Opening a business bank account doesn’t have to be a hassle. With digital banks and fintech companies that offer business accounts in the US, you can open an account and start using it in as little as 10 minutes. You only need to provide the most basic documents and information about you and your business or company.

I have used and reviewed hundreds of online, mobile, and digital bank accounts over the years. Both for personal and business use.

So, with this short introduction, let me show you what the best business banking accounts are.

- Best for Freelancers – lili

- Best for Small Businesses – Bluevine

- Best for Web3 Companies – Mercury

- Best for Startups – Brex

- Best for Corporations – Axos Bank

- Best for e-Commerce – Payoneer

- Best for Loans & Non-Profits – LendingClub

- Best for Corporate Cards – Rho

- Best for International Payments – Wise

- Best for Accepting Payments – Square

- Best for Digital Nomads – Wise

- Best for Accounting Tools – Grasshopper

- More Digital Bank Accounts

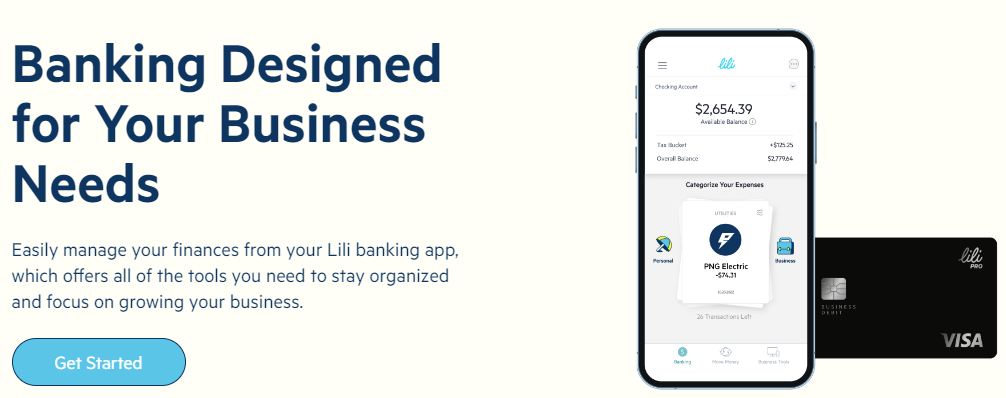

Best for Freelancers – lili

| Pros | Cons |

|---|---|

| No monthly fees | Wire transfers not supported |

| Unlimited and free transactions | Lacking some features |

| Free ATM withdrawals | |

| Integrated tools | |

| Tax optimizer |

lili was designed with freelancers and small business owners in mind. You can do all your banking, invoices, taxes, savings, and more in the lili app. There are no account fees, and you get a Visa debit card, early payment options, and automatic savings.

The free account offers essential tax planning tools, an easy “swipe left or right” expense management process, and an extensive ATM network.

Everyone who’s over 18 and has a valid SSN can open a bank account with lili that won’t affect their credit score.

If you hate fees (who doesn’t), you’ll be happy to know that apart from the free account, there are no foreign transaction fees or even overdraft fees. Plus, lili doesn’t require you to make an initial deposit.

I love organizing my finances neatly, and lili helps me focus on what matters – producing meaningful work and not busywork.

Best for Small Businesses – Bluevine

| Pros | Cons |

|---|---|

| No monthly maintenance fees | No joint accounts |

| No minimum balance or deposit requirements | |

| Multiple accounts for better budgeting | |

| High savings interest rate | |

| Access a revolving line of credit | |

| Streamlined checking, lending, and bill pay |

Bluevine is a digital bank that was founded around ten years ago. In their lifespan, they have helped more than 400,000 businesses with their business checking accounts and loans, among other things.

The fintech company has partnered with Coastal Community Bank, a member of FDIC, to offer fee-free business debit cards.

The account also has a high-yield interest rate for the money you aren’t using at the moment, as well as unlimited transactions, multiple sub-accounts, fee-free ATM withdrawals, and much more.

Bluevine also offers credit lines of up to $250,000 with rates as low as 6.2% and 5-minute decisions.

Best for Web3 Companies – Mercury

| Pros | Cons |

|---|---|

| No monthly fees | Not for freelancers |

| Free wire transfers | No cash deposits |

| Credit cards with cashback | |

| Venture debt & treasury | |

| Lots of experience with startups |

Mercury designed its online banking service for start-ups and tech-based businesses. It was launched in April 2019 by Immad Akhund, Max Tagher, and Jason Zhang and backed by lead investor Andreessen Horowitz.

Not only does this fintech provide checking and savings accounts, but also different financial tools like investing. For instance, Mercury Treasury will put your extra cash into the US Government securities and money market funds for improved yield and security, where you can get a very high-yield APY for your idle money.

After registering an account, each account user gets a physical Mastercard issued, provided they are in the United States. The card usually arrives within 8-10 business days, doesn’t have international transaction fees, and can be connected to Apple Pay.

Mercury also has people that understand how blockchain-based companies work and what they’re looking for in a bank account.

Unlike crypto, both your savings and checking accounts are insured up to $250,000 with FDIC.

Best for Startups – Brex

| Pros | Cons |

|---|---|

| No monthly fees | Only for startups and scaled companies |

| Unlimited and free transfers | |

| Corporate cards with higher credit limits | |

| Financing options | |

| Financial modeling |

Brex was founded in January 2017 and has since become a popular choice for many small businesses, offering them increasing flexibility where other business accounts and credit lines can’t.

Since then, the company pivoted to offer accounts only to VC-funded businesses, aka startups.

They get a free account that has functionalities such as automated invoice and payment processing and spending controls that save time and money.

Every entrepreneur knows that staying on top of your expenses can make or break you; that’s why with Brex, you can track them in real-time and issue cards, track transactions, approve them, or follow up on them.

Brex effortlessly integrates with your accounting tools and makes it easy to automate reconciliation and avoid unnecessary manual work and, therefore, errors.

E-commerce startups earn instant payouts on Amazon, Stripe, Shopify, Square, and other marketplaces and platforms. These payouts can, in fact, boost their Brex credit card limits and offer them to spend their earnings even before they’re deposited into the account.

Best for Corporations – Axos Bank

| Pros | Cons |

|---|---|

| A great choice of accounts | Below average CD rates |

| Desktop and app banking | Bad customer service |

| 90,000 fee-free ATMs across the US | |

| Extensive selection of financial products | |

| Analyzed Business Checking | |

| Commercial Lending |

Axos Bank was launched more than 20 years ago and offers not only small business, but also personal and commercial bank accounts. It’s the closest to traditional banks in terms of financial products on this list of digital banks.

They have two types of checking accounts – Basic and Interest. The Basic checking account has no monthly maintenance fees and gives you 50 checks for free and up to 200 free debit, credit, or deposit items for free. You also get unlimited ATM fee reimbursements and a dedicated relationship manager.

On the other hand, Interest Checking earns you APY and has no monthly maintenance fee if you maintain an average daily balance of at least $5,000. It does have a $100 minimum opening deposit requirement.

Axos also has a range of business savings accounts, certificates of deposit, and commercial lending that includes revolving lines of credit and asset-based lending options.

They’re a good choice for all business owners who are looking for convenient access to their personal, small business, and commercial banking accounts, commercial lending, competitive interest rates, low to no fees, etc.

For corporations, the bank offers industry expertise and custom products, treasury management, IntraFi network deposits, and analyzed business checking accounts, among other things.

Best for e-Commerce – Payoneer

| Pros | Cons |

|---|---|

| No monthly fees | High card transaction fees |

| Easy to open an account online | Strict terms and conditions |

| All significant marketplaces supported | Overeager fraud detecting system |

| Make and receive payments easily |

Payoneer is available in over 200 countries and supports withdrawal to local bank accounts in over 150 countries and currencies.

I’ve used Payoneer for many years without hiccups, and I can recommend it to all e-commerce sellers.

Those sellers that are offering their products on Amazon, or eBay, for instance, profit from getting paid in multiple currencies if needed, but into one account.

This makes it easy and efficient to manage incoming, outgoing, and upcoming payments, withdrawals, POS transactions, and fees. Plus, the integrated Amazon Store Manager lets sellers see the big picture by accruing all Amazon income in one place.

Benefits include the following:

- Receive payments immediately for e-commerce store sales

- Get paid quickly and easily from top e-commerce marketplaces

- Allow vendors that require recurring payments to debit your account automatically

- Track upcoming expenses and view your payment history

- Withdraw your funds to a local bank account

- Pay your suppliers and contractors for free with fast in-network payments

Best for Loans & Non-Profits – Lending Club

| Pros | Cons |

|---|---|

| Monthly fee can be waived | $100 minimum opening deposit |

| Unlimited transactions | |

| Fee-free ATM withdrawals | |

| Unlimited cash back |

Radius has merged with LendingClub, and now the new name is LendingClub. They offer personal, business, and institutional accounts, including lending, savings and checking accounts, and much more.

The bank regularly works with non-profit organizations and has an experienced team of specialists who can provide custom banking solutions to minimize operational risks allowing you to spend more time focusing on the mission.

LendingClub is part of two shared deposit ATM networks – MoneyPass and NYCE. That means you can use any ATM of other partner institutions to make deposits. The good news is that all ATM withdrawal fees are reimbursed at the end of each month.

But, LendingClub works best for small business loans that range from $5,000 – $500,000, commercial real estate financing up to $10 million, and equipment financing from $1 million to $10 million.

Their Marketplace offers plenty of apps that help you automatically save money for any business-related goals, for instance. Then there’s Billshark, the bill-negotiating service that helps you lower your bills to service providers like cable and internet.

If you opt for their small business checking account, you’ll get the ability to make and send professional-looking invoices, real-time transaction alerts, bill payments, mobile check deposits, transfers, wires, etc.

Best for Corporate Cards – Rho

| Pros | Cons |

|---|---|

| No monthly fees | Available to select businesses |

| Free transfers and bill pay | |

| Cash back | |

| Unlimited transactions | |

| Flexible credit limits |

Rho is a modern business bank account that helps entrepreneurs control their spending with state-of-the-art analytics and budgeting tools and charges hardly any fees.

There are no monthly maintenance fees, no ACH fees, no international USD wire fees, bill pays, and additional cards, and users are also free. Foreign transaction fees are among the lowest on the market, only 0.5% for most currencies and 0.75% for Asia-Pacific currencies.

If you need cards for you and your team, Rho can provide free unlimited cards that are either virtual or physical with built-in controls like smart limits and restrictions. The only thing you can’t do is withdraw cash from an ATM, as Rho doesn’t support that yet. But you get cash back.

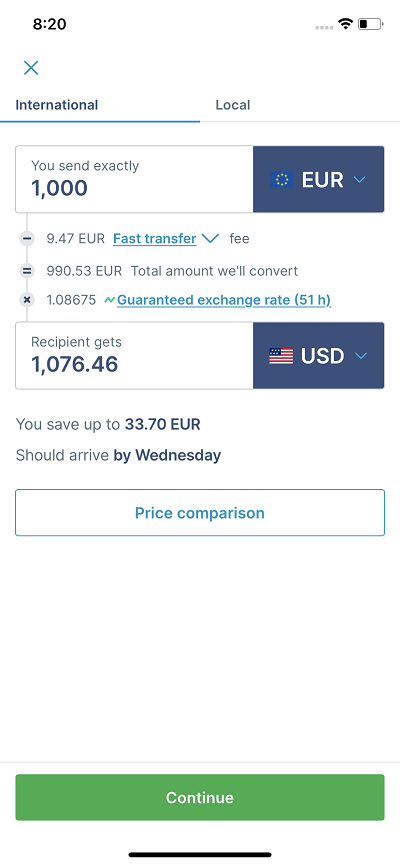

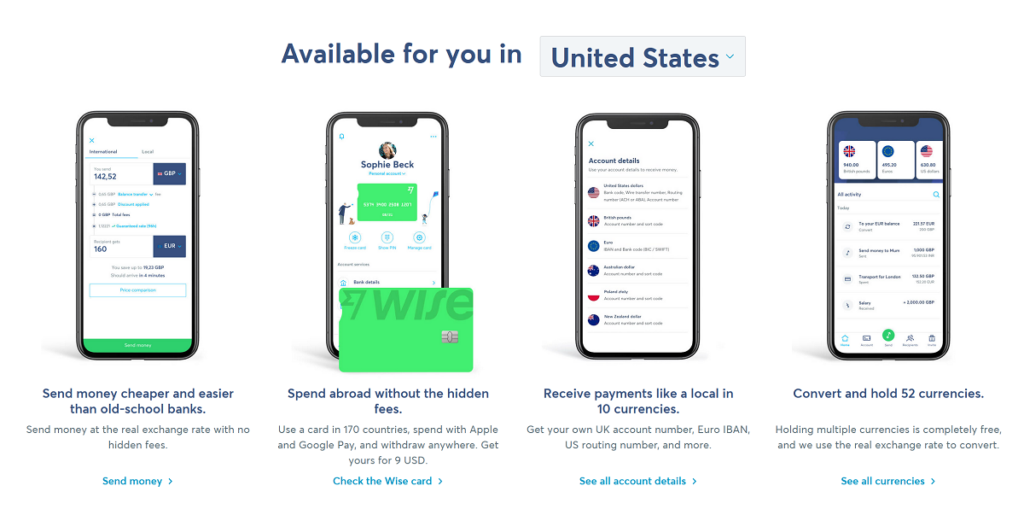

Best for International Payments – Wise

| Pros | Cons |

|---|---|

| No monthly fees | Deposits not insured |

| Transparent money transfers | No cashback |

| Excellent exchange rates | No savings interest rate |

| Easy to sign up | |

| IBAN from 10 different countries | |

| Holds 50+ currencies |

It’s easy to open a Wise account that will offer you plenty of features and benefits no matter if you’re a freelancer or you own a small business.

With Wise, you can make particular payments, recurring ones, and even mass payouts with exceptional rates. By getting a Wise account, you’ll get local bank account details for eight countries, including GBP, EUR, USD, AUD, and others.

You and your team can pay in-store and online without FX fees with virtual and physical debit cards worldwide.

Your business can save a fair amount of money with Wise’s renowned low-fee transfers when you’re paying for contractors, freelancers, or importing goods from overseas.

Best for Accepting Payments – Square

| Pros | Cons |

|---|---|

| POS software and hardware | Add-on services can add up costs |

| Square business card | |

| Lots of add-ons | |

| Low fees | |

| Offline payments | |

| Free magstripe reader |

Square lets you accept payments both in-person and online. You can connect your existing website or set up a free one from scratch.

Customers can also pay you remotely by card or ACH, or you can send them a checkout link over email or text. There are, in total, nine payment methods that you can accept.

Square’s terminal is a sleek-looking piece of hardware that acts as an all-in-one card machine. It will take payments by tapping, inserting, or swiping and can print receipts.

You can accept Apple Pay, Google Pay, other NFC payments, chip cards, and magstripe cards.

Square is a stellar and reliable product for small and medium businesses. With live phone support, a solid app for taking payments, and easy-to-use hardware and peripherals, businesses are flocking to the platform.

Best for Digital Nomads – Wise

Back to Wise. If you’re a digital nomad or you have an international business that includes many currencies or their conversion, I can wholeheartedly recommend Wise.

Digital nomads will appreciate its benefits like the ability to spend abroad like a local, receiving payments from any country in one of your ten different IBAN accounts, holding many different currencies, cheap money transfers, etc.

Both personal and business accounts are available, and both come with debit cards that you can manage from the same app.

You can manage spending, payroll, expenses, and cash flow on the go from virtually any country in the world.

Best for Accounting Tools – Grasshopper

| Pros | Cons |

|---|---|

| No monthly fees | No cash deposits |

| Cash back | $100 minimum opening deposit |

| Earn APY | |

| VC and private equity solutions | |

| Lending |

Grasshopper Bank was founded in 2016 and is said to be the first digital, commercial bank to launch in the US.

The bank has a straightforward, secure, and user-friendly interface that makes it easy to transfer money, approve transactions, add users, and manage their roles and permissions.

It’s primarily designed with small businesses and startups in mind, as well as different lending options like SBA, VC and private equity, commercial real estate, and yacht financing.

I love the account the most for its forecasting tools that let you quickly run if-then scenarios with your business expenses to see the effects on the runway and fundraising needs.

There are also automated bookkeeping, cash flow management, digital invoices, and more.

Besides having hardly any fees, one of the best things about this digital small business bank is that you’ll get a dedicated business banker who will support you in your endeavor.

Other Notable Digital Banks

Apart from the banks I listed above, there are many other digital banks that offer business accounts that are worth mentioning.

Baselane

- No monthly fees

- Designed for landlords and renters

- Bookkeeping and reporting

- Rent collection

- Insurance and loans

Baselane is a free app for managing rental property finances. It’s focused on 11 million independent landlords owning around 20% of the national housing supply.

On one platform, landlords get a high yield and cash back checking account, rent collection on autopilot, cash flow management, automated bookkeeping and reporting, as well as insurance and loans.

Found

- All-in-one banking account

- Integrated financial tools

- Easy sign-up

- No account fees

- Smart tax tools

- Automatic expense tracking

Found is a fintech company specializing in free business accounts and cards for the self-employed. There are no hidden fees or minimum balance requirements, as well as no credit checks when signing up.

Apart from this, you also get free unlimited ACH transfers, and robust tools to help you with your bookkeeping, taxes, and expenses.

You can also link your account to PayPal, Cash App, Venmo, Uber, Stripe, Etsy, Square, and others for quick and easy payments.

Guava

- Business checking account

- By and for Black small business owners

- Connects to Venmo, Etsy, Shopify, Stripe, etc.

- No hidden fees

- No minimum balance required

Guava was founded in 2018 by Kelly Ifill and is a digital banking platform focused Black small business owners.

With it, you get instant access to physical and virtual debit cards, cash flow management tools, connections to payment and selling platforms like Stripe, Venmo, Shopify, and others, as well as access to a community of Black small business owners.

NorthOne

- Free online signup

- No monthly fees

- No minimum balance

- Early paycheck

- Cashback and exclusive discounts

- Instant transfers

NorthOne is a fintech company that was founded in 2016 by Eytan Bensoussan and Justin Adler but launched only in 2019.

It’s trying to fill a gap in the market for high-quality, digital and app-based banking for businesses.

Small businesses and freelancers that need an inexpensive, no-frills bank account with the ability to connect to select accounting, e-commerce, and payment integrations have a solid choice in NorthOne. And the best thing is you can have an account in minutes.

The company partnered with The Bancorp Bank to offer banking services and FDIC deposit protection, as NorthOne doesn’t have a banking license.

Novo

- No monthly maintenance fees

- Easy to apply in under 10 minutes

- ATM fees reimbursed

- $50 initial deposit

- Free ACH transfers

- Supports Wise, Xero, Quickbooks…

- FDIC insured

The Banker magazine named Novo the “Most Innovative Bank in North America” in their 2021 Innovation in Digital Banking Awards.

The company was founded in 2016 by Michael Rangel (CEO) and Tyler McIntyre and has headquarters in New York, but the app was launched in 2018.

It’s a good choice for small businesses and freelancers because you get all the tools that small businesses need with the safety and FDIC insurance of a traditional bank.

For example, there’s a great tool that’s called Novo Reserves which allows users to set money aside in the app for taxes, profit, payroll, and other significant business expenses. This tool is great for budgeting and setting goals for your business.

Although I like the simplicity of the app and the platform as a whole, I’d like to see more options. With Novo being an extension of an already established bank, they only offer one type of account, and that’s their business checking account.

Oxygen

- Cashback on rideshare, gas, and more

- Tag expenses

- Get paid early

- Virtual cards with spending controls

- Business Savings Account

- Form an LLC inside the app

Oxygen was founded in 2018 by Hussein Ahmed and offers a business account for freelancers, sole traders, digital nomads, and small businesses.

There are no transaction fees, no minimum balance or minimum deposit, up to 5% cashback on shipping and gas, for example, but also no monthly or annual fees.

If you or your business have a US address, you are eligible for the Oxygen account. But Oxygen can also help you open an LLC if you need one. You can rush through the incorporation process in the Oxygen app with their turn-key service – wherever you are in the US.

Although Oxygen is not actually a bank, its banking services are provided by The Bancorp Bank, and deposits are insured up to $250,000 by the FDIC.

Relay

- Free and paid accounts

- For small businesses, accountants, and bookkeepers

- No hidden fees

- Free Atm withdrawals

- Free cash deposits

- Xero and Quickbooks integration

Relay is another business banking account that was launched in 2018/2019 with the help of Evolve, Bank & Trust.

It offers free and paid checking accounts that are insured for up to $250,000. In fact, you don’t get just one checking account, but 20 so you can separate your cash in an easy way.

You also get to issue up to 50 debit cards, virtual and physical, with spending limits. And if you pay $30 per month, you get free outgoing wire transfers, auto-import bills, and more.

Revolut

- Multicurrency account

- Free international and local payments

- Real (interbank) exchange rate

- Unlimited accounts

- View and control payments and transfers

- Set spending limits

- Block and freeze cards

- Accept payments on your website

More than 500,000 businesses worldwide already trust Revolut with their business account. And it’s easy to see why. They offer plenty of features that freelancers and small business owners will appreciate.

Apart from the US, Revolut for business is available in 50 countries, including Japan, the UK, Australia, etc.

You can make unlimited bank accounts in around 30 currencies. If you deal with multiple currencies in your business ventures, you should really look no further.

Prices start from $0 up to $39.99 per month for freelancers. Companies can also get a free account or pay up to $149.99/m as they grow and need to raise their limits.

Small business owners and freelancers can sign up using an email address with a laptop or phone in minutes and have the account approved in 24 hours or less. You’ll automatically get a USD, GBP, and Euro bank account with a sort code, account number, and an IBAN.

For all the reasons mentioned, I recommend Revolut if you are doing business with international customers or you need a bank account in a currency that’s not USD.

Vergo

- For Interior Designers, Architects & Builders

- High savings interest rate

- Cash back

- Connects to accounting software

- Mobile check deposits

Vergo is a digital bank account founded in 2021 by Rich Kane and made specifically with architects, builders, and interior designers in mind.

As it’s focused on a narrow industry, it’s packed with tools and features to help entrepreneurs thrive. Of course, there’s a checking account and a rewards card, as well as expense tracking and various accounting integrations.

Viably

- Built for e-commerce

- Funding platform

- No-fee banking account

- Spending analytics

- Forecasting

Viably is another relatively new digital bank (since 2021) that’s also narrowly focused on one industry. This time, it’s e-commerce. It’s basically an all-in-one finance software that’s built to propel your e-commerce business.

Not only is there a fee-free banking account, but you can also get your business funded directly from the app.

The company uses your online shop’s data to give you fast funding offers. Once you’re approved, the cash is immediately deposited into your Viably account. Now, that’s what I call great service.

Winden

- No monthly fees

- Unlimited rewards

- No credit checks

- Unlimited free worldwide transfers

- Instant payouts from platforms

Another digital banking account that was launched in 2021, Winden is focused on internet economy businesses like SaaS, e-commerce, agencies, freelancers, creators, and similar.

Its business debit cards offer unlimited rewards, zero fees, and premium travel benefits.

ZilBank

- For freelancers, startups, and small businesses

- No monthly fees

- Payroll management

- Check printing

- Customized expense cards

ZilBank was also founded as recently as 2021 and is focused on freelancers, startups, and small businesses.

The company has partnered with Evolve Bank & Trust, an FDIC Member, to issue Visa business debit cards.

It allows non-residents to open a bank account if they have a US-registered company, a US phone number, and a passport from any country.

Can I Open a US Business Bank Account Online?

This is a question that many entrepreneurs have. Yes, of course, you can open a US business bank account online. In fact, it’s very easy, and literally, every company on this list lets you open a banking account online.

Some require more documents than others, while a couple of them also let you open an account even if you don’t live in the United States.

More Useful Articles About Digital Banking

- 15 Best Digital Banks and Banking Accounts in the USA

- Is There Chime Business Account? (5 Alternatives)

- 15 Reasons Why Businesses Should Open a Digital Banking Account

- 12 Best Digital Banks in the UK in 2023 (Curated List)

- 7 Best Banks in the UAE in 2023 (Personal and Business)

- 6 Best Banks in Singapore for Every Account Type in 2023