Similarly to other Latin American countries, Colombia had a high number of unbanked people until recently.

According to the World Bank, an average of only 55% of Latin American adults have an account at a financial institution. Additionally, people from rural areas have fewer bank accounts than in urban centers.

In Colombia, traditional banks provide expensive services mainly focused on high-income clients with fees and costs of checking, savings, and loan services averaging 5-10% of a monthly minimum wage, thus making them hard to afford for low-income clients.

In general, the unbanked people of Colombia and Latin America save and borrow predominantly in the informal sector at greater risk and cost.

However, the number of Colombian people opening their first financial account increased significantly in 2020 because, as in many countries worldwide, the government passed out billions in contributions during the coronavirus lockdown.

In total, the number of banked Colombians is higher than 31 million now, according to the government’s Banca de Oportunidades program.

Welfare payments and VAT rebates for more impoverished Colombians were vital to the boosted use of financial products.

Officials say nearly 86 percent of Colombians now have some type of financial account.

Apart from the pandemic, the government’s regulatory bodies also significantly contributed to the rise of digital payments and digital bank accounts. The speed at which they developed fintech regulations is often praised because Colombia was among the first Latin American countries to create a regulatory sandbox for financial innovation.

These flexible regulations allowed fintech companies to promote new digital products and financial services and to bring even more people on board. These outstanding conditions have created a once-in-a-lifetime opportunity for the rise of new digital behaviors.

During the pandemic, millions of consumers made their first e-commerce purchases. This period was a trigger for the adoption of contactless payments via cards, wearables, and mobile devices. This, of course, includes Apple, Samsung, Google Pay, and other e-wallets (some of them local) that use QR codes or NFC.

Let’s take a look at the major digital banking players in Colombia.

DaviPlata

DaviPlata was launched more than ten years ago by Banco Davivienda. Its owner, therefore, is a well-known traditional bank and not a fintech company.

However, this digital wallet is very important for the Colombian banking market and even the economy as a whole, as it introduced millions of people to mobile and digital payments.

DaviPlata is the biggest, most widely used financial app in Colombia, with more than 12 million users. It was and still is a tool for the inclusion of the unbanked people of Colombia, especially in remote and rural parts of the country, without access to physical bank branches.

Although DaviPlata doesn’t offer a physical debit or credit card, there is a virtual card that can be used online worldwide, in allied businesses in-store, and in national e-commerce stores.

With the app, one can top up minutes, shop, pay for services, withdraw money from Davivienda ATMs and even transfer money from one cell phone to another. There’s also the ability to take out money at Davivienda ATMs and offices.

READ ALSO: 5 Great Examples of Banking as a Service

IRIS

Dann Regional, a Colombian bank specializing in corporate and consumer finance, launched IRIS, the country’s first 100% digital bank for SMEs, in 2021.

The digital bank makes money management and payments quite easy for businesses. Business owners and accountants can access and manage expenses, organize transactions, and reduce costs from any device.

The clients can also make vendor and payroll payments, transfer funds to and from their IRIS accounts, obtain statements, schedule automatic transactions, and more.

The company’s premier product is the digital savings account that adapts the interest rate according to how much money the company keeps in the bank. At this time, the interest rate of 3% is applied to all companies that keep up to $500,000.000 in their IRIS account and 4% over $500,000.001.

The other notable financial product is the tailored credit line that’s can be obtained after the analysis of different payment sources such as acquisitions, the assignment of contracts, CDTS, and IRIS control accounts.

The requirements to apply for business credit are:

- Minimum one year of operation

- Source of payment and/or a real guarantee

- Annual sales upwards of $5,000 million

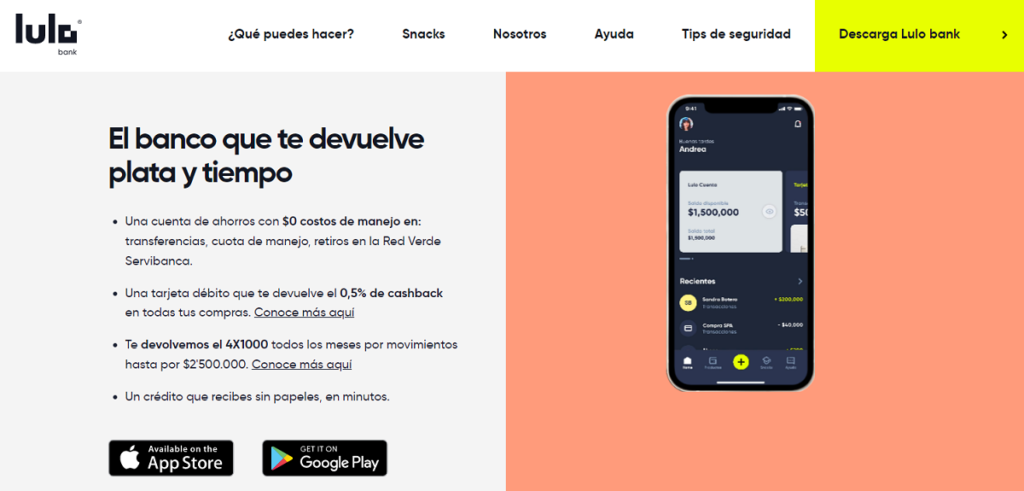

Lulo Bank

Lulo Bank was founded in 2019, and the app was launched in 2021. Lulo Bank is the first digital bank in the country and is part of the well-known Gilinski Group.

The company developed a typical digital banking account. I mean that in a good sense. The savings account has no monthly maintenance fees, free transfers, and free withdrawals from Servibanca ATMs.

The free debit card gives users 0.5% cashback on all purchases, savings rates of up to 2.5%, and you can even get back 4X1000 every month for movements of up to $2,500,000.

The more you keep in your account, the higher the interest rate you will get:

- From $0 to $525,000, you have a rate of 1.25% EA

- Between $525,001 to $1,000,000 is 1.50% EA

- From $1,000,001 to $2,000,000 is 2% EA

- $2,000,001 and up is 2.5% EA

Security is a huge factor for digital banks. For that reason, Lulo Bank implements the following security measures:

- Notifications of every movement and transaction

- Biometrics to protect your account

- Your money is protected for up to 50 million pesos with Fogafin deposit insurance

Lastly, the bank also offers easy applications for credit with rates from 1.15% MV – 14.70% EA and terms of up to 48 months.

Nequi

Nequi is a Colombian digital bank that was launched in 2016 by Bancolombia, a major bank and the first Colombian company to trade on the New York Stock Exchange.

In the six years since its founding, Nequi managed to become one of the most popular banks in the country, with more than 12 million customers. They also project to add 3 more million in the very near future.

It’s no wonder since the app is very intuitive and thus easy to use. Using only your cell phone, you can pay in thousands of businesses with Redebán dataphones and with Nequi and Bancolombia QR codes.

Create automatic savings goals that help you get what you want most. Also, organize your money in your pockets and store it under the Nequi Mattress.

Large and small companies alike that sell via social networks, in-store or online, can start getting paid with Nequi. Receive the money the same day in your Nequi account or the next day in a Bancolombia account.

There are three ways to charge with Nequi:

- Nequi Button – Integration via APIs

- QR Nequi – Print and display a QR code to get paid

- Nequi Collections – Charge via a notification to the cell phone or face to face with a QR code

You register with the one that works best for you, and then you can add the others.

Nubank

Nubank is the largest digital bank in the world and one of the largest fintech companies in the world overall. It was founded in 2013 in Brazil. Since then, the company spread to Mexico and Colombia.

In all these three markets together, there are more than 52 million users. The vast majority are in their home country, Brazil, and around two million combined in Mexico and Colombia.

Colombian David Vélez is the co-founder and CEO and the main engine behind the success of this digital bank.

Nubank is making all the right moves to attract tens of millions of customers that were either disappointed with the big banks or were totally ignored and neglected. If they continue on this path, there’s no stopping them, and they will take over the whole of Latin America in the years to come.

With Nu, you get a free checking account and a Mastercard credit card that can be used worldwide. This is the main selling point of Nu.

It should be noted that the company’s entry into the country is in its beta phase and it already has 5,000 customers who have received the card, and 50,000 new ones will be added in the coming months.

READ NEXT: 6 Ways How Digital Banking Helps To Save Money

RappiPay

RappiPay is a joint venture between Rappi and bank Banco Davivienda and is a standalone digital bank.

There are already more than 800,000 RappiPay users in Colombia, and over 200,000 have had a card issued. When you know that the account is free, plus you get a free debit card to use, it’s understandable.

With RappiPay, you can transfer money to other Colombian banks for free and withdraw cash at Davivienda ATMs for free. Top up your Rappi account and cell phone, and pay without contact on your Transmilenio, SITP, and Mio trips and save yourself the queue.

The popular RappiCard has a $0 lifetime handling fee, gives you 5% cashback buying trips at Rappi Travel, and coupons and discounts for many retailers such as Samsung, Cyglo, YouTube, Frenchies, and more.

Tpaga

Tpaga is a mobile wallet and a digital bank from Bogota that was founded in 2015. It offers its services to both personal and business customers.

Personal customers can use Tpaga to save, send and receive money, invest, request credit, secure a loan and make use of it in more than 8,000 points in the country. You can also invest in FIC and cryptocurrencies.

The app is incredibly popular with Colombians as it managed to get more than one million users on board.

The company is expanding and opening up its platform to allow other companies to operate their e-wallets on its digital platform and infrastructure. This open banking and fintech-as-a-service business model will allow the platform to be used to greater potential in the ecosystem.

Ualá

Ualá has been founded by a well-known Argentinian entrepreneur and historian Pierpaolo Barbieri in 2017. The fintech has since expanded rapidly from Argentina to other countries, including Colombia, by offering a simple payment account and a prepaid Mastercard.

There are no monthly fees, no fees to open or maintain an account, close an account, make money transfers between Ualá users, top-up funds, and no fees for ATM withdrawals worldwide.

To apply for Ualá, you need to simply:

- Download the app from the Play Store or App Store on your cell phone

- Complete the registration with your data from the app

- Receive your Ualá debit card anywhere in Colombia, completely free

- Activate your card from the app and save money by using it

With Ualá, you can manage your money easily from your cell phone without hidden costs.

READ NEXT: The Future Of Digital Banking (Five Likely Outcomes)

Benefits of Digital Banking

Digital banking has many advantages over conventional banking. There are also some drawbacks, of course. Regardless, we have to separate digital banking, usually executed by fintech companies, from online or mobile banking that traditional banks are delivering to their customers.

Fintech digital banks offer no to low fees, particularly for everyday banking, unlike standard banks that demand monthly fees, transfer fees and charge you for every other essential banking services.

Traditional banks have many expenses in terms of office and branch space; they have much more employees and legacy systems that are costly to sustain.

Digital banks have none of that, so they can afford not to charge for their accounts and give much better savings interest rates, therefore attracting more customers into their ranks.

The main way that digital banks make money is on interchange fees. They don’t charge these fees to their customers but to retailers and merchants.

That way the customers don’t have to pay for transactions, and the bank still gets to make money from these tiny transaction fees that add up quickly. For that reason, many retailers refuse to accept anything but cash.

Another thing that is beneficial to customers is that sending money is generally free and instant between people but often also to other banks. International transfers, more often than not, have an acceptable foreign currency exchange rate that isn’t designed to rip you off.

Conclusion

The digital banking space in Colombia is a lively one. There are digital banks that are products of longstanding traditional banks as well as newly developed apps by fintech companies from inside and outside of the country.

The recent pandemic may have been the most powerful force for the digitization of Latin America, helping to accelerate the migration to a payment ecosystem that is cardless and terminal-less without physical branches.

The government agencies also played a big part by bringing out swift regulations and a regulatory sandbox for fintech innovation. Thanks to that, more than 320 fintech companies are now operating in Colombia. That’s a 37% increase in the number of fintech companies since 2017.

The direct result of that is that digital banks and their apps are now popular and attractive products that have fallen on fertile ground and that the people of Colombia are eager to adopt.

However, there’s still a long road ahead for present and future digital banks in Colombia as customer retention and convincing the people to use them as their main bank account will be a challenge.