Last Updated on January 29, 2023 by TMB

- Can I Deposit a Check That’s Not in My Name?

- Can I Mobile Deposit a Check That is Not in My Name?

- Can Someone Deposit a Check For Me Without My Signature?

- What If Your Bank Doesn’t Allow Someone Else’s Check Deposits?

- Should You Deposit Someone Else’s Check On An ATM?

- How Do Criminals Cash Stolen Checks?

- Conclusion

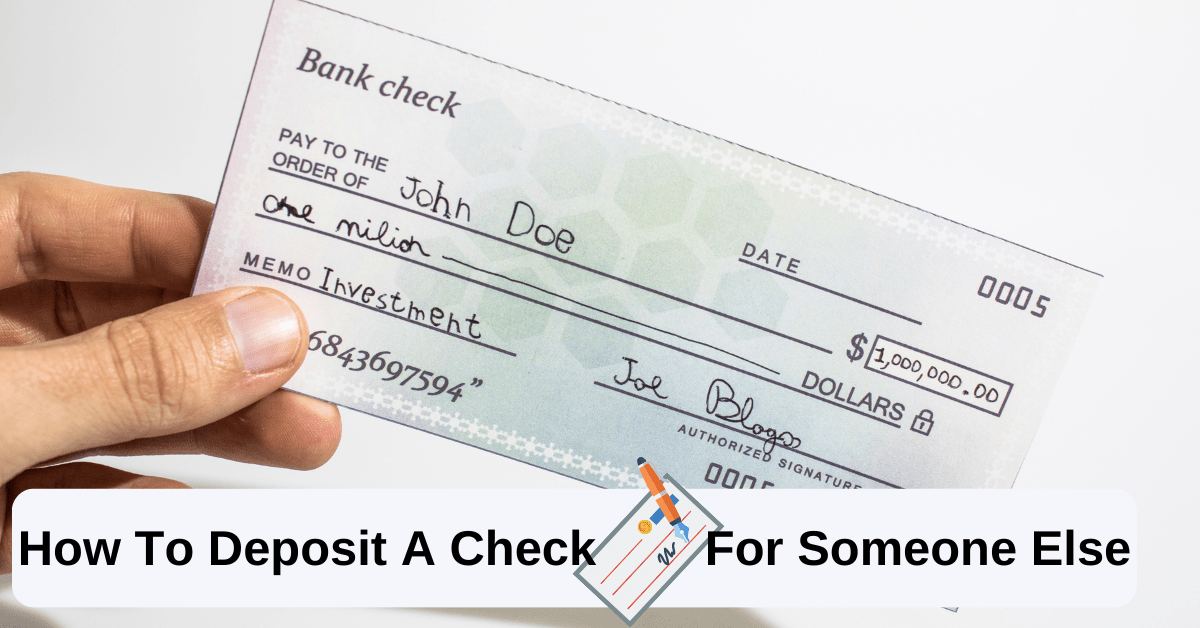

Endorsing and depositing checks doesn’t have to be complicated, especially if you need to deposit a check for someone else or they need to deposit your check.

To deposit someone’s check into your account, they will have to write “Pay to the order of: Your Name” and sign their name underneath the check.

To deposit someone’s check into their account, they will have to write “For Deposit Only” on the back of their check, with their account number and signature.

Another method of depositing someone else’s check into their account is to use a deposit slip and write their account information on it, and sign the back of their checks.

Before doing any of the above, you should confirm with the institution in question that they allow it. Only after you’ve confirmed it, proceed with the procedure.

Always ask for the receipt from the bank or institution that proves and confirms that the funds were indeed deposited correctly in the right account.

[lasso rel=”pxf” id=”10713″]

Can I Deposit a Check That’s Not in My Name?

As we just explained, it really is possible to deposit a check that’s not in your name. This can, however, depend on the institution. To make sure everything goes smoothly, ask the customer services agent whether it’s allowed and how to do it properly. That way, you won’t ruin a perfectly good check.

Can I Mobile Deposit a Check That is Not in My Name?

If you can’t or won’t go to the local bank branch, you can use your smartphone to deposit a check.

The best way to mobile deposit a check that’s not in your name is, in fact, for the person to deposit the check into their account and then transfer the money over to you.

That way, there won’t be any complications for either of you.

Can Someone Deposit a Check For Me Without My Signature?

To not run into problems, the safest way of depositing a check is to have it endorsed (signed).

Even if the bank, for example, accepts the check without a signature and the amount is deposited into the correct account, the bank could still reject the check in a week or two, and you’ll get the money and fees taken out of your account.

What If Your Bank Doesn’t Allow Someone Else’s Check Deposits?

In case your bank doesn’t allow depositing checks for someone else, you can go to check-cashing places that are dedicated to cashing checks for a (hefty) fee.

Usually, people that don’t have bank accounts use them. They are also good for after business hours if you’re in an emergency.

In all other cases, the fees are simply too high for people to use them regularly, especially if you have other ways of cashing checks.

We already mentioned mobile check deposits as an easy, fast, and free alternative. All the major banks, such as Wells Fargo and BofA, have the ability to do so, as well as digital banks like Chime, Cash App, or Venmo, for instance.

Credit unions are a viable alternative only if you’re a member of one. In that case, you can go to many other credit union branches as well if they participate in the scheme.

The check-issuing bank should arguably be your first stop when trying to cash a check. The main reason is that the bank clerk can check in the system whether there’s enough money in the corresponding bank account to cover the check.

After that, you can generally get the money immediately. However, if you also don’t have an account in this bank, you will have to pay a fee.

Should You Deposit Someone Else’s Check On An ATM?

Although ATMs are usually very handy and fast, in this case, we can’t recommend them. The process is completely automated and, therefore, prone to errors and mistakes.

This can result in checks not getting cleared and you having to wait additional time and having to pay a return fee.

You also can’t consult with the ATM to see what it has done and the bank might have limited information on it as well.

How Do Criminals Cash Stolen Checks?

Criminals are very savvy when it comes to cashing stolen checks. It’s no wonder banks take all these precautions.

Most businesses don’t even accept checks anymore because they’re unreliable and expensive to handle.

Criminals have been targeting paper checks as soon as they appeared in general use. However, the internet really made it easy for them to find buyers for stolen checks.

Indeed, there’s usually one criminal organization that does all the stealing and another that buys those stolen checks, alters them, and commits bank fraud.

The price of a stolen check ranges from $175 for personal checks to $250 for business checks! The transaction is done in bitcoin, of course.

The stolen check is then altered. The payee’s name is removed with nail polish remover and replaced by some other name, usually a retailer. The amount is also changed to a much higher amount.

The check is then cashed at a retailer like Walmart using a fake ID.

The problem with stolen checks is two-fold. Not only can the criminals defraud the bank, but they can also steal a person’s identity to generate fake IDs and passports, apply for loans, credit cards, and benefits, access the target’s bank account, or engage in other types of scams.

Conclusion

It’s surprisingly easy to deposit a check for someone else. They can therefore do it to transfer your check as well. All that is needed is a signature and a simple message depending on what you’re trying to accomplish.

To deposit someone’s check into your account:

- The payee has to write “Pay to the order of: Your Name” + their signature

To deposit someone’s check into their account:

- The payee has to write “For Deposit Only” on the back of their check + account number and signature