Astonishingly, 95% of Saudi Arabia’s population used some form of digital banking. This research didn’t include class 4 or “deprived” citizens, of which there are 11% in the country.

Still, digital channels are the number one method of interacting with banks. That must mean that the country is filled with neobanks, right? Well, not so much.

In fact, it’s exactly the opposite. There’s barely a challenger bank in sight as the market is still prevalent with traditional banks.

There are, in total, 35 banks on the Saudi market:

- 11 local traditional banks

- 3 local digital banks

- 21 foreign bank branches

There are also 19 licensed Saudi fintech companies that provide payment services, consumer microfinance, and electronic insurance brokerage.

It’s apparent that people are still using traditional online and mobile banking to fulfill their financial needs. Only three digital banks covering 35 million people won’t make a dent in the country, with so many affluent people willing and eager to use digital banking.

A whopping 88 percent of people are now ready to open a digital-only bank account, and 79 percent of Saudis actually want to share their data in exchange for a better banking service.

The same research also lists the reasons why customers have left their banks. Here are the main ones:

- The bank had poor customer service

- The bank had limited products

- Better loan offer from the new bank

- The bank increased its fees

- Better credit card from the new bank

- Better digital channel experience from the new bank

- Better deposit rates from the new bank

- More or better branches in another bank

The KSA banking market could definitely benefit from more competition, especially from fintech companies that are willing to offer a better, personalized customer experience, offer more financial products and embed new asset classes, offer better loans, and have no or low fees for day-to-day banking.

Although digital banks aren’t known for their exceptional customer service (on the contrary), they are certainly known for offering innovative financial products, a better user interface, and no fees.

They also offer good credit cards that have cashback and often have much better saving interest rates than incumbents.

The neobanks will face stiff competition from the Kingdom’s largest banks, such as Saudi National Bank, Al Rajhi Bank, and Samba.

Of course, Saudi Arabia isn’t the only country in the region to experiment with digital banking. We recently wrote about UAE.

Let’s explore what neobanks and digital banks from incumbents there are in KSA.

D360

D360 is a new digital bank that got its license in February 2022. It’s only the third neobank in the country to get a digital banking license.

The bank is yet to hit the market. However, we do know that it will be led by Derayah Financial Company and be funded by the Public Investment Fund to the tune of 1.65 billion riyals ($440 million).

Not much else is known about this neobank. Nevertheless, the Kingdom is investing heavily in the metaverse, blockchain, and many other technologies to diversify the economy and reduce oil dependence.

KSA’s Public Investment Fund is spending a lot of money not only on this digital bank but also on a new competitive gaming platform in Europe, for instance. Just to show you the scope of these investments.

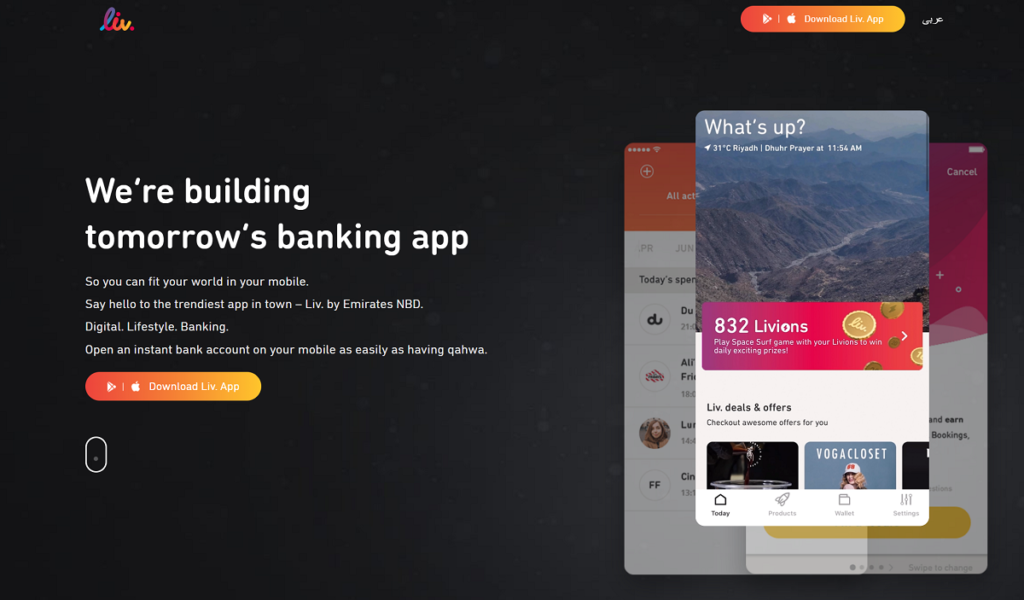

Liv.

Liv. is the first digital lifestyle banking app in the GCC designed to fit your lifestyle and finance in one app. It was launched by Emirates NBD, one of the top banks in UAE.

To get a bank account with Liv., you only need a KSA mobile phone number, valid Absher credentials, and, of course, a smartphone.

As is the case with most other digital banks, Liv. offers a simple account with no fees, no physical branches, easy money transfers, and good savings rates that is geared towards the younger demographic.

Here are some of its benefits:

- 2% interest rate and automated savings rules

- Discounts on concerts, events, promotions, and other exclusive benefits

- Automatic expense tracker to help you check where all your money goes for better money management

- Activate your card, lock & unlock it, order a new one, and more – directly in the app

- Pay friends and split bills using social media

- Instant money transfers using a mobile number

- Pay all your bills with one tap with SADAD

- Withdraw cash from any ATM in KSA for free

- Transfer and receive funds from any bank in KSA

- Get Statements directly in the app

- Collect Livions to win unique prizes

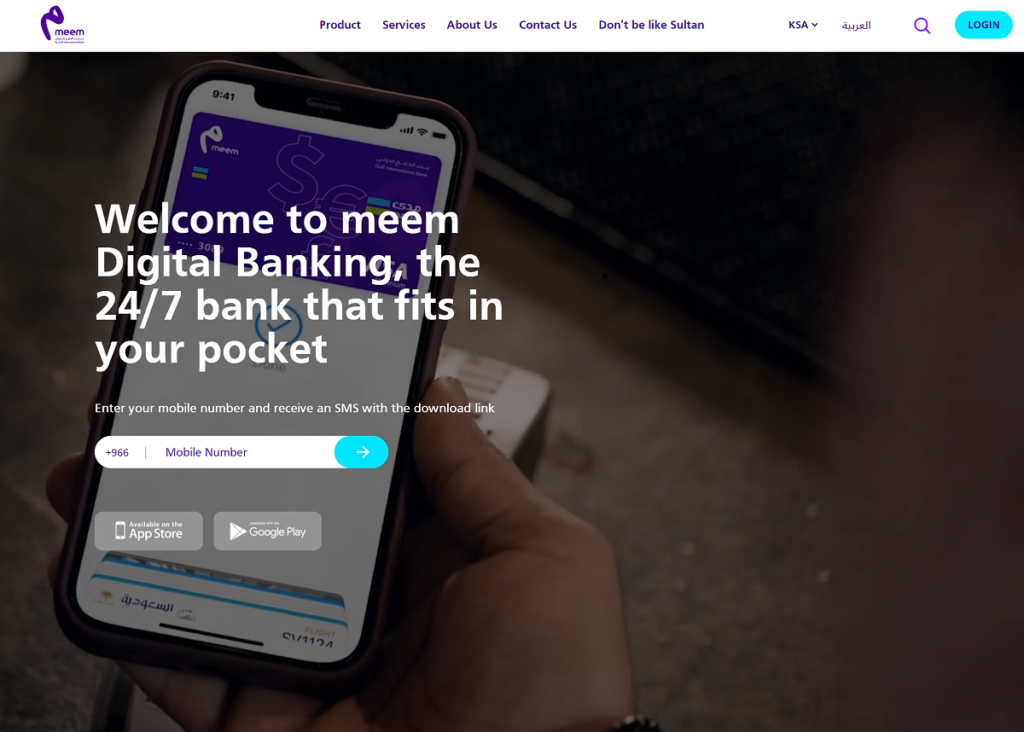

Meem

Meem is the retail banking arm of Gulf International Bank (GIB), owned by the governments of the six GCC countries. However, the bank’s main shareholder is the Public Investment Fund, which has a majority stake of 97.2%.

Meem is also the first digital Shariah-compliant bank in the world. It was launched in the KSA in 2014 and in Bahrain in 2018.

Since then, meem has been following the mobile-first approach, allowing you to bank easily with a minimum number of manual inputs or branch visits.

The company is offering:

- OnePack account

- Credit card

- Home finance

- Personal finance

- Murabaha deposits

The OnePack account offers a current and savings account, as well as a multicurrency account – all in one card and app.

Speaking of the cards, you can get a Shariah-compliant meem credit card with no hidden fees that offer a range of features and benefits, including:

- A flexible installment program

- A generous rewards program

- Low FX charges

- Purchase protection

- Access to selected airports around the world

If you need a mortgage, you’ll be happy to know that meem has a 100% digital application process that includes E-title deed transfer and is based on the principles of Murabaha.

Apart from that, you can get financing up to 5 million SAR for a period of up to 35 years. The APR is starting from 4.68% with admin fees of 1% or 5,000 SAR.

Personal finance is Shariah-compliant and 100% digital, with competitive rates and financing up to 1.5 million SAR for up to 60 months.

Meem also offers the world’s first real-time Shariah-compliant term deposit and commodities trading.

READ NEXT: 6 Ways How Digital Banking Helps To Save Money

Saudi Digital Bank

The Saudi Digital Bank, or SDB, is a creation of Abdul Rahman Saad Al-Rashed and Sons Company. This is a well-known KSA holding company with a portfolio of subsidiaries specialized in real estate, investment management, construction, and other sectors.

The new digital bank has a capital of USD 400 million, so it will be interesting how the final product looks like. It seems that they have brought in some experienced people.

It’s not known yet at what time SDB will hit the market.

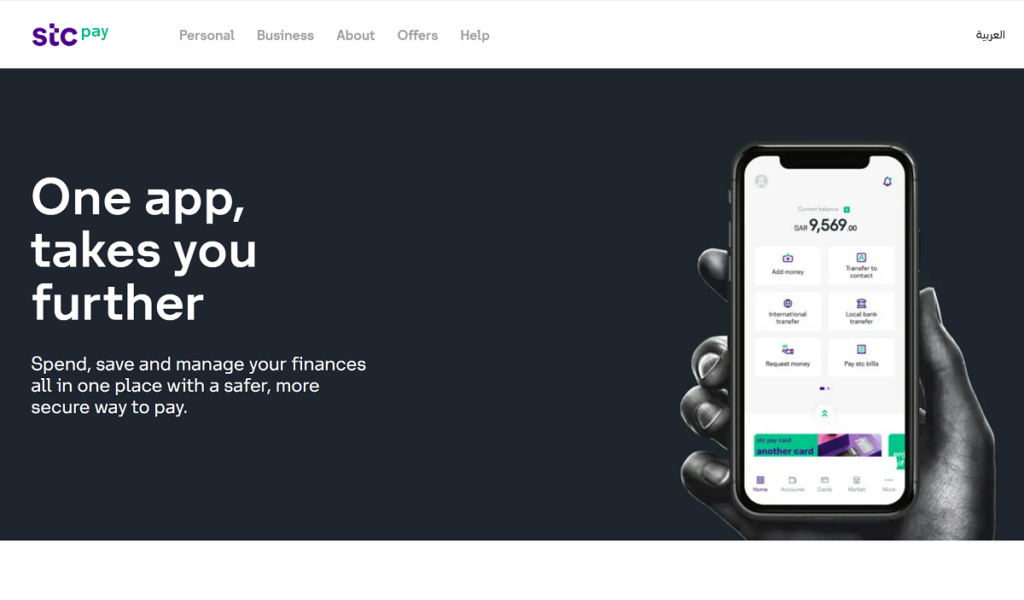

STC Bank (STC Pay)

STC Bank is one of the two digital banks to originally get the license from SAMA (KSA Central Bank). The bank started as an e-wallet named STC Pay, launched in 2018 as a subsidiary of the Saudi Telecom Company (STC).

The e-wallet has since developed into a financial app. The app offers international money transfers in partnership with Western Union.

Interestingly, WU bought a 15% stake in STC Pay and is therefore going to be a partner in the newly formed digital bank.

This deal made STC Pay a billion-dollar company and created the first “Saudi unicorn and the first fintech unicorn in the Middle East.”

Since STC Bank still isn’t on the market, let’s see what STC Pay is offering, as the two products could end up being very similar.

There are both personal and business accounts, as well as debit and credit cards. Naturally, there are different ways you can transfer money in or out of the account.

There’s also a marketplace where you can buy top-up cards, as well as directly buy millions of movies, TV shows, books, video games, music, etc.

STC Pay also has analytics and budgeting features, helping you stay on top of your spending and encouraging you to spend more wisely and save more.

Benefits of Digital Banking

Digital banking has many benefits over traditional banking. It also has some drawbacks. However, we have to separate digital banking, usually implemented by fintech companies, from online or mobile banking that incumbent banks are offering to their customers.

Fintech digital banks offer no to low fees, especially for day to day banking, unlike traditional banks that charge monthly fees, transfer fees and charge you for other crucial banking products.

Traditional banks have overhead in terms of office and branch space; they have much more employees and legacy systems that are expensive to maintain.

Digital banks have none of that, so they can afford not to charge for their accounts and offer much better savings interest rates, thus attracting more customers into their ranks.

You see, digital banks mainly make money on interchange fees. They don’t charge these fees to their customers but to retailers and merchants. That way, you, the user, don’t have to pay for transactions, and the bank still gets to earn money from these tiny transaction fees that add up quickly.

Another thing that is beneficial to customers is that money transfers are generally free and instant between users but often also between other banks. International transfers, more often than not, have a fair foreign currency exchange rate that isn’t designed to fleece you.

READ ALSO: The Future Of Digital Banking (Five Likely Outcomes)

Conclusion

The KSA market is enormous, and people are more than ready to jump into digital banking. That readiness isn’t reflected by the banking market in the country. The Kingdom is falling far behind other developed countries and even some GCC markets.

It seems that the government has snapped out of it and is trying to fast track some fintech companies to quickly develop the digital banking landscape in the country.

However, it could be 3-5 more years until the competition heats up and the people get the service that they deserve and that is expected in today’s world.

Gone are the days of dinosaur banks offering subpar customer service, poor banking apps, and meager financial products.

The world is everchanging and the fintech industry isn’t staying idle.