When we think of digital banking in the UK, we think of the trio – Revolut, Starling, and Monzo. And rightly so, as these three challenger banks have the best apps on the market and offer the most value.

In our book, Starling is a slight winner due to having a simple account structure with no membership for both personal and business accounts. They also have a kids account which is handy for parents. And lastly, no fees at home or abroad for ATM withdrawals.

Monzo is another solid digital bank account with cool-looking cards and a slick app. However, its free account is rather barebones, so if you want more features, you’ll have to upgrade.

The Premium account will set you back £15 per month but in return, you’ll get a metal debit card, phone and travel insurance as well as a higher interest rate.

Let’s dive in deeper and have a closer look at what they have to offer.

| MONZO | STARLING | |

| Customers | 6 million | 3 million |

| Banking Licence | Yes | Yes |

| Business Accounts | Yes | Yes |

| Joint Accounts | Yes | Yes |

| Teen Accounts | Yes (16-17) | Yes (6-16, 16-17) |

| Euro Account | No | Yes |

| Overdraft | Yes | Yes |

| FSCS Insurance | Yes | Yes |

| Trustpilot | 4.4/5 | 4.4/5 |

Monzo and Starling were founded in 2015 and 2014, respectively. Together with Revolut, they led the digital banking revolution in the UK.

And although Monzo managed to acquire double the amount of customers than Starling, The customers have deposited £5 billion less than those at Starling. Total customer deposits at Monzo stand at £4.4bn, and £9.6bn at Starling.

That can only mean that Starling’s customers are indeed treating it as their main bank account, which means they trust it completely.

On the other hand, it seems that many customers are still treating Monzo as their spending account and leaving the bulk of their money in another bank.

Fees

| MONZO | STARLING | |

| Monthly Fee | Free, £5/m, £15/m | Free |

| Business Acc. | Free, £5/m | Free |

| ATM Withdrawals UK | Free | Free |

| Foreign Withdrawals | 3% after £200 | Free |

| Card Delivery | Free | Free |

| International Transfers | 0.35%-2.85% | 0.4% + fixed fee (£0.30 or £5.50) |

Digital banks are rather known for not charging everyday fees. This is the case with these two as well.

You can open an account for free, get a debit card sent to you for free, and withdraw from UK ATMs for free as well.

Accounts & Cards

Starling

Let’s start with Starling. Their award-winning personal account is free. You can open it online or use the Current Account Switch Service for seamless switching from another bank.

The account can be managed online or by using their superb app. I like that you can set up and change everything in the app itself. No need to call or chat with customer support to change your personal details or to open additional accounts.

Speaking of, there are also joint, teen, kids, and Euro accounts. The Mastercard made of recycled plastic is free, and you can order additional ones that are connected to the designated Space in your account.

Lastly, you can deposit cash at Post Offices, deposit cheques with your camera, and earn interest at 0.05% AER up to £85k. There’s also an analytics and budgeting section to see where exactly your money is going and help you save some of it.

Monzo

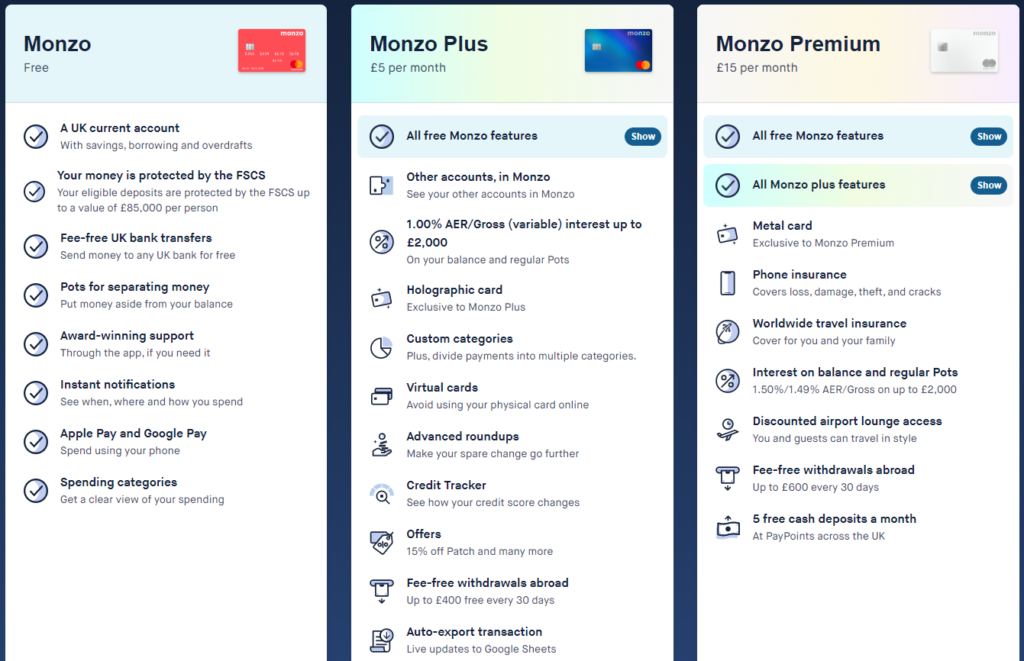

Monzo is much more complicated when it comes to accounts and more in line with Revolut. They have one free and two paid accounts.

The free account comes with a free Mastercard debit card that you can add to Google, Apple, and Samsung Pay, Pots for splitting money, and spending categories.

Monzo Plus (£5/m) allows you to see all your other bank accounts in the app, has a 1.00% AER for up to £2,000, a holographic card, virtual cards for more secure payments, advanced roundups, credit tracker to follow your credit score, discount codes, more fee-free withdrawals, and some other, more or less useful things.

Lastly, Monzo Premium (£15/m) has all the features of the Free and Plus accounts and adds a white metal card, phone and worldwide travel insurance, 1.50% interest rate, up to £600 in fee-free withdrawals per month abroad, discounted lounge access, and 5 free cash deposits per month.

Credibility & Security

Both Monzo and Starling excel in the security of your deposits and their apps’ security. They send you instant notifications for transactions occurring on your account, and you have the option to use fingerprint or PIN logins, as well as Touch and Face ID.

The card control options are all there as well. So, for instance, you can choose whether you want to allow or disable:

- Contactless and chip & pin payments,

- ATM withdrawals,

- Online payments and

- Your mobile wallet.

You can always freeze or cancel your card instantly if you think it might be lost or stolen.

Both banks are completely regulated UK banks that have to follow the same set of rules that high-street banks have to as well, to make sure that your money is 100% safe.

Your deposits are insured and protected for up to £85,000 by the Financial Services Compensation Scheme (FSCS). That means that if the bank goes under, you get all your money (up to £85,000) back. If deposits or savings are in a joint account, the total of FSCS protection doubles to £170,000. This protection is automatic and free.

As you can see, both banks offer safe and sound digital banking platforms in terms of app features and deposit protection.

READ ALSO: 15 Bank Account Scams in 2022 (How to Easily Avoid Them)

Travel

| MONZO | STARLING |

| No ATM fees up to £250/m in EEA and £200/m elsewhere, then 3% fee | No ATM fees |

| No fees for spending money | No fees for spending money |

| Mastercard exchange rate | Mastercard exchange rate |

| No need to inform them | No need to inform them |

The similarities don’t end here, as both Starling and Monzo offer fee-free travel with no spending fees, no fees on top of Mastercard’s exchange rate, and even zero ATM fees. That’s something.

Starling has unlimited free ATM withdrawals, but you can only withdraw up to £300. On the other side, Monzo’s free account doesn’t have free ATM withdrawals abroad, and even its £15/m Premium account has a monthly limit of £600 abroad.

Because Starling doesn’t charge ATM fees, this makes them a slight winner in the travelling comparison.

If you pay the £15 monthly fee for the Monzo Premium account, you get worldwide travel insurance for you and your family and discounted airport lounges, as well as phone insurance. That’s coupled with a metal card as well.

Saving

| MONZO | STARLING |

| Round ups | Round ups |

| Savings Pots | Savings Spaces |

| Savings rate 0%-1.50% AER | Savings rate 0.05% AER |

Starling delivers a slim 0.05% interest rate on their account and up until very recently, they even had a negative interest of -0.5% AER on deposits over €50,000 on your euro account. But that’s been scrapped now.

Neither bank offers a separate savings account, only sub-accounts called Spaces, and Pots, respectively. You can make a separate account by opening a new Saving Space/Pot in the app.

To make the account more personal and motivating, you can add a photo and a name to your Space. Spaces aren’t real savings accounts, and for that reason, your money is always available, and there’s no time limit as to how long the money has to sit in the account.

One can either save on autopilot by rounding up their transactions to the nearest pound or by adding cash manually from the main account.

Monzo’s Pots do the same thing; they collect your spare change, one-off sums, regular payments, and even quirky automated payments like putting a fiver into a Rainy Day Pot every time it gets hotter than 20 degrees.

It really is a shame, then, that Monzo’s free account doesn’t have any interest rates attached to your saving efforts.

Monzo and Starling do basic stuff here with their piggy banks with an abysmal interest rate of only 0.05% from Starling and a non-existing one (in the free account) for Monzo.

Business Account

Again, Starling went with a simple structure of offering one account that’s still comprehensive yet free and intended for sole traders and companies of all sizes.

Their zero-fee policy from the personal account transfers into the business account as well. Starling’s business account is any company’s dream and has all the features that a modern company hopes to have in a bank account.

Included are features such as:

- Integration with popular accounting tools,

- Cash and check deposits,

- Free payments to local and international firms,

- Access for more directors than one,

- Spending analytics,

- Digital receipts

The things that we like the most are the last two as both of these features just make life easier for a business owner.

If you’re in need of overdraft or business or government loans, Starling Bank does offer them. They are available from £25,001 to £250,000, with fixed monthly payments, no fees for early repayments, and terms from 12 to 72 months.

The business account lets you deposit up to £20,000 cash at the Post Office for a 0.3% charge per deposit with a minimum £3 fee, and cheques digitally in-app for free to your business account.

Starling also offers a Business Toolkit that, for only 7£/m, manages your invoices, bills, tax, VAT and more.

Monzo includes free and paid business accounts. For only £5/m, however, you’ll get all of these helpful features:

- Invoicing,

- Multi-user access,

- Virtual cards,

- Integrated accounting,

- Tax pots,

- Exclusive offers,

- Optional 6 months of Xero

There are no overdrafts and loans for businesses are only available through a marketplace. Some people also might find it disappointing that there are no mobile cheque deposits. You can only mail them by post. This isn’t something you’d expect from a digital bank in 2021.

Another concern is that you can deposit only up to £1,000 in cash every six months. If you or your business or trade rely heavily on cash, stay clear.

Monzo’s Business account isn’t bad, it’s just a bit worse than what Starling has to offer. If you need to deposit large sums of cash or want to scan cheques in, via the app conveniently, there is no choice here but to go with Starling or some other bank.

Joint Accounts

Both banks offer joint accounts if both partners have an existing personal account with the bank.

In Monzo’s case, simply head to the settings on the accounts tab and follow the instructions. You can also easily switch your existing joint account from another bank by using the Current Account Switch Service where you’ll be covered by their Switch Guarantee.

Both people will get separate debit cards that are different in design from the personal account cards. In the app, you can see who spent money on what and also set budgets for things like grocery shopping, restaurants, transport, or anything else.

Starling Joint account is equally easy to set up once you both have a Personal Starling account. If the two of you are sitting together, a joint account scanner will quickly locate your partner, and then all they’ll have to do is accept.

There’s nothing else to add here, really, as both banks make it equally easy to apply for their joint accounts, and both offer similar features. Deposits are equally protected by the FSCS.

Junior Accounts

Starling offers two kinds of junior accounts:

- A kids account called Starling Kite

- A teen account

Only parents can open a Kids account. It’s basically a Space in the regular adult account that’s reserved for kids from 6 to 16 years.

Teens, on the other hand, can apply for their Teen account with a smartphone and a passport to verify their identity. It has all the features of an adult account as it’s independent.

Starling’s kids account costs only £2 per month per card. Kids get their own version of the app, too, that’s fantastic for giving kids their pocket money and teaching them good spending habits with all the control in your hands.

Monzo doesn’t have a kids account but offers a personal account for 16 and 17-year-olds that is a fully-fledged banking account that’s missing only two things:

- Overdrafts

- Spending for things that only 18+ can buy or use, like gambling.

Apart from those, it’s a full UK current account with an account number and sort code, so you can send and receive money.

I recently made a comparison of two other popular kids accounts: Revolut Junior Vs. Go Henry (The Best Kids’ Apps)?

Customer Reviews

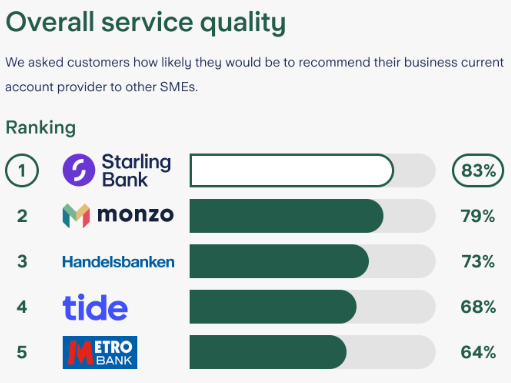

Both Monzo and Starling have the same rating of 4.4/5 stars on Trustpilot. The only difference is the number of reviews. Around 34,000 reviews were written about Starling and around 24,000 for Monzo.

As with any service, there are some disgruntled clients that have issues with the app itself or have not had so good customer service experience.

What is far more worrying is the number of sudden account closures that customers have experienced. It’s probably related to anti-money laundering, and anti-terrorism requirements banks have to implement.

Many of these customers were simply caught in the crosshairs and had their accounts closed by a mistake. That doesn’t make it any better, though, as banks should obviously have better systems in place then.