Last Updated on January 29, 2023 by TMB

We are in the midst of a digital transformation of many industries, but the banking and financial industries, in particular, are going through major changes that will affect billions of people worldwide.

You could say that this all started with the rise of the internet, and you wouldn’t be wrong. It was a gradual and natural process going in line with the advances in technology, smartphone penetration in the general population, and ever-changing regulation that has tried to keep up with advancements.

Terms that were almost non-existent just a decade ago are now part of our everyday language. I’m talking about fintech and digital banking, of course.

There’s almost a hundred percent certainty that you have used products or services from not just one but many fintech companies. Because you are reading this, there’s also a big chance that you have used online, digital, or mobile banking too.

However, let’s see in detail and in plain language what the distinction between the terms fintech, digital banking, and online banking is. With well-known companies as examples, everything should sit in place after you’re finished reading the article.

What Is Fintech?

Financial technology, or fintech for short, is a broad term describing many aspects of using technology to bring financial services such as payments, lending, banking, money transfers, and investing (just to name a few) to end consumers.

Many companies that started out only as technology companies have transitioned into fintech in recent years because adding financial services to their applications, platforms, products, or services made perfect sense from the standpoint of user experience, customer service, and, of course, revenue.

The beauty of fintech is that almost any industry or business, whether they’re tech or not, can use the services of fintech companies to add financial features to their existing business.

Fintech competes with traditional methods of banking, lending, payments, insurance, and other financial services and financial products.

A fintech company can offer one or more of these services to end consumers (B2C) or to other businesses (B2B). They can also offer a whole platform as an almost turnkey solution to aspiring businesses.

A great example of this is Banking as a Service (BaaS), where a fintech company offers everything needed to start a digital bank or to add a financial product to one’s portfolio of other services.

Fintechs can also be categorized into seven categories:

- Payments

- Money Management

- Crowdfunding

- Crypto

- Lending

- Insurance

- Robo-Advising

READ ALSO: The 19 Biggest Fintech Companies In The World

What Is Digital Banking?

Digital banking is much more than merely offering banking services online (that’s online banking). It’s the digitization of traditional banking to the point that digital banks don’t have physical branches because neither they nor their customers need them.

And while online banking is a product of incumbent banks as their way of modernizing their banking business while still keeping branches nation or worldwide, digital banking is led mostly by fintech companies to simplify this age-old industry and make it more accessible.

Digital banks can be founded by fintech companies or existing banks but through a separate entity and app. To open a digital bank, a company, in most cases, doesn’t have to have a banking license (depending on the country and its regulations) but can be regulated as an e-money institution that issues cards and offers other services and products through a third-party company or bank.

Many digital banks have tens of millions of users and are spanning dozens of countries, especially in Europe, where the market is unified and open.

Difference Between Fintech And Digital Banking

Fintech is a much broader term than digital banking. It encompasses not only digital banks but also singular services such as payments, international transactions, lending, digital wallets, crypto-investing, buy now, pay later, and much more.

A fintech company can be a digital bank, but a digital bank doesn’t have to be a fintech. It can be a regular bank as well that is implementing fintech’s services or platforms.

There are tens of thousands of fintech companies as of 2021:

- North and South America: 10,755

- Europe, the Middle East, and Africa (EMEA): 9,323

- Asia Pacific (APAC): 6,268

On the other side, there are far fewer than a thousand, most people would say even fewer than 500 digital banks in the world.

Fintech Examples

With so many fintech companies worldwide, there are bound to be many excellent examples. And that’s true. There are so many great fintech examples that I could list here.

Just like digital banks, fintech companies mostly begin as startups looking for a quick expansion and millions in venture capital to fuel their unlimited growth.

Profitability is often at the back of the mind of these companies as they are seeking to onboard thousands of users daily. Luckily, the investors don’t care about profitability at this stage as it’s all about the future potential and waiting for a profitable exit once the company hits IPO.

Stripe

Stripe is one of the most highly valued startups in the world. It’s a fintech behemoth that changed the world of payments with seven lines of code.

Patrick and John Collison, brothers from rural Ireland, founded Stripe in 2009 and developed a hit product for Silicon Valley startups. Their payment platform could suddenly be found plugged into the websites and apps of thousands of companies.

Fast forward to today, and the amount of businesses, small and big, that are using Stripe is staggering. Millions of businesses are using Stripe’s software and APIs to accept payments, send payouts, and manage their businesses online.

Stripe is a special fintech because it makes moving money seamless and borderless. 90% of US adults have bought something from a business that’s using Stripe. The platform supports more than 135 currencies.

Stripe’s use cases are so broad that they cover the following:

- SaaS

- Platforms

- Marketplaces

- Ecommerce

- Creator Economy

- Crypto

- Embedded Finance

I have successfully and quickly integrated Stripe into several types of my own businesses, either directly or through third-party apps and plugins, and I can tell you, it couldn’t be easier and faster.

As you can see, Stripe serves some of the biggest companies in the world, but if you open an e-commerce store yourself, you could also use its services, as the company doesn’t shy away from small businesses.

The company’s valuation was $9 billion in 2016, $36 billion in 2020, and a staggering $95 billion in 2021. Recently, however, the company had to scale back its valuation to “only” $74 billion.

The latest valuation is in line with the tech companies’ downturn in 2022.

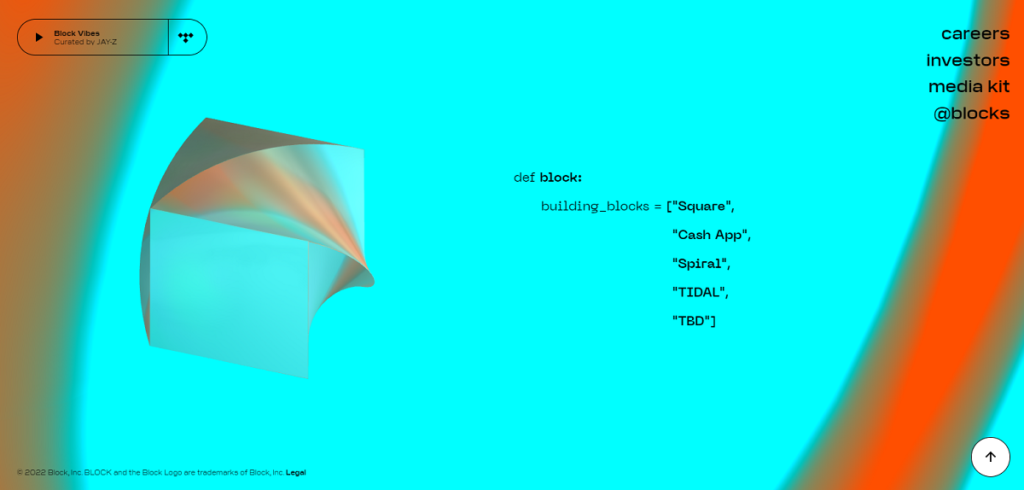

Block

Block, Inc., formerly known as Square, Inc., is the brainchild of Twitter founder Jack Dorsey, as well as Buzz Andersen and Jim McKelvey.

Block is a well-known financial services, digital and mobile payments, and merchant services aggregator company from San Francisco.

The fintech company has several popular brands in the P2P and business payments, streaming, and crypto space. The companies include:

- Square

- Cash App

- Tidal

- Spiral

- TBD

Cash App and Square are definitely showrunners with tens of millions of business and personal users.

Cash App is a digital banking and mobile payment app popular among young people for its fast and free money transfers as well as for its stock and bitcoin investing.

Block is the perfect example of a fintech that is at the same time much more than a digital bank. It’s an ecosystem of apps serving people and businesses that seek to manage their money, stream music, or learn and invest in bitcoin, blockchain, and emerging technologies.

Digital Bank Examples

There are plenty of digital banks out there, and most developed and emerging countries already have a healthy number of digital banks on the market, shoulder to shoulder with traditional banks.

We already mentioned that digital banking is a bit different than online or mobile banking. Digital banks are mostly startups looking to disrupt the stale banking markets with millions of unsatisfied customers.

What digital or challenger banks are looking to do is to offer completely free or low-cost checking and savings accounts with higher savings interest rates than what incumbent banks are offering, and with a much-improved user interface and often, but not always, better customer service.

In fact, it is this last point that is the worst part of digital banking. As these startups are gaining millions of users in a short time span, they are slow to keep up with the demand for customer service. Once they sort this out as well, there will be no stopping them.

READ ASLO: 6 Ways Digital Banking Helps You Save Money

Revolut

Revolut is a challenger bank from the UK that has expanded worldwide since 2015 and has more than 18 million personal and 500k+ business users.

The company raised $800 million in July 2021, giving it a valuation of $33 billion. That’s a 6x valuation since their last funding round in 2020.

Revolut is both a fintech and a digital bank that offers bank accounts, virtual and debit cards, interest-bearing “vaults”, as well as commission-free crypto, stock, and commodities trading.

The company started as an app and a prepaid card but soon became a household name by enabling people to spend abroad without paying high foreign exchange fees, transfer money to other users for free and instantly, and manage money with its advanced budgeting and analytics side of the app.

All of these features launched them into the digital banking stratosphere, and Revolut became UK’s first digital banking unicorn in April 2018.

Revolut is now offering a financial super app that allows its users to sign up for a plethora of banking, insurance, travel, and investing means.

Alongside dedicated investing apps like Robinhood, Betterment, Acorns, Degiro, and others, Revolut has popularised investing in stocks, commodities, and cryptocurrencies.

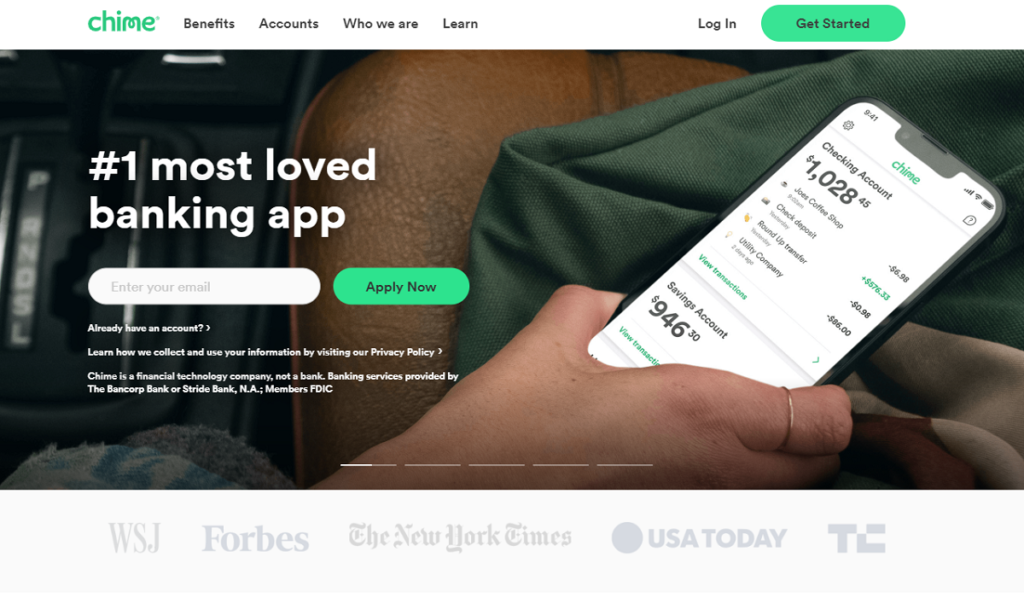

Chime

Chime is a challenger bank from San Francisco that was founded in 2013. By many reports, it’s the largest challenger bank in the US, with more than 12 million users in 2021. Of that, nearly 8 million use Chime as their primary bank account, something that many digital banks struggle with. Additionally, Chime is predicted to reach 22+ million users by 2025.

For that reason, Chime is another great example of a digital bank that’s done many things right. First of all, it has been focusing on unbanked and underbanked people in the US that were having trouble opening a traditional bank account.

Second, it has been helping people get on track with their credit score with the Credit Builder Program. The program in question is basically a free credit card that resorts all your successful balance repayments to the major credit bureaus in the country and thus helps your credit score reach new levels.

Also, like other successful digital banks, Chime has offered a no-fee checking account, a high-yield savings account, and the ability to get paid early, as well as to send and receive money instantly for free.

Online Bank Example

As we already mentioned, digital banking is different than online banking. While digital banking accounts are mostly coming from fintech companies, online banking accounts are merely an extension of existing brick and mortar banks that have digitized their offline banks.

Here’s an example of a successful transition into online banking by one of the most well-known traditional banks in the US.

Bank of America

Bank of America is the second-largest bank in the United States (after JPMorgan Chase) and the eighth-largest bank in the world.

The pandemic really made people use digital banking channels more than ever, and BoA is no different. In fact, a whopping 70% of its personal and business users used the BoA online and mobile banking arms to fulfill their banking needs.

It’s no surprise since BoA’s award-winning online and mobile banking are easy to use, the information about fees and rates is relatively easy to find, and you can easily pay bills, deposit checks, transfer money, track rewards, and monitor all your accounts, including Merrill’s investment account.

What sets BoA online and mobile banking from similar products is its virtual assistant, Erica. Erica is basically a chatbot that can help you easily do your day-to-day banking, do all of the above, and more by interacting like you would with a real bank teller.

Ask questions or give directives via voice commands, texting, or tapping options, and Erica will, for instance, lock/unlock your card, find past transactions, send money to your friends and family, view bills and schedule payments, etc.

However, although BoA offers all these advantages, the underlying fact remains – Bank of America is still very much a traditional bank with high fees and lousy savings rates.

How Do Fintech Companies Make Money?

Fintech companies in the early stages usually aren’t profitable, but they do make money. If they have plenty of users, they can charge them a subscription or membership, show them ads in the app, or even sell users’ data to third parties.

They can also sell their product to other companies to be implemented in their apps, websites, or platforms via APIs. Another way is to sell licenses and code.

Many of the digital banking ways of making money that you will read below are also legitimate ways of earning money for fintech companies in general.

How Do Digital Banks Make Money?

Most digital banks are under ten years old, and many are under five. And although profitability isn’t the main concern, making money is.

Just like fintech companies, digital banks make money in various ways:

- Raising funds from institutional investors

- Getting interchange fees

- Offering premium accounts

- Offering SME accounts

- Extending credit cards

- Having loans and mortgages

- Charging overdraft fees

- Providing a marketplace

Raising money was perhaps the “easiest” way to make money when interest rates were historically very low. Venture capital firms were, and still are, lining up to invest in digital banks not only in the United States or the UK but worldwide.

Major challenger banks have been able to raise more than a billion dollars and sometimes even several billion.

Digital banks have accounts that are free of charge, and most of the day-to-day financial services are free, including ATM withdrawals, money transfers, card and app transactions, debit cards, and monthly maintenance fees.

For 90% of people, this is all they need. And it’s all for free. But there is a hidden fee. Well, it’s hidden from users, not from retailers and merchants. It’s the interchange fee that Visa and Mastercard charge sellers whenever a customer buys something from them with the card.

This small fee is charged to them and not us, the digital bank users. By doing this, digital banks can still make good money even though they aren’t charging their clients for almost anything.

It’s also why you often see “mom and pop” shops that only accept cash. Their margins are already razor-thin, and they can’t afford to share money with card companies.

Conclusion

Digital banks and fintech companies are very often overlapping; however, there are subtle differences between them. Fintech companies often focus on a single or several financial services that they offer to end users or other companies.

Digital banks have a more complete financial product that they offer via a digital banking app to personal and business clients.

Both are relatively new innovations hailing from the rise of the internet and smartphones, and in recent years, the pandemic that caused businesses and everyday people to digitalize very quickly.