If you’re reading this, that means you’ve heard of the company, either from your friends and family or you saw one of their ads.

As a long-time Wise user, I decided to write a more personal review of the popular money transfer app and debit card.

There are too many run-of-the-mill reviews of the app out there, and not many that highlight real-world use cases.

So, without further ado, here’s what I think of Wise after using it for several years while shopping, traveling, paying and getting paid, and sending money abroad.

I’ll keep this short. Wise, formerly known as TransferWise, is a fintech company from London that launched its somewhat unique product in 2011.

This means they’ve been around for more than 10 years, and their app isn’t some kind of fad as the user base is constantly growing and is now standing at around 16 million people worldwide.

The company also has more than 5,000 people working for them in 17 countries across 4 continents.

How Wise Works

Wise uses a clever way to link their bank accounts all over the world.

For us, the users, that means that we’re not sending money directly to the recipients but to local Wise accounts that then transfer the funds in local currency to their destination.

The company simply uses the best exchange rate you can get (the one you see on Google) and adds a slight fee.

This starkly contrasts traditional banks, post offices, and other money transfer services like PayPal that add a massive markup to their seemingly “free” transfers.

With Wise, the person transferring the funds saves on fees, and the recipient gets all the money for free in his or her local currency.

READ ALSO: 4 Ways to Transfer Money Using Routing and Account Numbers

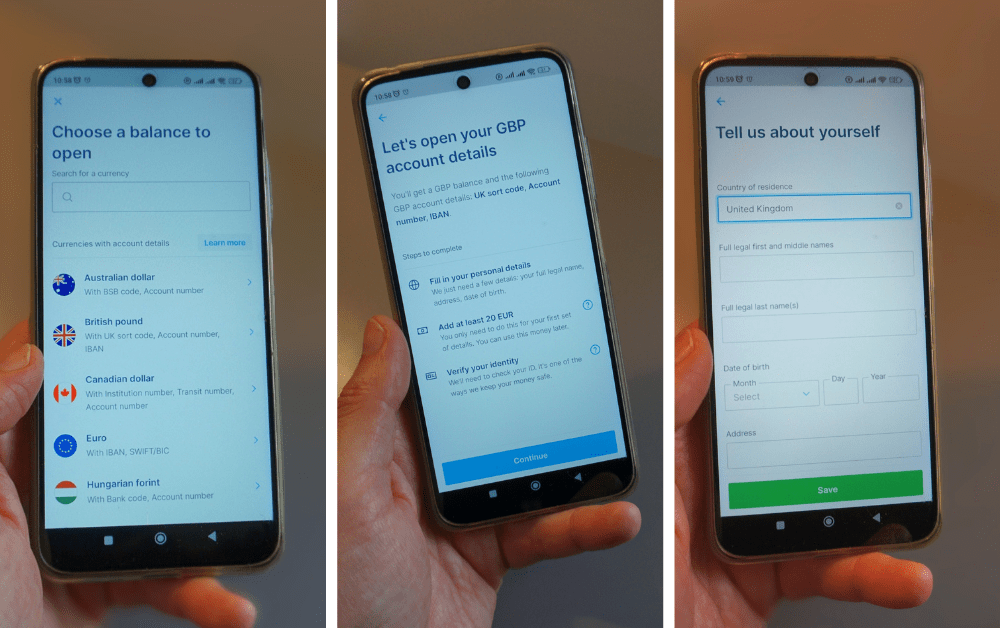

How to open a Wise account

Wise is more than a simple remittance service.

You can have a Wise account in a couple of minutes, as the process is easy and straightforward for both personal and business accounts (yes, you can open a business account, too!).

You can register by using your email address or, even more accessible, by using your Google, Facebook, or Apple account.

Simply add a password and select your home country.

You’ll need to have an ID for verification as well.

After that, you can choose to open up to 10 balances.

Basically, those are currencies with account details like IBAN, account number, sort code, or whatever they’re called in certain countries.

These accounts enable you to pay and get paid in a local currency.

The 10 currencies (with account details) included are:

- United States dollar

- Australian dollar

- Canadian dollar

- New Zealand dollar

- Singapore dollar

- Euro

- British Pound

- Hungarian forint

- Romanian leu

- Turkish lira

Additionally, there are 40 more currencies that don’t have account details, but you can keep a balance or send/receive money.

That effectively means that you can keep 50+ currencies in your account and can convert money between any of these currencies that you hold in your account.

Wise Pros & Cons

| Pros | Cons |

|---|---|

| No monthly fees | ATM fees above €/£200/$100 |

| Transparent money transfers | Debit card not free and not available in many countries |

| Great exchange rates | Deposits not insured |

| Easy to sign up | No cashback |

| Account details for 10 different countries | No savings interest rate (except UK and Singapore) |

| Holds 50+ currencies |

Features

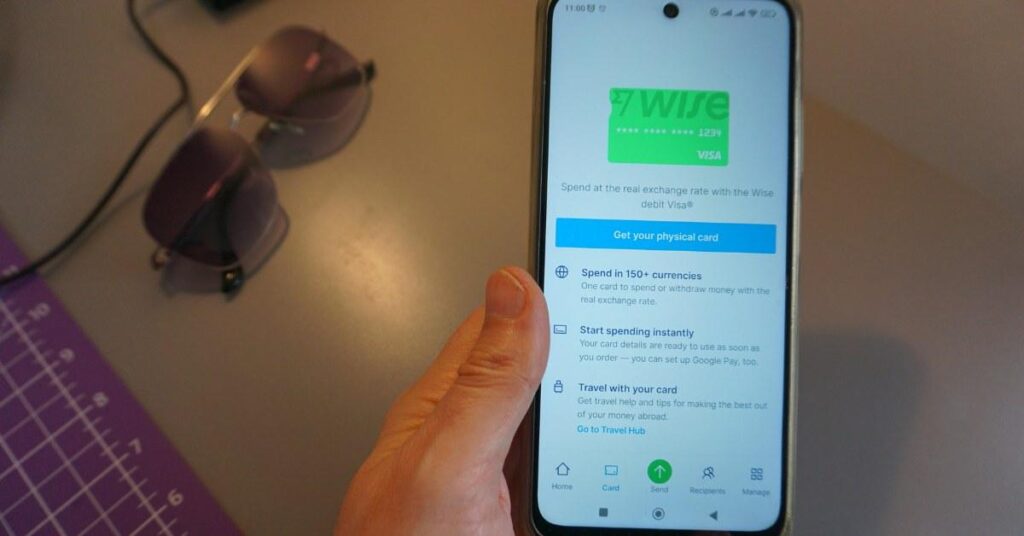

Wise Debit Card

Wise has a multi-currency account that comes with an optional debit card.

Although I ordered the card for a small one-time fee, you really don’t have to.

Simply add the virtual debit card to your favorite digital wallet like Samsung, Google, or Apple Pay.

I used the card (virtual and plastic) around the world, and there were zero transaction fees and low conversion fees.

If you have money in your account in that currency, there are no fees at all.

For instance, I once got paid in Danish krone for a gig, and I kept it (didn’t convert to my currency).

This came in handy when I traveled to Denmark as I didn’t have to convert any money.

Wise claims that you can save up to 88% when you spend internationally with their Wise debit card.

Although I didn’t crunch the numbers, it does sound about right to me.

The FX fees that Wise charges are only 0.35% compared to the nearly 3%+ that banks and other services normally charge.

I already mentioned virtual cards.

My virtual/digital card has different details from my physical card and can be frozen after each use.

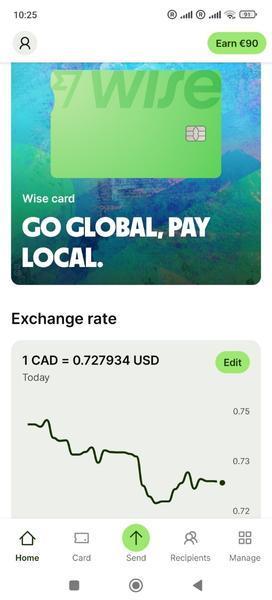

You can also hold more than 50 currencies on Wise. But can you convert these funds into other currencies?

You can do that as you wish for a low conversion fee.

Debit cards aren’t available in all countries, unfortunately.

They are available in the US, the UK, Australia, Singapore, Europe, New Zealand, and Japan and are perfect for frequent travelers, expats, and those that have bank accounts in different countries.

READ NEXT: Cash App to Venmo Transfers: Tips to Help You Do It Right

Wise Mobile App

For everything, there’s an app nowadays, and Wise is no different.

It makes quick and fast money transfers and allows you to monitor the status of the transfer, send verification documents, and make payments.

It’s compatible with iOS and Android devices.

International Money Transfers

Wise is best known for international transfers including currency exchange.

From my experience, the transfers are fast, reliable, and in most cases cheaper than the competition.

They’re also far cheaper than traditional banks, post offices, Western Union, PayPal, and similar.

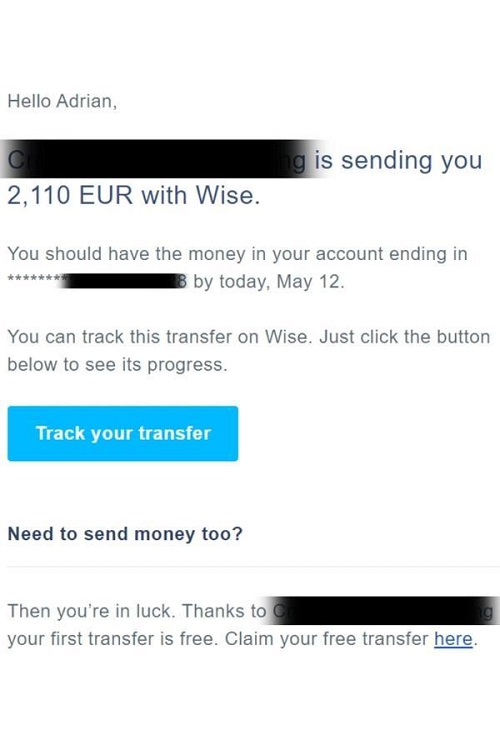

The recipient gets an email when the money is scheduled to arrive, coupled with a link to track the transfer.

Just like when you’re getting your mail delivered.

I wish traditional bank accounts had this level of customer service and a high-quality user interface.

When I’m sending the funds from the Wise app, I can clearly see how much the fees are, how much money the recipient is getting, and when.

This is only comparable to other similar remittance services and miles ahead of any direct bank-to-bank transfer we’re used to, especially when making business payments.

Assets

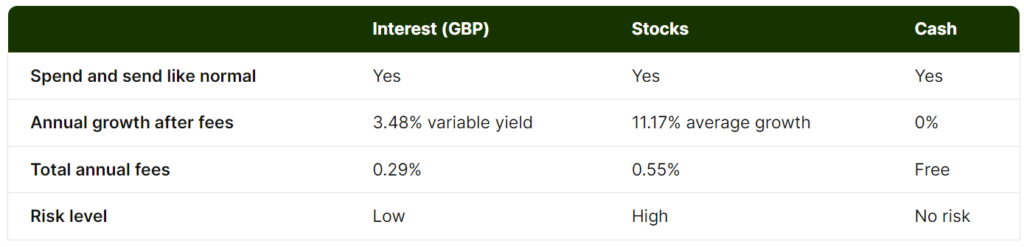

I love that Wise is finally offering some kind of savings interest rate or an investment opportunity to put your idle money in.

The feature is limited to a couple of countries (UK and Singapore) for now, but at least it’s a start, and hopefully, the company will expand it to other territories.

So, what am I talking about here? The feature is called Assets, and it gives you the option to invest your money into a low-risk fund with government-backed assets that will give you around a 3.48% variable rate (based on past experience).

You can also invest your funds in stocks and hold a share in the world’s biggest companies with an 11.17% average growth.

None of this is free, and there is a risk of losing money, too.

The annual fees are relatively low and comparable to other managed portfolios, for instance.

Business Account

Not all digital banks offer business accounts. With Wise, you can get a dedicated bank account for:

- e-commerce stores

- online publishing

- YouTube

- account for freelancers

- as well as other types of small to medium businesses

With this account, you can pay your expenses, invoices, contractors and freelancers worldwide.

Companies and startups can automate their payments with a powerful API, create invoices, and even integrate with Xero.

I use the business card to make online transactions and pay for any and all business expenses I have, among other things.

RELATED: 12 Best Digital Banking Accounts for the US Business

Wise Pricing & Fees

- Free account setup

- No monthly fees

- €7/$9/£7 to order a debit card

- One-time fee of £45/€50 for business accounts (free in US/AUS/JPN)

- 0.41% fixed fee to send money (varies by currency)

- 0.33%-3.56% to convert a currency using your card

- Free ATM withdrawals up to $100/£200/€200/30 days, after that 2%/1.75%

- $4.14 to receive USD wire transfers

Wise doesn’t have many fees.

However, some of them can add up. If you need to withdraw a lot of cash each month, for instance. In that case, Wise might not be the best for you.

A physical debit card comes with a one-time payment of around $9, depending on where you live.

Business account opening can also be costly in a handful of countries for some reason.

However, when we’re talking about international money transfers, Wise arguably has the best rates in the market.

Every time you’re making a transfer, you’ll clearly see exactly how much you’ll be paying and when the funds will arrive.

And if Wise isn’t the cheapest at that moment, it will show you!

That’s right, you can find out on their website (or app) what the best service is for your transfer.

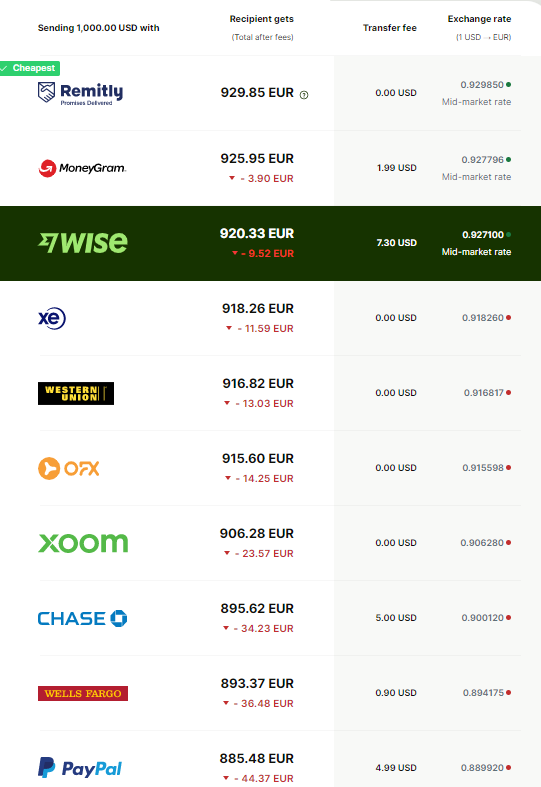

For instance, if I were to transfer $1,000 to someone in euros, there would be a total fee of $7.30 if I use a connected bank account.

The recipient will receive €920.33. That’s still worse than Remitly (€929.85) and MoneyGram (€925.95).

However, as the website will tell you, the transfer might be faster even though they may be a bit more expensive than others.

Also, look how far down the list traditional banks and even PayPal are. Imagine saving $40 per transfer by not using them.

How Long Does a Transfer Take?

Due to its advanced technology, the average Wise money transfer takes much less time than the usual bank transfer.

Transfers between Wise accounts are instant, and transfers to other bank accounts often take between several minutes and several hours.

On the Wise website, you can find four different reasons for the amount of time that it’ll take for the money to transfer:

- How you pay (some payment methods are quicker than others)

- The countries you’re sending from and to (every currency and country is different)

- What time you pay for your transfer (outside normal working hours and national holidays add extra time), and

- Security checks (verification can add extra time to your transfer)

Is Wise Safe?

I give Wise five stars when it comes to safety and security.

The company has an excellent track record and is regulated by the FCA in the UK and FinCEN in the US. Around the world, it’s regulated by the country’s local authorities.

The app has real-time notifications. That way, you’re always mindful of what’s happening with your Wise account and card.

There’s also a dedicated fraud and security operations team within the company that monitors for any anomalies and performs routine vulnerability scans.

Although Wise is a fintech company and not a bank, there’s no deposit insurance with the FDIC, FSCS, CDIC, etc.

That doesn’t mean your funds are protected.

I’d say they are protected even more so, as they are kept safeguarded in reputable banks and used only for their intended purpose.

The funds aren’t speculated with, and would be returned to you in whole, and not up to an insured amount, as is the case with banks.

Customer Reviews

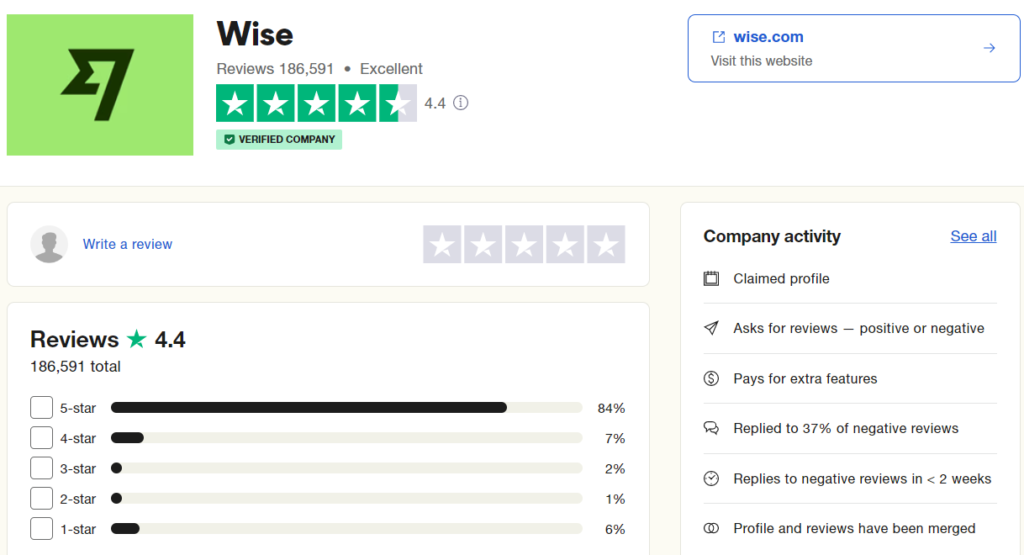

Wise has a 4.4 rating out of more than 186,000 reviews on Trustpilot, with 84% of customer reviews saying that it’s an excellent service and only 6% that it’s bad.

As with most other digital banks, there seem to be people getting their accounts suspended out of the blue. It’s probably due to the tough anti-money laundering regulations the company has to adhere to.

Unfortunately, even people who have done nothing wrong can end up with their accounts suspended. Resolving these issues is very slow in some cases, too.

READ ALSO: How to Send Money from PayPal to Venmo

Who is Wise Best Suited for?

Now that we’ve covered Wise’s most important and most used features, do you feel like this is the banking account for you?

If you’re sending money to family and friends abroad or you’re transferring money between your bank accounts in different countries, it will be perfect.

From my experience, it’s best used as a spending account and money transfer service.

I don’t hold great amounts of money in it, but it does help me save significant sums on my travels and currency conversion fees when sending cash or spending it online or in stores, restaurants, bars, etc.

I also saved plenty of money when moving money between my bank accounts in different countries to make a deposit for a car and an apartment. All went without hiccups and was very fast.

Freelancers, small business owners, contractors, and anyone else that pays and/or gets paid in a different currency will love the app.

I find it much more user-friendly than the likes of Payoneer, PayPal, and similar apps used for international business payments and expenses.

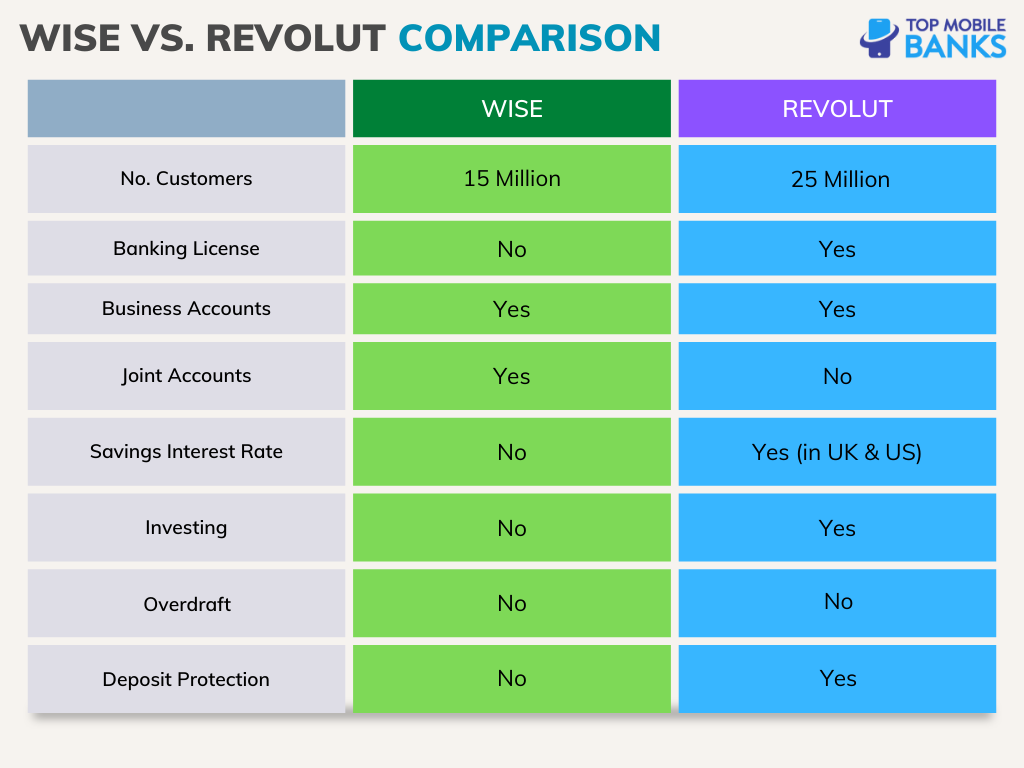

Wise vs. Revolut

Having used both for a long time, I can see some apparent differences and similarities between the two apps.

On one side, Revolut has a clear goal – to become a financial super app.

For that reason, it offers a more rounded product with more features and benefits to users.

It also has pricing tiers, with the free account basically comparable to Wise.

But to get the most out of Revolut, you’ll have to upgrade to one of the top two tiers.

Wise, on the other side, concentrates on offering a free banking account that lets you hold, spend, and move money with ease around the world at market-beating prices.

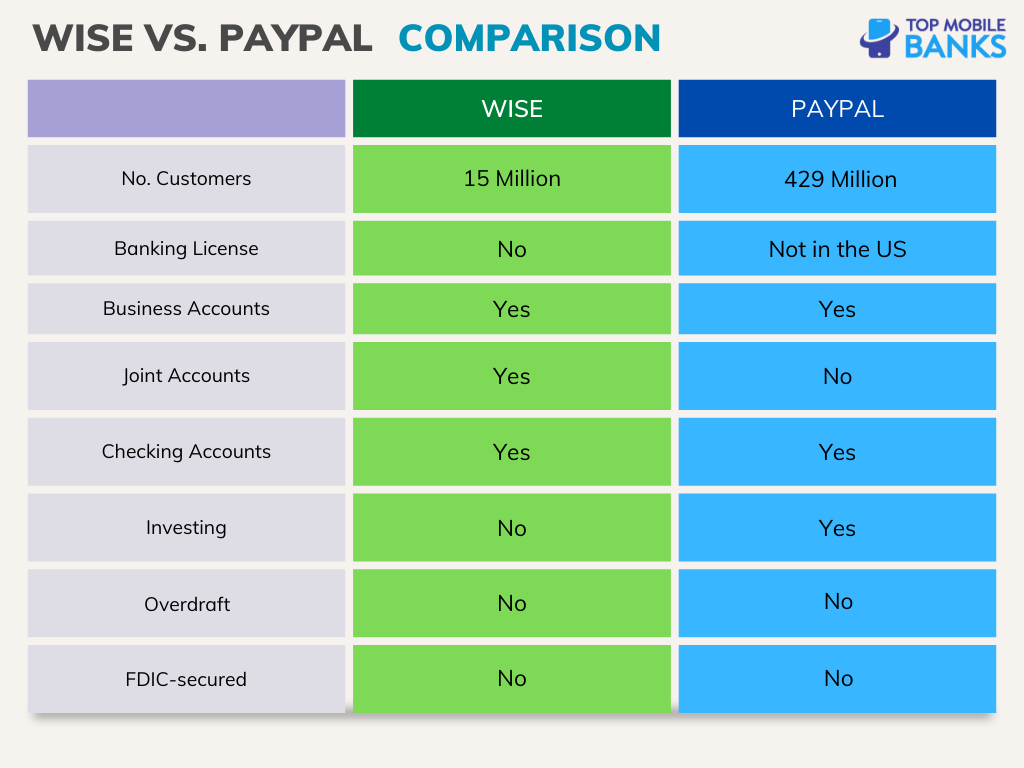

Wise vs. PayPal

I have been using PayPal for as long as I remember.

Much less so in recent years when I discovered Wise and Revolut.

In my opinion, Wise is still the best option for international money transfers.

It is affordable, fast, and transparent.

PayPal is readily available to most people, as so many people already have an account ready to send and receive funds.

It’s more than a simple money transfer service, and with hundreds of millions of users, it isn’t going anywhere.

With both debit and credit cards and their famous purchase protection and security, there’s still value there.

That being said, Wise has much better fees for international transfers than PayPal. It’s simply because Wise doesn’t move money across borders but instead uses local accounts in all supported countries to make payments.

It’s thus able to give us the actual mid-market rate, as it’s cheaper for them too.

More Useful Articles About Digital Banking

- 12 Best Digital Banking Accounts for the US Business

- 11 Best Digital Banks in the EU (All Account Types)

- 15 Best Digital Banks and Banking Accounts in the USA

- 8 Best Digital Banking Accounts for Digital Nomads

- 9 Best Digital Banking Accounts in Singapore

- 12 Best Digital Banks in the UK (Curated List)