In the last six years, the Indonesian banking sector went through a fascinating transformation. 2016 was a crucial year in this regard as it was marked by the launch of Jenius, a digital banking product of BTPN, an incumbent bank.

Since then, 13 more digital banks have cropped up. Some were products of traditional banks, while others came from fintech companies.

The most recent regulations allow foreign companies to own 99% of local lenders, whereas the previous figure was 40%. These regulations also bolster faster permits for digital services.

The previous timeframe was 60 days, and now it’s a maximum of 14 days. Basic services such as accounts, savings, or transfers don’t even require a permit. Also, a digital bank offering such services only needs to report to OJK, the country’s financial services authority.

Apart from the 13 digital banks we are listing in the article, five further fintech startups are waiting to enter the market: BukuKas, Shopee, Grab, Gojek, and Youtab Indonesia.

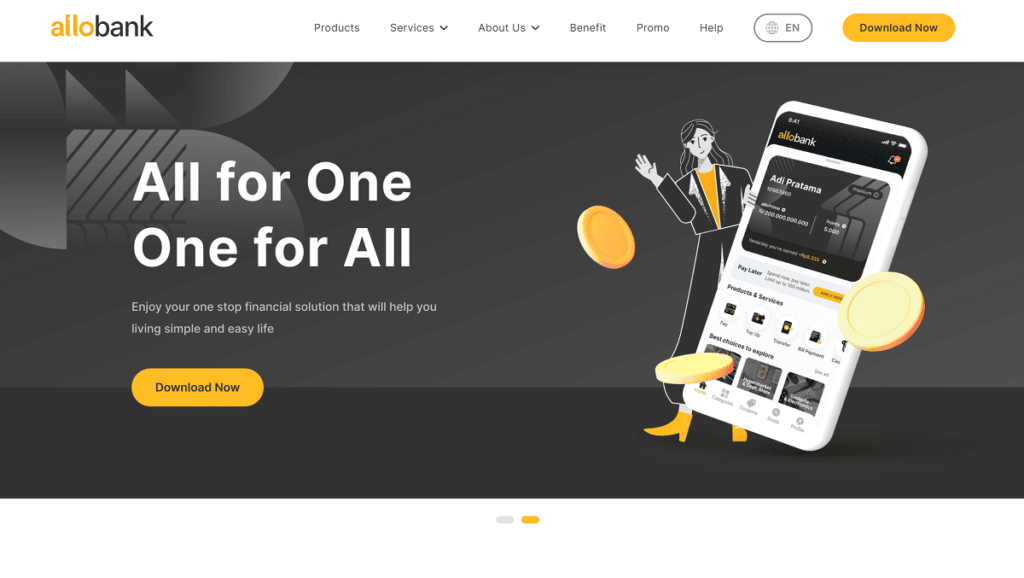

Allo Bank

Let’s kick-start this alphabetical list of digital banks in Indonesia with Allo Bank. This traditional Indonesian bank has a long history.

Previously known as PT Bank Arta Griya, in 1992, the bank changed its branding several times. The bank was acquired by PT Mega Corpora in 2021 and received OJK approval in March of the same year.

In June 2021, the bank changed its name again. This time to Allo Bank.

Allo Bank, unlike some other banks on this list, has a modern app that offers no monthly admin fees, an account that is easy to open, and above-market savings interest rates of up to 6%.

The Bank notably has an MPC Customer loyalty program consisting of Membership, Points, and Coupons that are combined and available on all CT Corpora platforms.

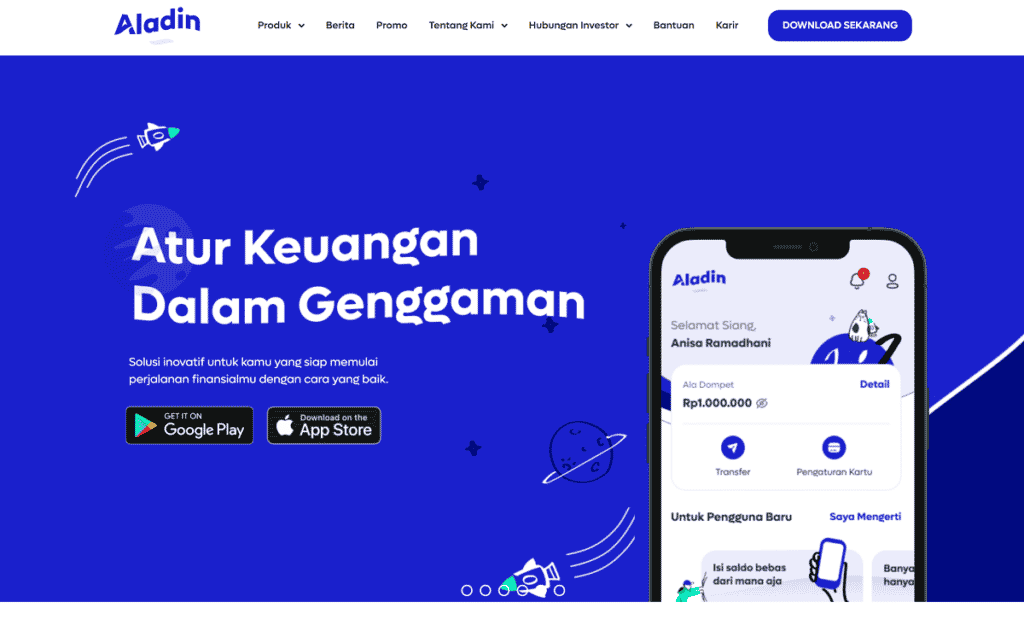

Bank Aladin

Aladin is on a mission to become the leading digital sharia bank. In its business, the company claims to adhere to Islamic values, such as trust, honesty, justice, respect for others, truth, and tolerance.

The account comes with a GPN debit card that you can use to shop in-store or online and withdraw cash at ATMs.

Apart from your main account, you can open up to 20 savings accounts based on a Mudharabah or profit-sharing contract. Your savings aren’t locked in, and therefore you can withdraw them anytime you want.

There’s also a way to donate to others anywhere, anytime, from the Aladin app. At this time, donations in the form of Zakat (Mal, Profession, Fitrah), Infaq, Waqf, and Qurban are available.

Bank Capital

Bank Capital was founded in 1989 but entered digital banking in 2020. For that reason, as it doesn’t have a separate digital banking entity, it’s more of an online bank still.

With its dedicated app, you can do many things you’d expect. For instance, you can check your balance, send money, and pay your bills.

There’s a personal and a business account, and both offer savings accounts and loans.

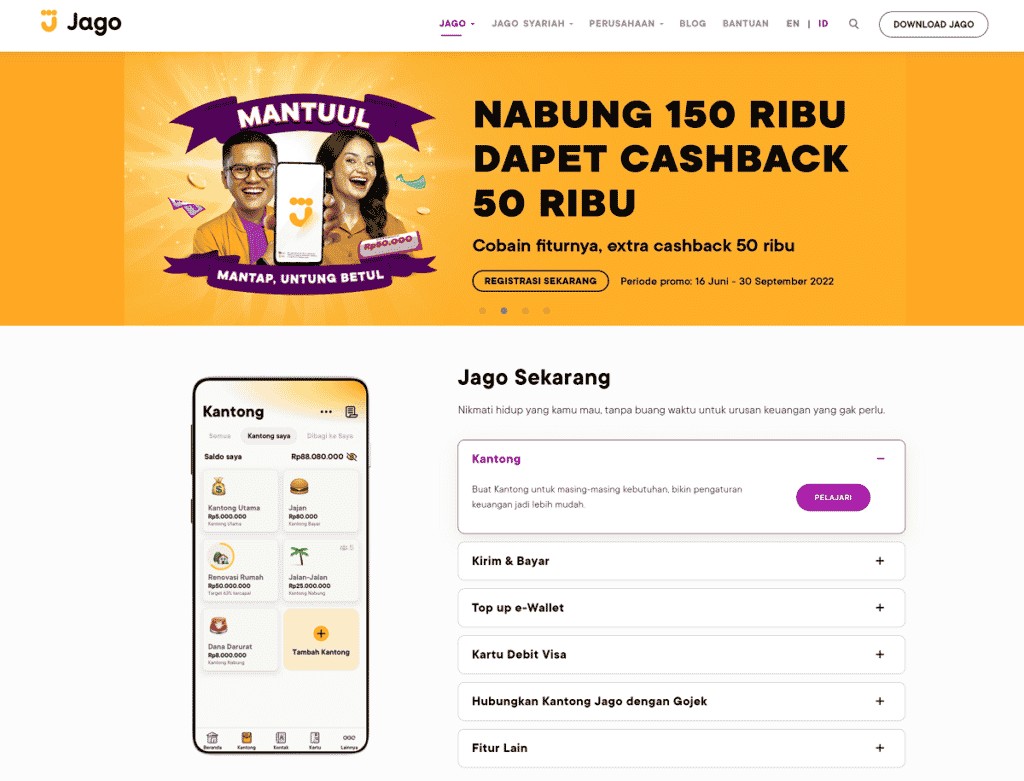

Bank Jago

Jago channels some of the best digital banks in the West. The company says that the Jago app was developed around a “life-centric principle.” The bank used to be called Bank Artos but changed its name in 2020 after a change in the controlling shareholder.

The Jago app itself was only launched in 2021 but has proven to be popular due to its appeal to the younger generations.

My favorite Jago feature is Pockets which are a practical way to manage your savings and expenses. By separating money into these pockets, or sub-accounts, you can better organize your money and spending.

By using a savings pocket, you can easily stash your money away for an emergency fund, for example. To get higher interest rates, you can make a time deposit that is flexible, and you can add money at any time.

Bank Neo Commerce

After 30 years in the banking business, BNC transformed into a digital bank. Previously called Bank Yudha Bhakti, the bank officially changed its name to Bank Neo Commerce.

BNC offers current and savings accounts, time deposits, and deposits on call products, as well as loans.

The interest rates are 2.50% for checking accounts, 3.50% for prime savings, and 0.50% – 1.50% for regular savings accounts. Deposits offer a 3.50% interest rate for 1 – 12 months.

Although the app looks and feels modern, there aren’t as many features as we’d like to see.

Bank Raya

Bank Raya is a subsidiary of Bank Rakyat Indonesia. It is revamping its products and pivoting to cater gig economy that’s on the rise and projected to have 75 million people in 2025.

They were the first company to accelerate the issuance of digital lending through Pinang, their first full-service digital lending product, that’s a well-known name now.

Raya has a plethora of digital banking products:

- A GPN debit card

- Pinang Connect P2P loans

- Paylater – buy now, pay later program

- QRIS payments

- Digital savings

- Pinang Flexi quick loans

Raya’s savings account is interesting because there’s no minimum balance required, no monthly admin fees, free transfers and cash withdrawals, and various savings options with competitive interest rates.

There are also pockets that are a great way to separate your money:

- Saku Bujet

- Used for daily transactions. Freely connect to the card for transactions

- Saku Jaga

- Deposit money and withdraw anytime without penalty.

- Saku Pintar

- Use Pocket Smart to get interest of up to 4%. Save automatically with two withdrawals in one year

READ NEXT: 6 Ways How Digital Banking Helps To Save Money

blu (BCA Digital)

BCA Digital is a fintech that provides financial, corporate governance, digital media, consulting, and, of course, banking services.

BCA developed their blu digital banking app that you can use to open a:

- bluAccount – without monthly admin fees

- bluSaving – 10 different types of savings

- bluGether – joint savings account for up to 24 people

- bluDeposit – simple and flexible time deposits with a higher interest rate than bluSaving

To start using blu, you only need to download the app and have your E-KTP and NPWP (optional) ready.

Even people living outside of Indonesia can open an account. However, they will need to have E-KTP, an Indonesian mobile number, and have to activate roaming for OTP SMS.

blu also has an extensive rewards program with 20+ promotional discounts

Digibank by DBS

Digibank by DBS offers personal and business accounts, as well as wealth management. The handy app offers savings, deposits, investments, credit cards, and instant loans at the tap of a finger.

Unlike some other banks in Indonesia, Digibank offers a Visa credit card that can be yours in “60 seconds,” and that comes with many benefits, such as rewards points and discounts with local retailers and restaurants.

And, although the bank offers a good savings rate of up to 3,50%, you can earn even more money by investing in government bonds. They deliver a rate of return above deposits and have guarantees from the Indonesian government.

Those that need to send money abroad will be happy to know they can now do that any time and wherever they are to fulfill all their business and personal needs. The Digibank app will quickly send money to your friends and family overseas as well as business partners.

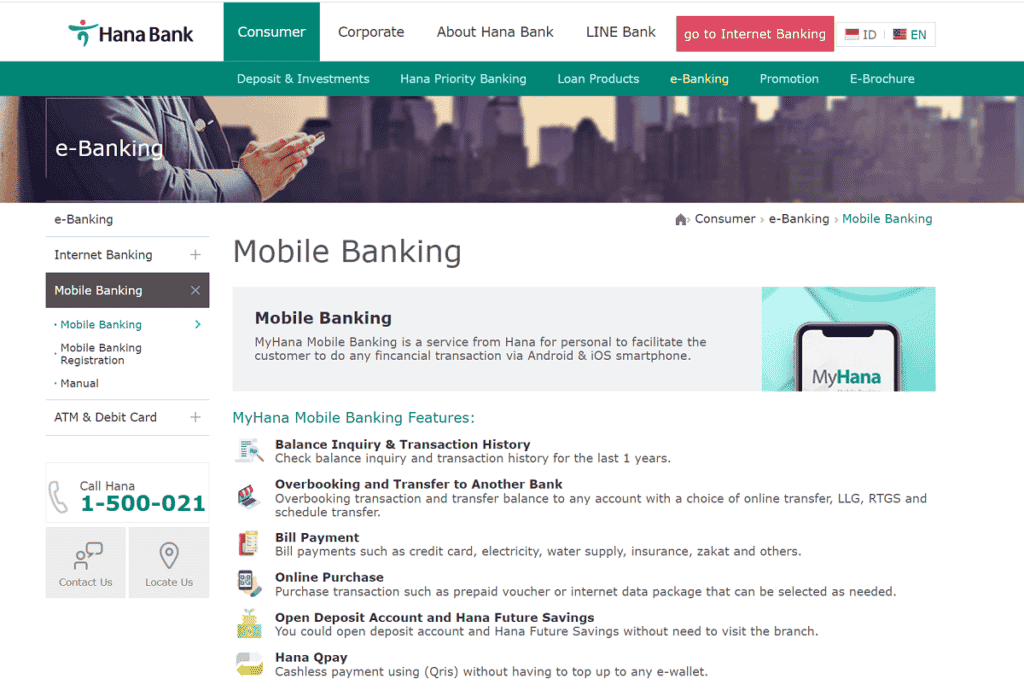

Hana Bank

Hana Bank has a long history. It started out in 1971 as Bank Pasar Pagi Madju and has rebranded a couple of times since then. The last rebrand came in 2020 since, when it’s known by its current name.

The bank’s mission is “to provide fast, convenient, and customer-focused services as well as have a high commitment to Indonesia’s economic development.”

The bank offers personal and business savings accounts that are easy to sign up for. All you need to do to open an account is to provide proof of identity with an ID Card, KITAS, Passport, or other identification as required.

On the personal side, it offers a regular savings account, Future Savings, Giro, and Junior.

The MyHana app offers all the typical operations you can expect to find in a digital banking app.

Jenius (BTPN)

Jenius is the original digital bank in Indonesia that kick-started the whole development process in the country. It was launched in 2016 by bank BTPN, a traditional bank dating back to 1958 when it was serving military veterans.

Jenius already has more than 3.3 million users that save and make transactions with the app and card.

With Jenius, it’s easy to buy credit and data packages, pay bills (credit cards, electricity, water, internet), pay zakat, donate or give to charity.

Online transactions at various merchants are now simpler. Just enter $Cashtag without the need for a debit or credit card.

Speaking of cards, there are three types of debit cards that you can use for various payments, including online transactions:

- m-Card

- e-Card

- x-Card

Apart from saving and deposits, now you can invest in Jenius to grow your money. Simply open the Jenius app, select Wealth at the bottom of the screen, then select the Investment

menu to invest in mutual funds.

READ ALSO: The Future Of Digital Banking (Five Likely Outcomes)

Jenius also offers business accounts through its app. Activate a business account in the Jenius app to separate/manage your business finances and download Bisniskit from Jenius on Google Play or App Store so you can manage your business more easily so your business can grow faster.

Jenius lists four amenities you get with a Jenius business account:

- Send and receive money to fellow Jenius, other banks, and other digital payments

- Track the entire history of transactions and download monthly financial reports in the form of e-statements

- Shop online at all Visa merchants using a virtual debit card

- Pay your business’ operational bills from your business account

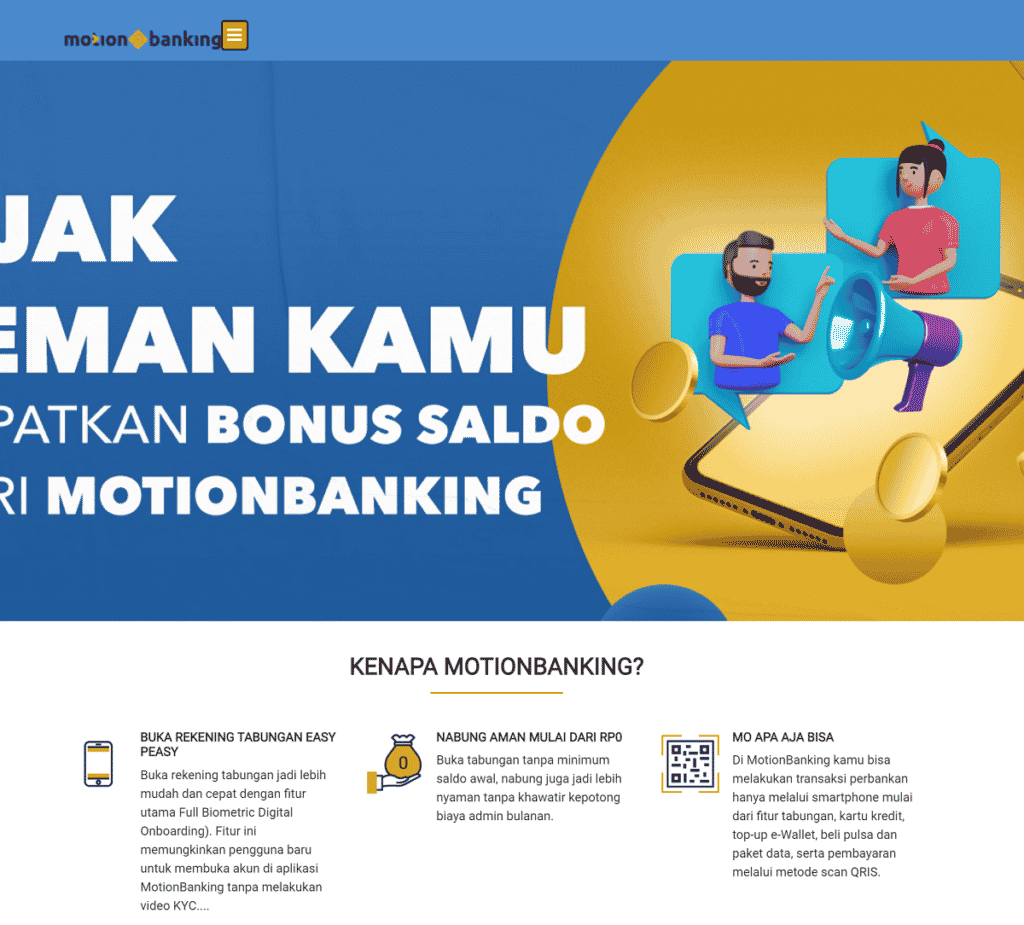

Motion Banking (MNC Bank)

Motion Banking is a mobile banking app from MNC Bank that was designed to provide day to day banking for MNC Bank customers to conduct financial and non-financial transactions, which can be accessed anytime and anywhere via smartphone.

Opening a Motion Banking savings account is easy and fast using Full Biometric Digital Onboarding. The savings account doesn’t require a minimum balance nor has monthly admin fees.

The MB app has the following features:

- Savings account,

- Credit card,

- e-Wallet top-up,

- Buying credit and data packages,

- payments via the QRIS scan method

QNB

The QNB bank is one of the oldest banking institutions in Indonesia, dating all the way back to 1913. However, like other traditional banks on the market, it has recognized the need to modernize and launch a digital banking product.

Anyone can register for QNB Online Banking online through their website. The app offers the following features:

- Fund your transfers, credit cards, Western Union payments, bill payments, and top-ups,

- Access your Accounts and Loans,

- Locate ATMs and branches,

- Redeem Life Rewards partners and points

- See interest & Forex rates,

- Request checkbook

- Apply for other QNB products

A new feature in QNB are time deposits that you can now open without having to come to a branch office.

QNB offers a full suite of banking products, and there’s not enough space to list them all.

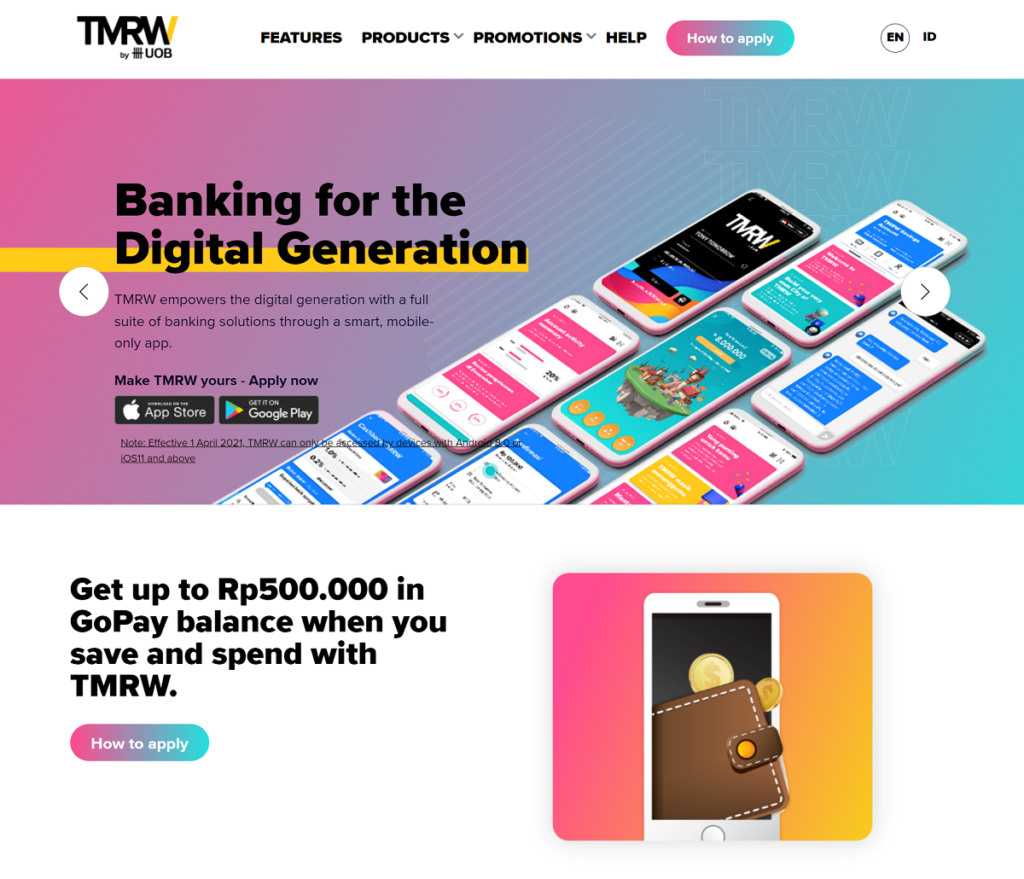

TMRW (Bank UOB)

TMRW is next on our list of digital banks in Indonesia. It’s a mobile bank that offers a checking and savings account, a GPN debit and Mastercard credit card, and even an interactive savings game.

People respond to incentives better if they’re gamified. The City of TMRW is, as we just said, an interactive savings game where the more money you save, the better your imaginary city will look like.

Personalize your city and transfer money easily between your TMRW Everyday Account and your TMRW Savings Account via the City of TMRW.

The Everyday Account has a savings rate of 0.5% p.a., and the Savings account, 3.50% p.a.

Benefits of Digital Banks

Digital banks have many glaring advantages over traditional banks. Not just in Indonesia but everywhere they came to the market.

First of all, they have low to no fees. That means that there are no monthly admin fees you have to pay. If a digital bank has paid plans, they always have an entry plan that’s free and enough for everyday banking.

Money transfer fees are also either non-existent, or they are very cheap, and foreign exchange fees are much fairer than what traditional banks offer.

I’ve recently had to open a traditional bank account. It took an hour sitting behind the clerk’s desk and signing a document around 15 times. Not to mention the various official documents I had to submit.

On the other side, you can open a digital bank account in a matter of minutes by simply downloading the app, typing your name, email, and address, and taking a photo of your ID and a selfie.

The process is incredibly easy and painless. Governments and financial institutions know everything about us already and have our info in their systems. There’s really no need to complicate the process.

What this traditional bank’s mobile app lacks are budgeting and analytics features. This is something most, if not all, digital banks do very well.

Every single transaction you make is categorized so you can see a clear breakdown of your expenses.

Easily make a budget for your week or month by setting a limit for the category you want to have under control. For most people, it’s groceries, restaurants, or entertainment that can get out of control without a proper budget.

Lastly, we have savings interest rates. They are often much higher with digital banks as they want to incentivize you to deposit more money with them as they need a cash boost.

Conclusion

It’s going to be an interesting couple of years ahead of us as all these banks start to “fight” for customers. This should be very beneficial to Indonesian people as they will get more benefits for the same or even less money.

However, some of these banks won’t survive, and we’ve already seen at least one bank (Wokee) that’s already gone.

Indonesia is a large country with almost 300 million people, many of which are still unbanked or underbanked, and as long as banks focus on them as well, and not only on the middle class, there should be more than enough users for everyone.