | Some transfers take time |

| Instant credit options | Scammers love it |

| Secure |

What can I say about PayPal that hasn’t been said many times before? The company has been around for around a quarter of a century. After all, you probably have an account and the app installed on your phone.

PayPal is an international powerhouse with around 430 million users and counting! In the US, it offers both personal and business accounts and debit and credit cards, as well as Buy Now, Pay Later. It also offers a high interest rate without fees and minimum balances.

The company also ventured into the crypto market and offers a platform to buy and sell Bitcoin, Bitcoin Cash, Ethereum, and Litecoin.

And even though PayPal is so international, it’s not inherently great for travelers because of its high foreign transaction and exchange fees as well as out-of-network ATM fees.

But if you’re going to use it for shopping in the States, it’s still one of the best options.

Best Digital Banking Account for Building Credit Score – Chime

| Pros | Cons |

|---|---|

| No monthly fees | Limited features |

| Overdraft protection up to $200 | Limited cash deposit locations |

| 2.00% APY on savings accounts | No joint accounts |

| Peer-to-peer transfers to anybody | |

| Credit Builder Card |

Chime is one of our favorite digital banking accounts and mobile payment apps and one that we’ve written extensively about. Because it has more than 14 million US customers, it’s one of the top contenders among digital banks.

I love its Pay Anyone feature the most. It’s like having Zelle but much more secure and less prone to scammers and hackers. You can send money to any debit card or bank account for free, no matter if the recipient is a Chime member or not.

Apart from sending money and making payments online and in-store, Chime also offers fee-free overdrafts, a high-yield savings account, free ATM withdrawals at 60,000 ATMs, as well as a free credit builder card.

This secure credit card can help you rebuild your poor credit score without negatively affecting it when signing up.

Chime is perhaps best known for having almost no fees. This makes it easy to do your everyday banking without worrying about the consequences.

RELATED: 10 Biggest Mobile Payment Apps Dominating in the US

Best Digital Banking Account for Casual Use – Cash App

| Pros | Cons |

|---|---|

| No monthly fees | Spending limits |

| No transaction fees | Withdrawal limits |

| No FX fees | Bitcoin fees |

| Free tax returns | Limited functionality |

| Free debit card | Scammers use it |

| Stock and Bitcoin trading |

If you had to guess how many users Cash App had, what would you say? 5 million? 10 million? 15? Try 80+ million! That’s right. There’s almost no person below 35 without a Cash App account.

But what’s so appealing in this app that it’s now one of two or three most popular mobile payment apps and digital banking accounts?

For one, it’s free. It’s also easy to use, and everyone has it installed already, making it extremely easy to split bills or send cash. Additionally, any person above 13 can now have Cash App and a personalized debit card. This includes the UK as well!

Then there’s also the Bitcoin and stock investing side of the app. In recent years we have seen an incredible surge in investing in crypto and fractional shares of companies listed on stock exchanges.

Not only can you invest with as little as $1, but you can sell and transfer stocks and Bitcoin just as easily.

It seems like Block (formerly Square, Cash App’s parent company) nailed the formula and is reaping the benefits. On a year-over-year basis, Cash App’s revenue was actually down 21%, but the gross profit was up 29%!

We’ve written many useful guides about using Cash App:

- 4 Steps to Mobile Deposit a Paper Check on Cash App

- Cash App Bank Name and Address (Direct Deposit Form)

- Don’t Fall for It: The Top 13 Cash App Scams

- 3 Easy Ways to Transfer Money from Chime to Cash App

- How to Transfer Money From Gift Card to Cash App

- 6 Possible Reasons Why Cash App Transfer Failed (How to Fix)

- How to Use and Pay With Cash App Without a Card

Best Digital Banking Account for Metal Cards – Revolut

| Pros | Cons |

|---|---|

| Exclusive 18G solid steel metal card | Expensive |

| High APY | Poor customer support |

| 10 fee-free international transfers per month | No overdraft |

| Purchase protection | No credit cards |

| Travel insurance | |

| Commission-free stock trading | |

| Up to 5 Junior accounts | |

| Free lounge access for 4 people |

UK’s Revolut has made a big splash this side of the Atlantic as well. It’s also one of the pioneers when it comes to metal debit cards.

For a relatively high monthly fee of $16.99, you get plenty of perks. Will they absorb this monthly cost depends mostly on you.

Apart from getting a cool metal card, you’ll get the most out of this account if you’re a frequent traveler, as the perks pertain mostly to domestic and international travel.

To illustrate this, you get free lounge access, lost or damaged baggage protection, trip delay coverage, trip cancelation and interruption protection, and primary accidental medical insurance.

Read Also: Best Metal Cards by Digital Banks

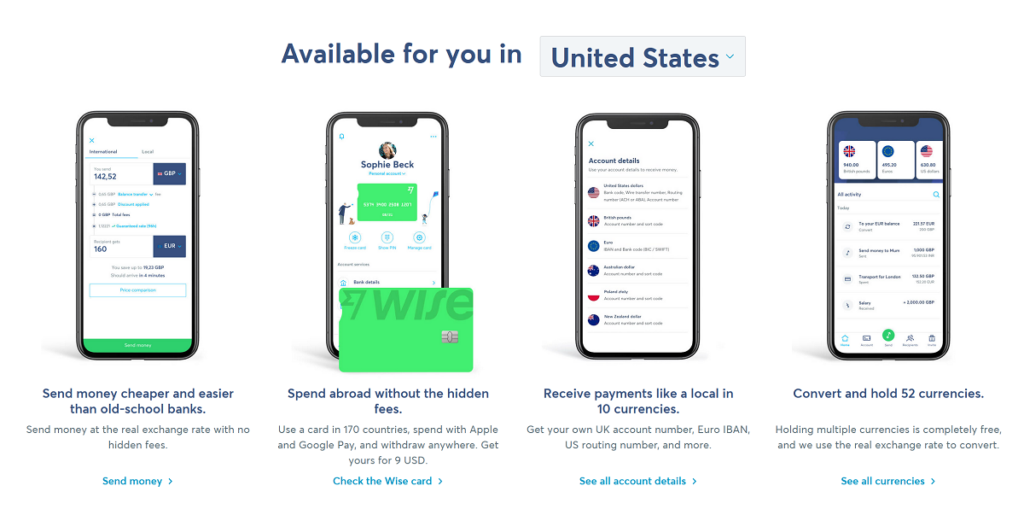

Best Digital Banking Account for International use & Payments – Wise

| Pros | Cons |

|---|---|

| Fees as low as possible | 1%-2% fee for ATM withdrawals above £200/$100/€250 |

| Transparent, cheap, and fast money transfers | Debit card not free and not available in many countries |

| International debit cards available | Deposits not insured (but safeguarded) |

| Spend in any currency | |

| Easy to signup | |

| Great for travelers |

Wise is the best payment app for international transfers. It has an almost cult-like following among frequent travelers, people that are relocating to a different country, and those that are often sending money abroad.

The reasons for that are that you can hold 50 currencies in one account and transfer funds to 175 countries. They also have some of the best foreign transaction fees and a fair exchange rate without hidden fees.

It also has an excellent business account for freelancers, SMEs, and big companies alike. With the advent of e-commerce and sourcing products and services around the world, you can’t afford to lose money on currency conversion.

Wise simply uses the best exchange rate that you can get and adds a really small fee on top. This is in stark contrast to big banks and other money transfer services like PayPal that add a huge markup to their supposedly “free” transfers.

Wise use its technology to link its bank accounts all over the world. In practice, that means that you’re not sending money directly to the recipient but to a Wise account that then transfers money in local currency to its destination.

The sender saves on fees, and the recipient gets the money for free in their local currency.

READ ALSO: 30 Biggest Digital Banks in the World (Customers and Valuation)

Best Digital Banking Account for Freelancers – Lili

| Pros | Cons |

|---|---|

| No monthly fees | Mobile transfer limits |

| One-stop shop for small businesses | Fees for certain features |

| Write-Off Tracker | |

| Invoicing Software | |

| All-inclusive tools for taxes and expenses |

I have to say, I’m impressed with the benefits and features that Lili offers. The free account has features such as essential tax planning tools, an easy “swipe left or right” expense management process, and an extensive ATM network.

Lili has all the tools you’ll need as a freelancer and is an excellent “beginner” program for those looking to get on the right track.

Apart from the simple sign-up process, no hidden fees, and helpful financial resources, there are many other reasons why Lili Bank stands out.

Best Digital Banking Account for Startups – Brex

| Pros | Cons |

|---|---|

| No monthly or annual fee | No Intro APR |

| New cardholder bonus offer | No revolving balances |

| No need for good credit | Convoluted rewards |

| No foreign transaction fees | |

| No need for personal guarantee |

Brex is an incredibly successful digital bank from San Francisco that is focused mostly on startups but also scaled companies, e-commerce businesses, and similar entities. As it’s a startup itself, the firm is incredibly successful in attracting funding.

Its offering includes business accounts, corporate cards, rewards, and, most importantly, venture debt. This product isn’t for everyone, as it was developed for early-stage yet venture-backed tech companies that have a product market fit and a recurring revenue base.

The firm took a big reputation hit in 2022 when it decided to sever itself from tens of thousands of smaller businesses that were its clients as the company started focusing on bigger, venture-backed startups.

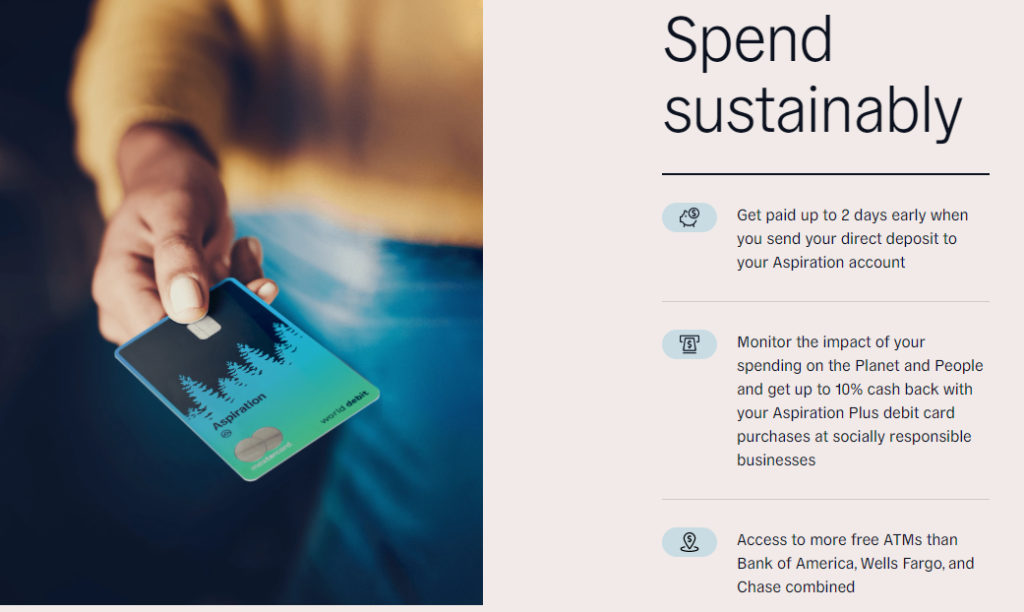

Best Digital Banking Account for the Environment – Aspiration

| Pros | Cons |

|---|---|

| Plant trees by swiping your card | Aspiration Plus has a monthly fee |

| Offset your carbon footprint when buying fuel | $10 account opening fee |

| No money given to fossil fuel projects | Limit of $1,000 for incoming transfers |

| Get up to 5% APY on your savings with Aspiration Plus | Must spend $1,000 minimum monthly on a debit card to earn the APY |

Aspiration stands out from not just other digital banking accounts but all other financial institutions. It has a strong focus on socially and environmentally conscious processes. Aspiration rewards, invests in, and supports businesses and organizations that take care of the planet and don’t invest any money into fossil fuel-related projects and products.

This fintech company offers one free and one paid account. The Spend & Save (or Pay What Is Fair) is a basic and free account. You get to choose your own fee. You can either give no money or, if you think the app and the company deserve something, gives as much or as little as you want.

The account comes with 3-5% cash back on purchases at socially conscious businesses. Aspiration even donates 10 cents of every $1 paid in fees to charities.

The paid premium account is called Aspiration Plus. It costs $7.99 per month but comes with a rewards credit card and a higher yield for savings balance, as well as 10% cash back on purchases at select establishments that focus on planet conservation.

RELATED: Aspiration Vs. Ally Bank (Simpler Vs. Traditional Banking)

Best for Digital Banking Account for Social Payments – Venmo

| Pros | Cons |

|---|---|

| No monthly fees | Public payments by default |

| Free transactions from bank account or debit card | No ability to cancel payments |

| Social element | Scammers love it |

| Instant payments | No international transactions |

| Cashback | No FDIC insurance |

Venmo and Cash App are close competitors. Although Venmo was founded in 2009, the mobile payments app got famous after PayPal acquired it in 2013. The app is now one of the most-used payment platforms, with around 80 million users and counting.

Although Venmo is often “dismissed” as an app for Gen Z, the truth is that all demographics use it, as well as all ethnicities and income levels.

Venmo is most known for its social aspects, where you send money to friends and family and can add a short message coupled with emojis. But the app has transformed far beyond that.

With added features like a Venmo credit card with up to 3% cash back, crypto investing, the ability to pay at major online retailers like Shopify and Amazon, PayPal-like purchase protection, and Venmo business accounts, it is appealing to a wide range of people that are done with traditional banking.

The app is completely free to use except for a 1.75% fee for instant withdrawals, a 3% fee for sending money to other people with your credit card, and small fees for buying and selling crypto.

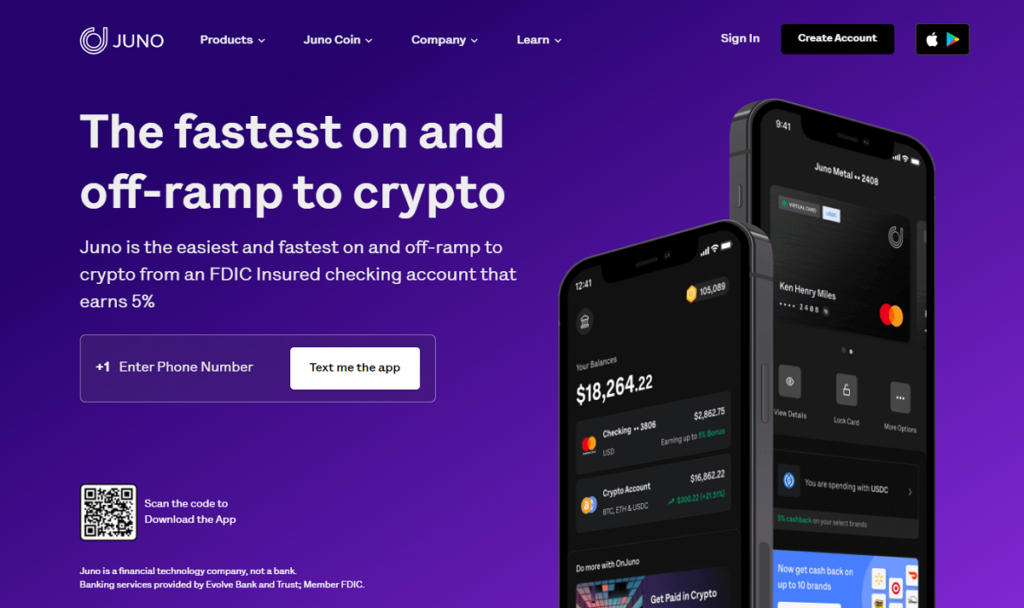

Best Digital Banking Account for Crypto Enthusiasts & Cashback – Juno

| Pros | Cons |

|---|---|

| No monthly service fees | No overdrafts |

| 5% cashback | No joint accounts |

| Easy for immigrants to qualify | Interest compounded monthly, not daily |

| High APY | |

| Crypto friendly | |

| FDIC insured |

Juno is a great neobank that offers excellent APY, no minimum opening deposit, no monthly service fees, and an instant virtual card or a cool black metal card.

It is very crypto-friendly, as you can buy, sell, and cash out very quickly and very easily. I love that you can fund your account with bank transfer, Cash App and Zelle. And use your funds to buy Bitcoin, Ethereum, USDC, and many other cryptos.

I also found it easy to buy NFTs with it. Simply search any NFT collection, such as the popular Bored Apes, Azuki, or Cool Cat, and instantly checkout with no failures.

But I love even more the cashback I got. In fact, the list of brands or merchants on which you get a 5% cashback is extensive, and some of the most popular merchants are on it. Here they are:

- Shopping: Best Buy, Amazon, Target, and The Home Depot

- Subscriptions: Netflix, HBO, Prime Video, Spotify, Apple, Disney Plus

- Health: Headspace, Calm, and Peloton

- Groceries and Health: Trader Joe’s and Patel Brothers

- Food and Drink: Starbucks, Dunkin, Grubhub, Uber Eats, Blue Bottle, Doordash, Postmates, Chick-fil-A, In-N-Out, Wendy’s, and Taco Bell,

- Transportation: Uber, Lyft, Exxon, United Airlines, American Airlines, Chevron, and Shell

- Travel: Airbnb

- Services: Verizon and Xfinity

You can choose any 5 from the list and qualify for the 5% cashback. I’m not going to lie, it’s a difficult choice to choose only five of these.

READ NEXT: 19 Biggest Fintech Companies in the World

Best Digital Banking Account for Cash Advances – MoneyLion

| Pros | Cons |

| Cashbacks and other rewards | $1 monthly fee |

| No-interest cash advances up to $250 | $19.99/m for Credit Builder Plus |

| Fee-free 55,000+ ATMs | |

| Great for beginner investors | |

| Finance tracker | |

| Helps your credit score |

MoneyLion is a popular digital bank that I prefer for cash advances. Cash advances are part of the so-called Instacash program and can be up to $500. This comes without interest, credit checks, or additional monthly fees.

Although you start at only a $25 cash advance, you can unlock higher amounts with recurring deposits but also by signing up for the Credit Builder membership or by completing certain tasks in the App.

If you do all of these, your cash advance will be up to a maximum of $1,000. Alternative cash advance banking apps are also Varo and Chime, as they offer them as well.

Best Digital Wallet – Apple Pay

| Pros | Cons |

|---|---|

| No monthly fees | Works only with Apple devices |

| No transaction fees | Limited features |

| No internet connection required | Instant transfer fee of 1.5% |

| Easy to use with an Apple Watch | |

| Excellent privacy |

If you live in the States, you probably have an iPhone, iPad, iMac, or iWatch. There’s no denying that Apple and its iOS managed to infiltrate the lives of most of us.

Apple Pay is their way of capturing our financial lives as well, as almost 50 million people are projected to use it in 2023.

So, what does Apple Pay do that it’s so popular? First of all, we don’t have to carry our physical cards around anymore or even apply for them in our banks. It’s also an easy way to pay online.

Setup is also incredibly easy if you have iOS, as the app is already on your device. You simply have to take a photo of your bank card, and you’re on your way.

Of course, you can also add your boarding passes, loyalty cards, tickets of all sorts, driver’s licenses, IDs, keys, and more.

Alternatives to Apple Pay are Google Pay and Samsung Pay if you have Android or Samsung devices, respectively.

READ NEXT: Cash App Vs. Apple Pay (There Is a Significant Difference)

Other Notable Digital Banks and Digital Banking Accounts in the US

Axos Bank

- Free to sign up

- Current account

- Savings account

- Business account

- Commercial account

- Mortgages and loans

- Investing

Axos Bank is a pioneer of digital banking as it has been around for more than 20 years already. The bank has low to no fees and offers okay interest rates and easy access to their personal accounts, as well as accounts for SMEs.

Axos is indeed like a traditional bank in digital clothing. But, as they’re mobile-only, you won’t have to pay fees for everything.

Ally Bank

- Free online sign-up

- Checking and Savings accounts

- Stocks & ETFs investing

- Mortgage

- Vehicle financing

- Personal loans

I love Ally for their range of financial products. The bank has been around for a really long time (since 1919) but has transformed into an online-only bank in the last decade.

It’s also renowned for being one of the biggest car finance companies, because it provides car financing and leasing for 4.5 million clients and originates 1.4 million car loans per year.

The bank offers, besides loans, checking and savings accounts, credit cards, investment and savings products, mortgages, and personal loans.

Cheese

- Supports Asian communities and immigrants

- No minimum deposit

- No account maintenance fees

- No transactional fees

- Automatic cashback earnings

- Up to 10% cash back at certain Asian-owned businesses

Cheese offers a simple checking account that is FDIC insured and has no monthly fees or credit checks. Its main feature is the credit builder program that lets you take out a loan of at least $500 with a term length of 12 or 24 months.

I love the app as it is helping Asian communities and has even pledged $100,000 to nonprofits and community service programs in support of Asian neighborhoods and businesses.

Cred.ai

- No fees and interest rates

- The credit card is a solid metal card

- Early access to paycheck

- They have stealth cards for protection

- You can build your credit

- Access to 55,000 free ATMs

Cred is a relatively new digital banking app focusing on Gen Z and Millennials. It’s most notable for black metal credit cards that act as both debit and credit cards.

There are no fees or interest, and you build your credit on autopilot by using the card. If you’re looking for a disruptive bank with the latest technology that comes with a solid metal credit card, cred.ai might be for you. You also won’t pay any fees for all transactions.

Cogni

- Fast online account opening

- Cogni Pay (instant internal transfers)

- Single-Use Cards

- Free ATM withdrawals

- Deposit at stores

Cogni is a fintech that launched the service in March 2020. It offers a people-first service and looks to deliver a bank-level service without the extra costs to its clients.

Cogni is the last-generation of online-only banking solutions that seek to offer flexible, effective, and convenient payments, transfers, and accounts.

Users can perform instant transfers to other Cogni accounts within the app, deposit cash into their account using Visa ReadyLink locations, and even create checks using the digital checkbook service.

Dave

- Up to $500 cash advance

- Credit builder

- Connects to digital banks

- Early payday

- No interest

- No credit check

- FDIC insured

Dave is an extremely popular mobile banking app. I love it because I was able to easily register for its fee-free checking account. In return, it also enables effortless money saving, coupled with budgeting and cash advances.

Of course, as with most similar digital banking apps, you will get paid up to two days early once you set up direct deposits.

Apart from these, Dave is notable for giving up to $500 cash advances that get deposited instantly if you have their checking account too.

And lastly, Dave helps you find side hustles directly from the app allowing you to find flexible and local jobs that suit you.

Majority

- 30-day free trial

- Get paid early

- FDIC insured

- Discounts

- Free phone calls

- Multilanguage live support

Majority is “the first-ever financial membership built by migrants, for migrants.” Founded by Swedes that know how difficult it is to be a migrant in America, this young fintech startup will make waves in the immigrant community.

This fintech company is offering an all-in-one account with banking and, surprisingly, telecommunication in the form of in-app phone calls to cell phones and landlines in 35+ countries.

Majority’s monthly membership fee is $5.99, and you get a Visa debit card for that with local discounts, no minimum balance or deposit requirements, no overdraft or foreign transaction fees, and free international money transfers (that are somewhat limited).

Marcus

- 150 years in the financial business

- No-penalty CD option

- No checking account

- FDIC-secured

- High-yield CDs

- Investing & loans

- Available in the UK

Marcus is a digital bank account from Goldman Sachs. It was created in 2016 and has had good success. Although it lacks a checking account, it offers good savings and investment options, as well as loans and credit cards.

The app also has an investment side to it where you can start investing for as little as $5. I also like their MarcusPay loan service, which acts like Buy Now, Pay Later, and has no fees and a fixed-rate installment plan.

READ ALSO: 10 Biggest Mobile Payment Apps Dominating in the US

Mercury

- Digital banking for startups

- For US registered companies

- No minimum deposit to open an account

- Virtual cards

- Mercury Raise program

- API access

Mercury offers digital banking services aimed at start-ups and tech-based businesses. It has all the usual digital banking services, including a checking account and savings account, various financial tools, and full developer API access to customize their account.

Mercury’s banking model includes that most account transactions are entirely free, so start-ups can focus on building their business.

This no-fee model translates to a physical Mastercard debit card for every user, allowing access to withdraw cash from the Allpoint network of ATMs with no additional transaction fees.

Monzo US

- No monthly minimum deposits

- No account charges

- No overdraft fees

- No Monzo to Monzo fees

- No ATM fees at over 38,000 ATMs nationwide

- No markup on the exchange rate when traveling

- FDIC insured up to $250,000

Monzo is a regulated bank in the UK, but in the US they had to partner with the Ohio-based Sutton Bank that is actually the one that holds Monzo users’ deposits and protects their money with insurance from the Federal Deposit Insurance Corporation (FDIC).

The company offers a dialed-down product here in the form of a checking account and a debit card, with intelligent spending insights that can help you save time and money, in addition to Pots allow you to segment your money.

One

- No monthly fees

- High APY

- Early payday

- No ATM fees

- No minimum deposit

- Savings pockets

- Credit line

One was founded in 2019 by Bill Harris and Brian Hamilton, the company CEO. It is a strong contender in the neobanking world with a simple structure that contains a single account for checking and saving.

You’ll benefit the most with their account if you set up a direct deposit which opens up benefits and raises the limits.

One’s card acts like both a debit card and a credit card. And your One account can therefore give you access to low-cost credit through Credit Line. You can enable it straight from your Spending Pocket.

Oxygen

- Personal and business accounts

- Almost no fees

- Cashback

- Coverage for damage, theft, and more

- 40K+ Fee-free Allpoint network ATMs

Oxygen is one of the newest online-only banking accounts in the US. It was founded in 2020 and offers banking accounts to personal and business customers.

Accounts have four tiers, one of them free. They come with cashback rewards, savings goals, early payday, virtual cards, as well as cell phone and travel insurance, lounge access, Netflix and Peloton reimbursement, and other perks, depending on the tier.

Oxygen can also be helpful if you’re thinking about opening an LLC. It will help you with formatting a company, and any fees for the LLC creation will vary by state and the services you choose.

But in the end, it’s a turn-key service that can save you time and money if you don’t know where to start when trying to start a business.

Payoneer

- Easy to sign up online

- Good choice for SMEs and freelancers

- Free prepaid Mastercard

- Connects to a wide range of marketplaces

- Flexible withdrawal options

- No account fees if used fairly regularly

Payoneer was founded in 2005 by Yuval Tal, who was also the company CEO until 2020 when he stepped down to join an Israeli cyber-security think tank.

The company headquarters are in New York, but they also have 24 offices worldwide. Their team is getting bigger every day, and as of now, it’s 2,000 people big. More than 5 million customers have used Payoneer’s services.

Payoneer has a wide range of payment services and solutions that make it easy to pay and get paid. Unfortunately, this comes at a cost, as some fees can quickly add up and eat a part of your profit.

Quontic

- Free online sign-up

- High APYs on savings accounts

- Bitcoin rewards checking

- Community Development Loans

- Interest compounded daily

- 90k+ ATMs

Quontic Bank has been around since 2009 and is proud to be a Community Development Financial Institution (CDFI) accredited by the US Treasury for its ongoing work on advancing the financial power and stability of low-income people.

It has high-interest savings and checking accounts but also lends to economically disadvantaged people and their communities, as well as gig workers and disenfranchised small business owners.