Deciding between Chime and Ally isn’t easy. Each has unique features that make them stand-out options for digital banking; however, the question is which one is best overall.

Ally offers a wider choice of financial products than Chime and has a bigger interest rate for savings accounts. Chime, on the other hand, has a simple checking and saving account that is suitable for nearly anyone looking for a free bank account.

Let’s dive a bit deeper and see how they fare against each other in terms of accounts and cards, credibility, savings, and investing.

[lasso rel=”pxf” id=”10713″]

Pros & Cons

Pros

| Chime | Ally |

| No minimum balance requirement | No overdraft fees |

| No monthly fees | Free transfers |

| Fee-free overdrafts up to $200 | Free overdraft service |

| 2.00% APY | No minimum balance requirement |

| 60,000 fee-free ATMs | No monthly maintenance fees |

| No foreign transaction fees | 55,000+ fee-free ATMs |

| Mobile check deposits | Checking, Savings, CDs |

| Paycheck up to 2-days early | Personal and auto loans |

| Mortgage | |

| Investing and retirement |

Cons

| Chime | Ally |

| Limited services | No cash deposits |

| Limited cash deposit locations | Lagging customer service |

About Chime

Chime got its start in 2013 thanks to founders Chris Brett (CEO) and Ryan King (CFO).

Technically speaking, Chime isn’t a bank at all. They’re a financial technology company that offers banking services provided by The Bancorp Bank or Stride Bank, N.A., Members FDIC.

What Chime is, it’s a privately owned company based in San Francisco that focuses on no-fee mobile banking accounts, debit cards, and credit cards. Rather than making money on loans and penalties like other banks, Chime makes money when customers spend money with their cards.

They say that’s all a part of their mission to give everyone financial peace of mind. Chime’s goal is to streamline banking services. They want to make managing your money easy, even if you don’t have much financial experience.

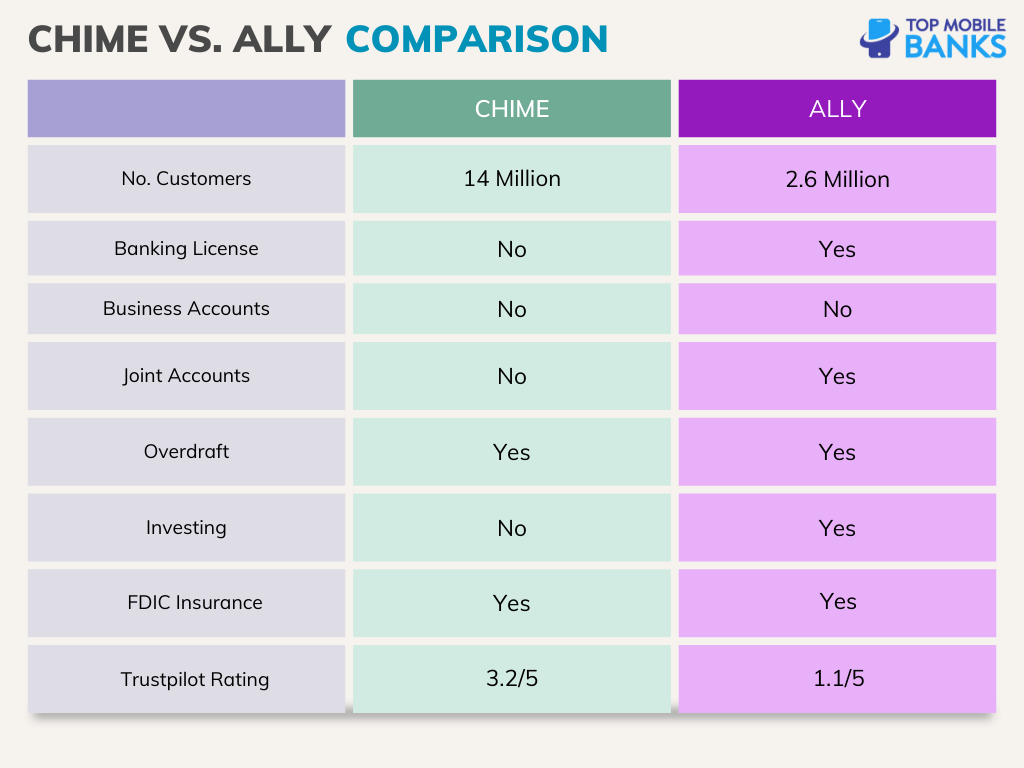

So far, customers seem to be happy with the fintech company because more than 14 million customers already use it. That’s a massive number in less than ten years as a financial startup. It points to the fact that Chime has a lot to offer its clientele.

How to Open a Chime Account

It’s extremely easy to open a Chime account. All you have to do is visit their website or download the app from the Google Play Store or the Apple App Store.

There are no documents that you’ll need to submit. All you’ll have to do is enter your full name, email, address, password, and SSN. These personal details will be enough to open an account and quickly verify your identity.

There are no credit checks, but you have to be a United States resident and at least 18 years old to open a Chime account.

About Ally

Believe it or not, Ally Bank has been around for over 100 years! That’s rare in digital banking, given that online banks need the internet to function.

But Ally bank is different. It didn’t begin as an online bank but rather as a lending institution for the automobile industry.

General Motors Corporation established the bank in 1919 as GMAC (General Motors Acceptance Corporation). GMAC helped dealers finance and maintain their automobile inventories to keep up with growing consumer demand.

During World War II, GMAC’s financing capabilities allowed General Motors to supply submarine engines, airplanes, trucks, and tanks to the Allies.

After the war, the bank continued to finance automobiles and home appliances until the economic recession of 2008.

At that point, GMAC realized the world didn’t need another standard bank. They changed their name and business model, moving into the digital world.

The newly formed Ally Bank made three promises to future customers. They would “do right, talk straight, and be obviously better.”

Today, Ally Bank is a publicly traded company with headquarters in Midvale, Utah. They offer car financing, corporate and personal lending, mortgage loans, vehicle insurance, an electronic trading platform, and, of course, online banking.

How to Open an Ally Account

Likewise, to open an Ally account, all you have to do is visit their website or download the app for iOS or Android phones.

Start by choosing from a “Bank, Invest, or Home Loans” account, or an “Auto Financing” account.

Fees

| ALLY | CHIME |

| No monthly or annual fees | No monthly or annual fees |

| No minimum balance | No minimum balance |

| Free to open an account | Free to open an account |

| No fee for using debit card | No fee for using debit card |

| 55,000+ fee-free ATMs | 60,000+ fee-free ATMs |

| Reimburses up to $10/m for out-of-network ATMs | $2.50 out-of-network ATM fee |

There are hardly any fees with both of these online banks which is an industry-standard at this point and a way to lure customers away from traditional banks that are riddled with fees and charges.

Accounts & Cards

Chime

Chime has a somewhat basic setup consisting of a checking account plus a free Visa debit card that you can use anywhere, including internationally. This checking account has no monthly fees, no minimum balance, and no foreign transaction fees.

Couple that with the fact of how easy it is to open it, and it’s no wonder more than 14 million people are on board already.

Additionally, for those with poor credit scores, the Chime Credit Builder credit card can help improve them. It doesn’t have interest, no annual fees, or credit checks during application. And, critically, once you pay your monthly balance on time, the company will report the fact to the three major credit bureaus.

Lastly, if you already have a Chime checking account, you can open a high-yield savings account with 2.00% APY. You have to fund it directly from your checking account as well.

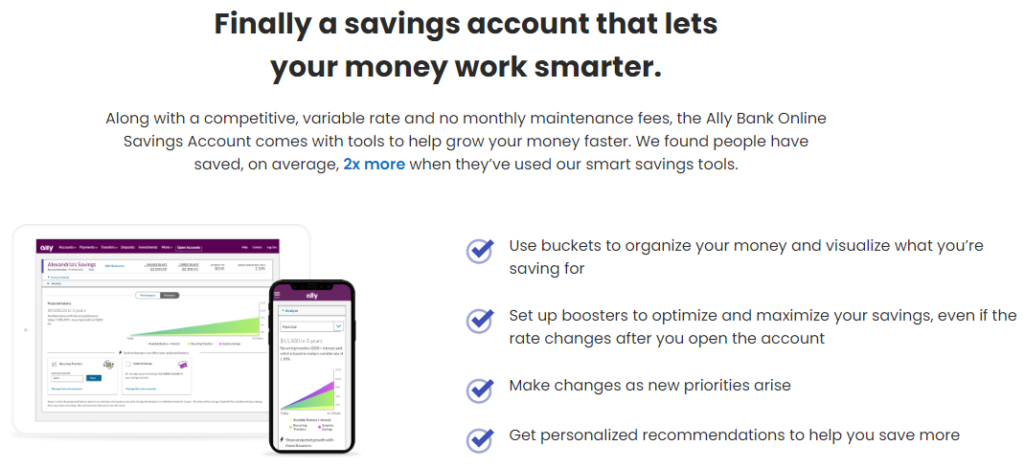

Ally

Ally has many different options when it comes to accounts. Firstly, there’s the Online Saving Account with a 3.00% APY that comes with features such as surprise savings, round ups, buckets, and recurring transfers.

Savings buckets let you create up to 10 separate spaces that coexist and can be dedicated to various themes like travel, home, emergencies, groceries, etc.

Recurring transfers enable you to move money into the savings account on a regular basis.

Round-ups round up your transactions to the nearest dollar. Lastly, surprise savings allow the bank to analyze your linked checking accounts for cash that can be saved on your behalf automatically.

Next, there’s the Interest Checking account that earns you an interest of 0.10% if you have less than a $15,000 minimum daily balance and 0.25% if you have more than a $15,000 minimum daily balance.

An account with even better rates is the Money Market fund. It earns up to 3.00% APY on all balances with no minimum balance requirements.

High Yield Certificates of Deposits (CDs) can earn an even higher interest rate when you lock in your funds for a longer term (12 months+).

There are no minimum deposit requirements, and the APY starts at 1.50%. If you can leave your money for more than 12 months, the APY goes to 4.00%. 18 months and up will lift the APY to 4.10%.

There are two more CDs:

- Raise Your Rate CDs (3.25% APY)

- No Penalty CDs (3.30% APY)

If you need a credit card, Ally has got you covered as there are four different credit card types:

- Ally Platinum

- Everyday Cash Back

- Unlimited Cash Back

- Unlimited Cash Back for Nurses & Educators

Credibility & Security

Chime

Hackers and scammers are plaguing mobile payment apps, and Chime is no different due to how easy it is to sign up for their service. The company is regularly closing accounts in droves leading to many people not being able to access their accounts which lead to controversy.

Apart from that, the company hasn’t had any issues and is known to utilize all the latest security features that guarantee its systems and customer data are safe.

All the funds (up to $250,000) are FDIC insured through Chime’s partner banks, The Bancorp Bank and Stride Bank.

Ally

Ally is a long-standing and well-respected bank with a long and colorful history. It’s also a Member FDIC, and Equal Housing Lender. Additionally, all the funds, except securities products, are FDIC insured for up to $250,000.

Saving

Chime

We already mentioned that Chime offers savings accounts with an APY of 2.00%, which is credited on the first day of the month.

You do have to have a checking account first to open a savings account. However, if you close the savings account for any reason, you can’t re-open it for three months (as per federal law).

There are several ways of depositing money into the Chime savings account:

- Transfer money from the Chime checking account

- Have 10% of your direct deposits transferred

- Round up your transactions to the nearest dollar

In the last case, if your purchase was $9.50, Chime will remove $10 from your account and deposit 50 cents into your savings account.

Ally

We already mentioned Ally’s savings accounts, so I’ll just recap them. There are five savings account types:

- Online Savings

- Money Market

- High Yield CD

- Raise Your Rate CD

- No Penalty CD

Investing

Chime has no investment options at the moment, and I don’t think they have anything planned for the near future.

On the other side, Ally offers an abundance of investment opportunities to its clients:

- Self-Directed Trading

- Robo Portfolios

- Wealth Management

- Forex

- IRAs

The investment options include:

- Stocks & ETFs

- Options

- Bonds

- Commission-free ETFs

- Mutual Funds

- Margin Accounts

- Securities Income Program

The Self-Directed Trading account is a commission-free 24/7 trading platform that lets you make your own investment strategy. Plus, there are no account minimums, and you can even transfer the investment account you have somewhere else. This includes individual stocks or even all your investments.

If you transfer more than $2,500 from another broker, Ally gives you a $75 credit to cover the costs.

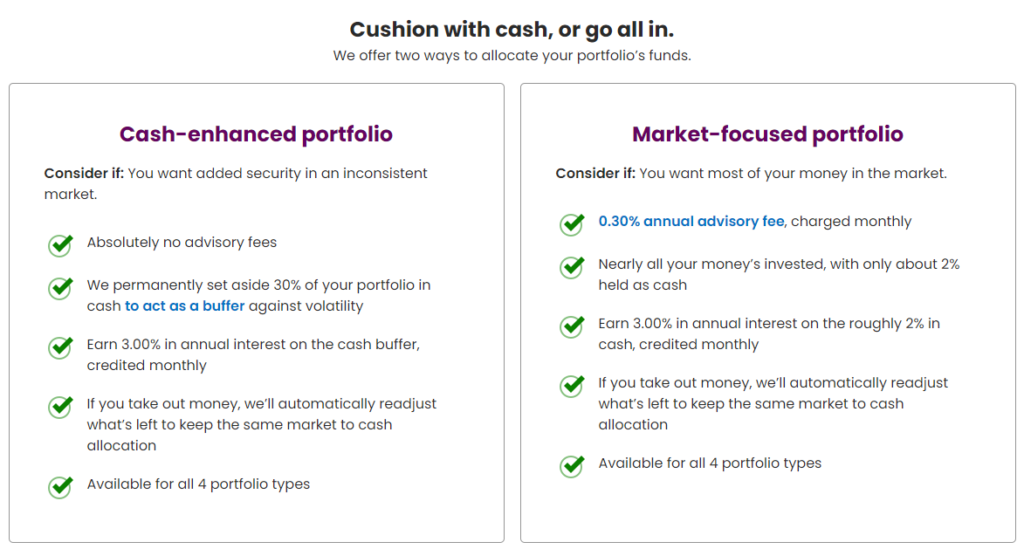

Robo Portfolios were designed by human experts and are managed and monitored daily. You can start investing with as little as $100.

Choose whether you prefer the cash-enhanced or market-focused portfolio. Update your portfolio goals at any time.

There are four portfolios:

- Core (for hands-off investors)

- Income (higher dividend yields)

- Tax optimized

- Socially responsible

Wealth Management lets you invest in the themes, causes, or companies you care about most. You can get one-on-one personalized guidance from a dedicated fiduciary Senior Wealth Advisor if you invest at least $100,000.

The advisory fee caps at 0.85%, which is $71/m for a $100,000 portfolio.

Customer Reviews

Chime

Chime has a somewhat good 3.2-star rating out of 5 on Trustpilot, with 74% of 8,000+ reviewers giving it an excellent mark and 13% a poor one. With this score, Chime is placed better than traditional banks like Bank of America (1.4), Chase (1.3), Capital One (1.2), and Wells Fargo (1.2) but worse than the likes of MoneyLion (4.7), Current (3.8), or Varo (3.8).

Ally

Ally, on the other side, is doing way worse on Trustpilot. They have a meager 1.1/5 star rating from less than 400 reviews. Per this rating, the bank is placed among traditional banks and not digital banks.

People seem to have the most grudges for long wait times to get customer support.

Ally fairs considerably better on the Google Play Store (3.9/5 from 24,000+ ratings) and Apple App Store (4.7/5 from 48,000+ ratings).

Why You Should Choose Chime

Zero Fees

Chime, like most other digital banks, doesn’t charge monthly, minimum balance, or overdraft fees.

There are also no fees for international transactions and ATM withdrawals as long as it’s within their ATM network.

High Yield Savings Account

If you open a Chime savings account, you can avail of a high yield of 2.00% APY. This is much higher than most traditional or even digital banks.

Mobile App

Chime’s mobile app is highly rated (4.8/5 on App Store and 4.6/5 on Google Play). The app functions exceptionally well, based on these reviews by customers already using the app.

Why You Should Choose Ally

Range of Financial Products

Ally offers a wide range of financial products, much more than other digital banks.

There’s an interest checking account, savings account, high-yield CDs, as well as investment products and loans. In this regard, Ally really is a full-service bank that provides all these services without physical locations.

Fees

Just like Chime, Ally has almost no fees. The bank doesn’t demand a monthly maintenance fee, has free ATM withdrawals, has no need for a minimum balance, and doesn’t charge for overdrafts and transfers.

Digital Access

As a truly digital bank, all of Ally’s financial products and services are available via the app and online on the website. There’s no need for physical branches. In addition, customer support is available 24/7, and you can get them via phone, email, or live chat.

Conclusion

Ally offers a far greater range of financial products, which is great if you need them. If you’re looking for simple checking and savings accounts, Chime is for you.