Last Updated on December 8, 2022 by TMB

Traditional banks are notorious for charging high overdraft fees when they overdraw their checking accounts. These fees are costing everyday Americans billions of dollars each year!

Almost all conventional banks, like Bank of America or Chase, for instance, charge an overdraft fee of $35 per transaction that’s made while you’re in a negative balance.

| TRADITIONAL BANKS | OVERDRAFT FEE | DIGITAL BANKING | OVERDRAFT FEE |

|---|---|---|---|

| Bank of America | $35 | Chime | $0 |

| Chase | $34 | One Finance | $0 |

| Regions Bank | $36 | Axos Bank | $0 |

| Fifth Third Bank | $37 | Ally Bank | $0 |

| TD Bank | $35 | Current | $0 |

| KeyBank | $34 | Majority | $0 |

| Truist Financial Corporation | $36 | MoneyLion | $0 |

| Wells Fargo | $35 | Monzo | $0 |

| PNC Bank | $36 | SoFi | $0 |

| US Bank | $36 | Juno | $0 |

Some banks have imposed a limit of 4-6 transactions, but others allow for up to 12 transactions in a day. That means that you could pay $420 ($35×12) in overdraft fees in a single day!

Luckily, digital banks have introduced new models and policies around overdrafts.

Most digital banks allow customers to spend more money than they have in their accounts without paying a fee.

We chose the best digital banks on the market that allow overdrafts without fees.

[lasso rel=”pxf” id=”10713″]

READ ALSO: How Digital Banking Helps You Save Money

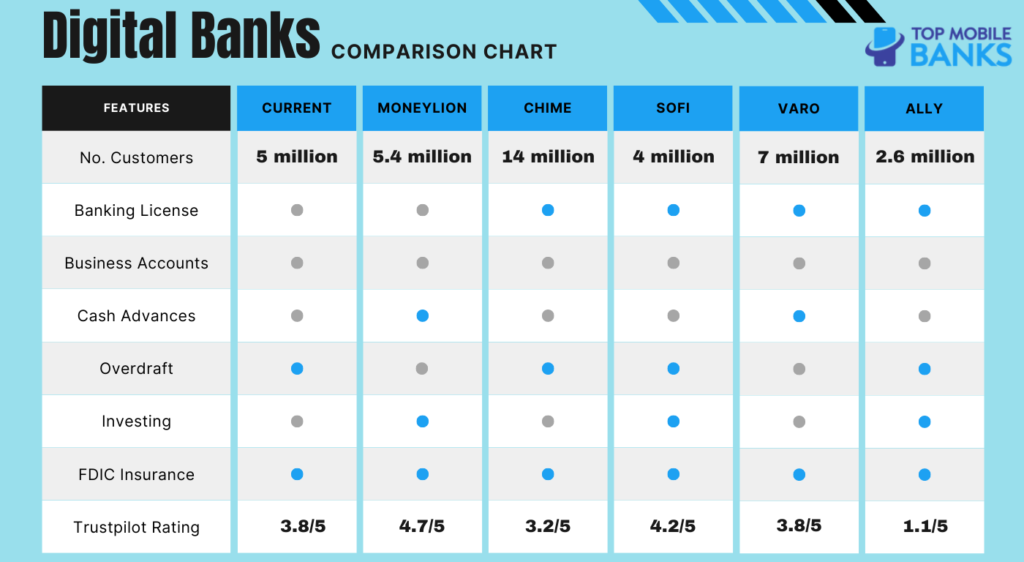

1. Current

- Fee-free overdraft up to $200

- Points and cashback

- Instant Current transfers

- Cash deposits at 60,000 stores

- Free ATM withdrawals

- Gas hold refunds

Current, a digital bank with around 5 million customers, is one of the simplest and best companies in the industry.

They offer a no-frills checking account that has no fees, early payday, cash back, fee-free ATMs, and even teen accounts. All of the features and benefits are now completely free, whereas you had to pay a monthly fee to access the more advanced features and teen banking.

The company also offers savings pods which are basically separate savings accounts. They come with a superb 4.00% APY. Another great thing about these pods is that you can access your money anytime without restrictions or penalties.

Next, there’s a crypto trading platform where you can buy and sell the 27 most popular cryptocurrencies for as little as $1.

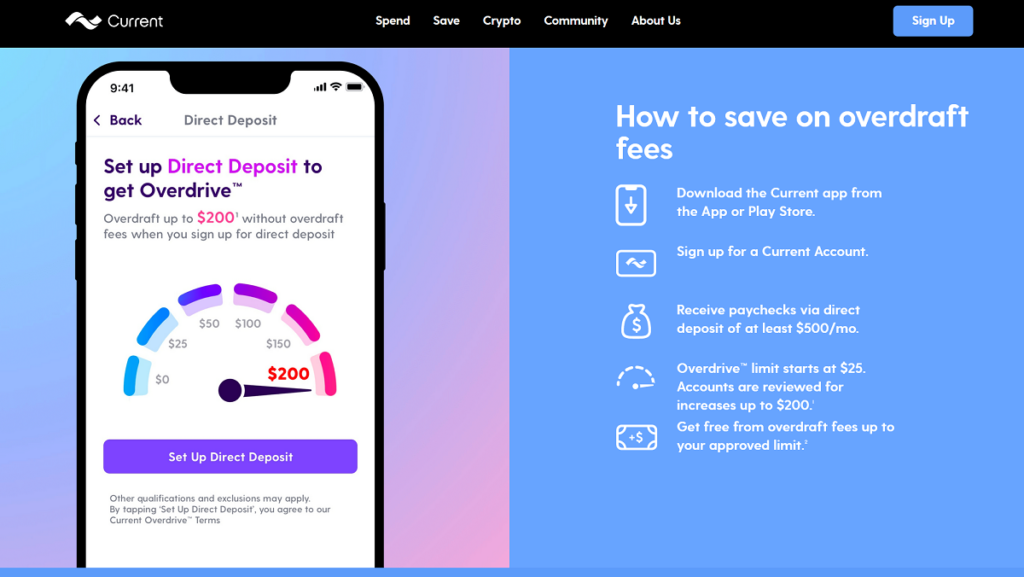

Lastly, and the reason why we’re here, is the overdraft. Namely, Current offers overdraft with no fees for people that receive paychecks via direct deposit of at least $500 per month.

That’s the main requirement. The overdraft limits start at $25 and can potentially increase to up to $200 after your account is reviewed.

The next time you get a deposit into your account, the amount will cover the negative balance.

You need to know that Overdrive only functions with debit card purchases. Transactions such as ACH, Current Pay transfers, checks, and ATM withdrawals don’t apply.

2. Chime

- Fee-free overdraft with SpotMe

- Savings account

- Spending account

- Credit builder

- Two days early paycheck

- 2.0% APY on savings accounts

Chime is one of the most popular digital banks in the US. It was established in 2013 and offers checking accounts at no fee, as well as a high-yield savings account.

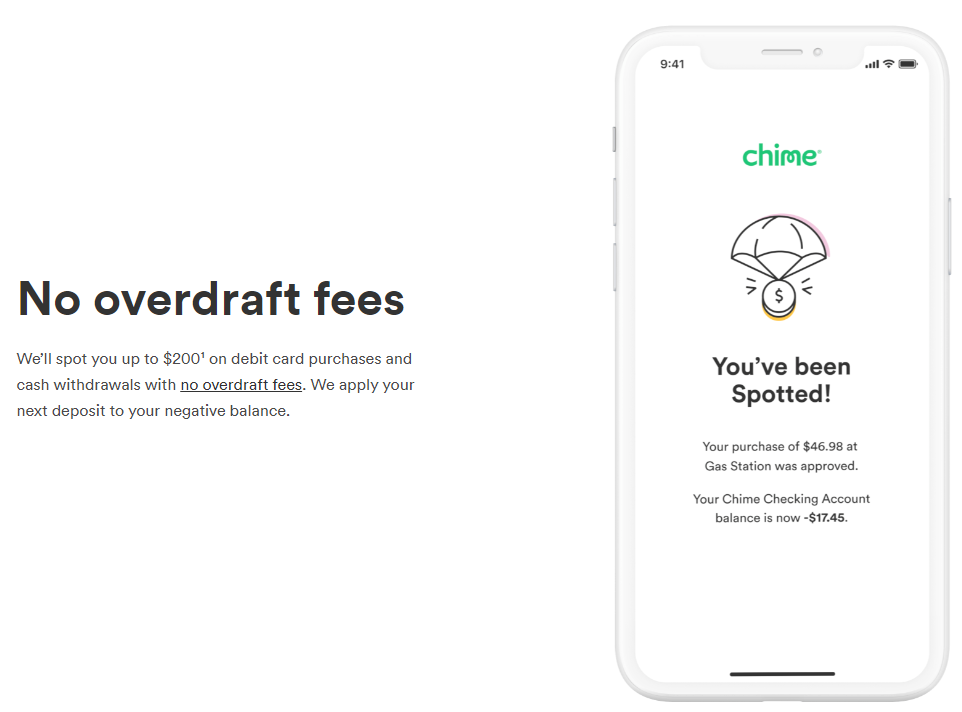

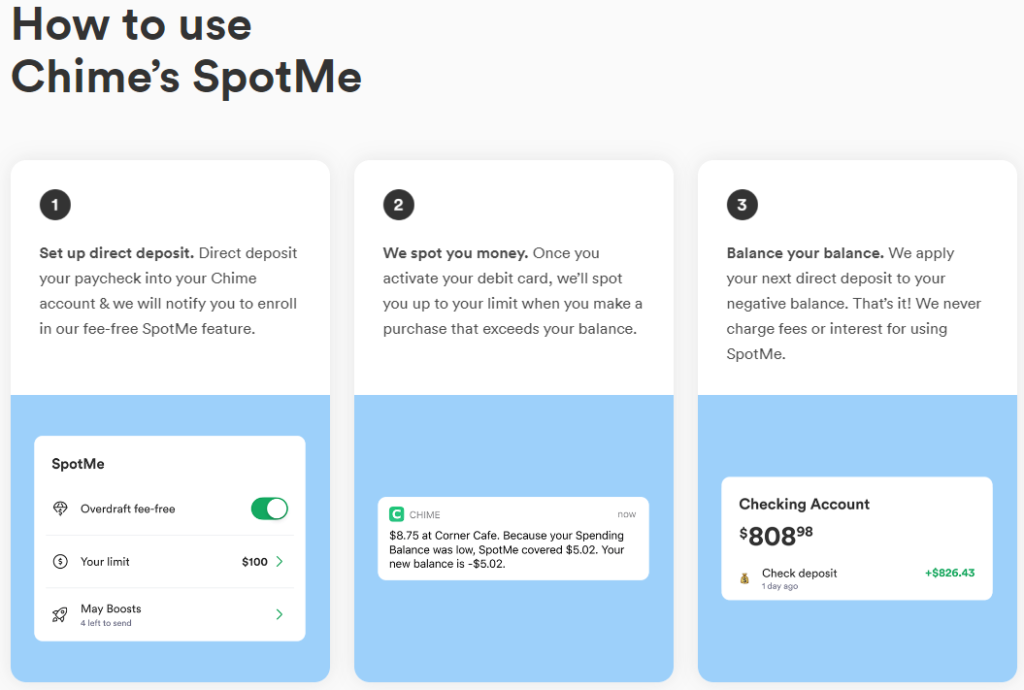

Chime offers its customers overdrafts at no cost via the feature SpotMe. If you need to draw more than you have in your account, the bank will spot you up to $200 on your cash withdrawals and debit card purchases.

To be eligible for SpotMe, you must be a US citizen over 18. You also need to receive a single deposit of $200 or more in your Spending Account 34 days prior and have an activated Chime debit card.

Once you qualify, you can overdraw $20 on purchases and cash withdrawals for a start. The bank will then increase your limit up to $200 based on your account history, spending activity, direct deposit amounts, and frequency.

This limit will be displayed on the Chime mobile app, and the bank will send you notifications when your limit changes.

Although SpotMe doesn’t charge any overdraft fees, you might incur third-party costs with ATM transactions. The feature also doesn’t cover non-debit card transactions such as ACH transfers or Checkbook transactions.

Lastly, Chime provides its customers with a Chime Credit Builder Visa Credit Card to build their credit scores. With direct deposits, you can receive your paycheck two days early, and all your deposits are FDIC insured for up to $250,000.

3. SoFi

- Overdraft protection

- No monthly fees

- Saving, spending, and investing accounts

- Loans available

- Credit score and budgeting assistance

- Access to thousands of fee-free ATMs

- Mobile deposits

- Cash deposits and withdrawals

- Financial and estate planning

- Career counseling

SoFi is more than a digital bank. It’s a one-stop shop for your finances. It offers everything from checking and savings accounts to personal, student, auto and mortgage loans, as well as credit cards, insurance, and investing.

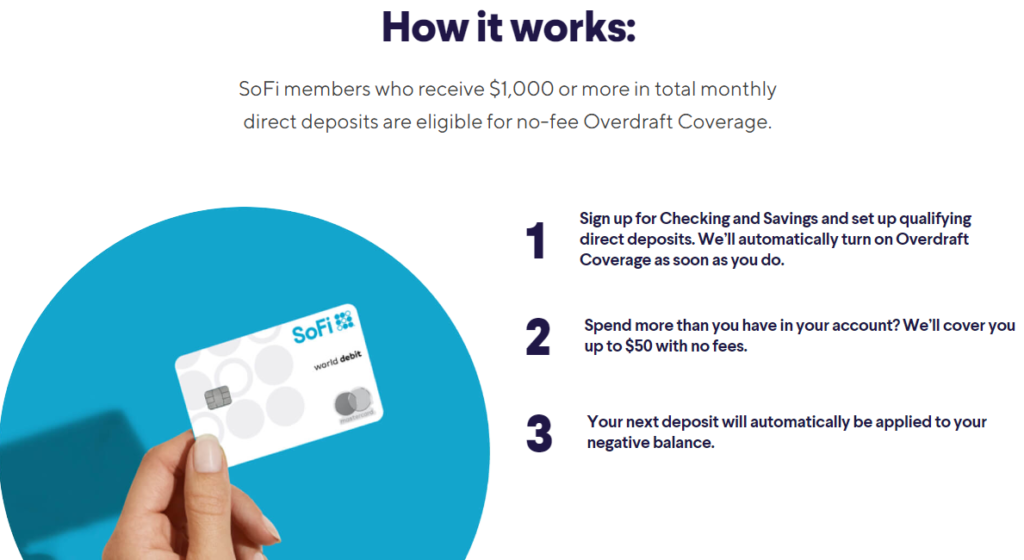

Of course, SoFi also has no-fee overdraft coverage. The company will cover you up to $50 if you’re bound to go into overdraft.

You will have to have a SoFi checking and savings account and set up direct deposits. You’ll also have to receive $1,000+ in total monthly direct deposits.

4. Ally

- No overdraft fees

- Overdraft Transfer Service

- Checking account

- Savings account

- Free ATM withdrawals

- 1.50%-4.10% APY with a High Yield CD

- 3.00% APY on savings account

- Personal loans and mortgages

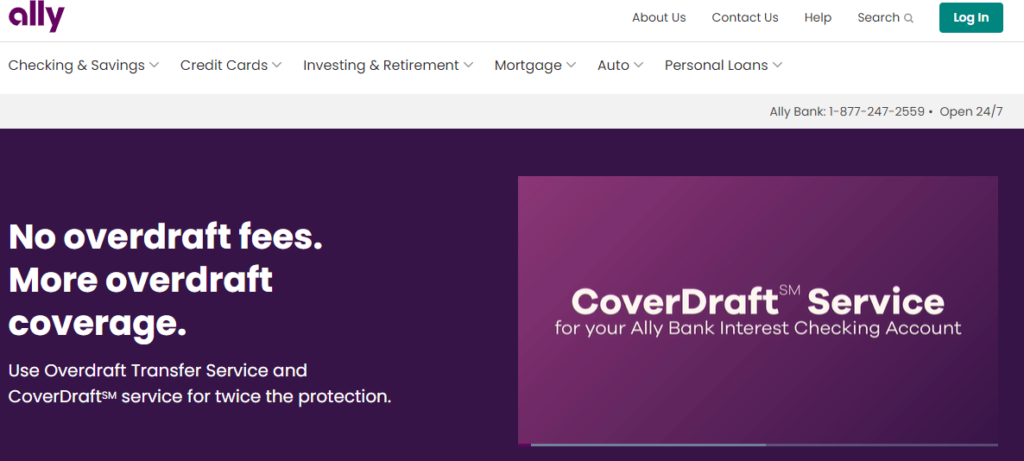

Ally is one of America’s biggest digital banks. The digital-only banking division of Ally Financial Inc. offers its customers at no fee for all types of accounts. Every Ally Bank customer is eligible, and they have no restrictions.

If you don’t have enough money in your account to cover a transaction, you can get overdraft coverage once you sign up for the Overdraft Transfer Service.

This service automatically transfers available funds in $100 increments from your savings account or money market to cover your purchases.

Ally will move these funds to your checking account at no fee. Also, keep in mind that if you don’t set up this Overdraft Transfer Service and your card is declined, the bank will not charge you an overdraft fee.

You can sign up for this service by logging into your account and selecting the linked account you want to transfer funds to.

Apart from the checking account services, Ally also offers high yield certificates of deposit (CDs), mortgages, home loans, individual retirement accounts (IRAs), and investment advisory services through Ally Invest.

READ NEXT: 6 Reasons Why Digital Banks Are The Future Of Banking

5. MoneyLion

- $250 fee-free overdraft

- Early paycheck

- Zero ATM fees at Allpoint

- Price protection

- Rewards on spending

- $19.99 /mo Credit Builder Plus

- $1,000 Credit Builder loan

- ETFs investing

Next up on our list is MoneyLion. One of the best-rated digital banks on Trustpilot with an amazing score of 4.7/5 from around 28,000 reviews.

So, why is this excellent bank in the last place on this list? It’s because they don’t really offer overdrafts. However, they don’t have any overdraft or overdraft protection fees as well. If you don’t have enough funds in your account, your transaction will simply get declined.

On the other side, if you are strapped for cash, MoneyLion offers free cash advances of up to $300. To get cash advances, there are no credit checks, no monthly fees, and no interest or other charges.

To become eligible for cash advances, all you have to do is link your checking account. First, you’ll only get up to $25, but if you have recurring deposits in your linked external account, you’ll unlock $50 – $250.

And if you get direct deposits into your RoarMoney checking account or start using the credit builder program, cash advances go up to $300.

6. Varo

- Early direct deposit

- No monthly fees

- Checking account

- Debit card

- Savings account

- Early Direct Deposit

- $100 Instant Cash

- Free ATM Withdrawals

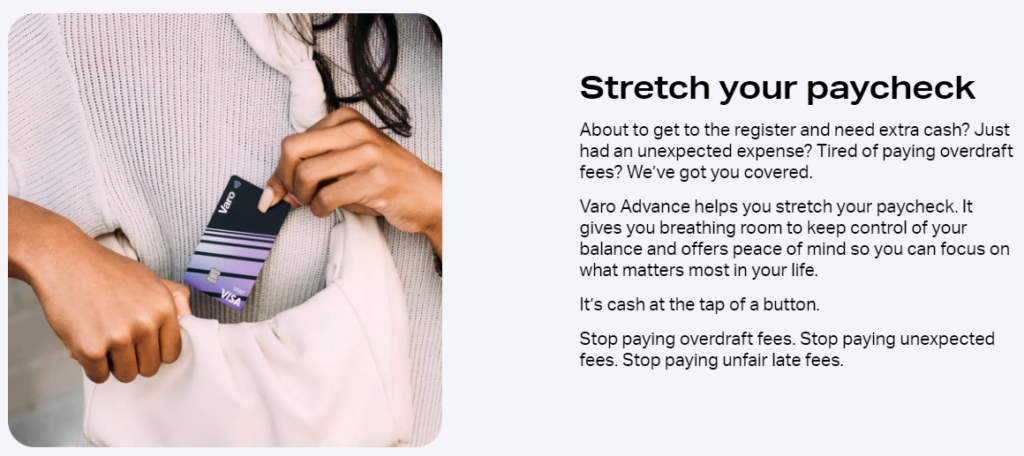

And, last but not least, we have Varo – the first digital bank in the US to get a banking license.

Varo also doesn’t offer overdrafts per se but, similar to MoneyLion offers cash advances. However, to use cash advances, you don’t have to go to $0 on your account. You can get up to $100 whenever you need it.

There are some requirements, though:

- Your Varo account has to be older than 30 days

- It needs to be active

- You need to have $1,000+ in direct deposits in the last 31 days

Getting $20 is free. If you need $50, for example, you will have to pay $3. For $75, $4, and to get $100, you’ll need to pay back $5 more.

RELATED: Cash App Overdraft (Is It Available?) Plus 4 Alternatives

Overdraft Protection Vs. Overdraft Coverage

Banks have found innovative ways to provide overdrafts to their customers. To make the service better, they offer either overdraft protection or overdraft coverage. As a customer, you also need to distinguish between the two features.

For both overdraft services, the bank will not automatically sign up. You have to opt-in for either of these services on your checking account to give permission to the bank.

Overdraft Coverage

With this feature, the bank will advance you cash to make a purchase when you don’t have sufficient funds in your checking account. In some cases, the bank will increase your limit depending on your account history.

Overdraft Protection

On the other hand, you can link your checking account to another account with funds such as savings or money market funds with overdraft protection. The eligible funding account differs depending on the specific bank.

In this alternative, if you don’t have enough funds in your checking account, the bank will transfer cash from your linked account to pay for the purchase.

How to Avoid Overdraft Fees

If your account always runs into low balances, here are a few tips to avoid overdraft fees.

Switch Banks

If you have accounts in a bank that still charges overdraft fees, especially the traditional banks, you can switch to a digital bank with better or no fees.

Most digital banks will not charge you a monthly maintenance fee or an overdraft fee and will offer some form of coverage and protection. Therefore, you don’t have to stick with an expensive bank, as there are other cheaper alternatives.

Track Your Account Balance

The simplest way to avoid paying any overdraft fees is by watching your account balance closely.

Digital banks provide all the services via their websites or mobile apps, making it easy to track your spending and balances on the go.

Use the available online banking tools to your advantage to ensure your account doesn’t run into a negative balance.

Link Checking Account to Savings Account

If your bank has this alternative, you can link your checking account to the savings one. This way, the bank can transfer funds when you are running low on cash and need to purchase.

Also, ensure your savings account has enough money to cover the necessary expenses.

Set up Bank Notifications

Another way to monitor your account and spending is by signing up for alerts and notifications via email or mobile apps.

You can set up a low-balance alert to keep you in the loop about how much money is available in your account.

Once you notice your funds are low, you can deposit more cash, minimize spending or cancel some payments in advance.

Avoid Overdraft Protection

According to federal law, banks can’t sign you up for overdraft protection unless you opt in. Therefore, if you don’t sign up when opening your checking account, your card will only be declined when you withdraw cash or make a payment with insufficient funds.

Conclusion

Digital banks are way ahead of traditional banks in terms of fees and simplicity but also overdrafts. Charging overdraft fees means preying on the most vulnerable members of our society.

Not only are overdraft fees unethical, but they’re also cruel, and it’s no wonder digital banks have no such fees and even offer overdraft protection as well as cash advances.

We covered some of the best digital banks on the market, and they, too, offer overdraft protection or cash advances.