Last Updated on November 29, 2022 by TMB

Today, we’re having a closer look at two popular Canadian digital banks – KOHO and EQ Bank. They’re very different, as you’ll see. But first, here’s our short verdict.

Comparing KOHO to EQ Bank is like comparing apples to oranges. While KOHO offers a cash back debit card and spending and savings account in one, EQ Bank offers only savings and investing accounts with no debit cards or ATM withdrawals.

Both are digital banks but are focused on different kinds of clients.

Pros & Cons

Pros

| KOHO | EQ Bank |

| Early payroll | No monthly fees |

| Budgeting tools | $200,000 maximum deposit |

| A choice of different card designs | Good interest rates |

| Cashback | Free transfers and bill payments |

| Credit builder | Cheap international transfers |

| Free ATM withdrawals | CDIC insured up to $100,000 |

Cons

| KOHO | EQ Bank |

| Unresponsive customer support | No spending account |

| Deposits aren’t CDIC insured | No debit card |

| No ATM withdrawals |

About KOHO

KOHO is a fintech company from Toronto, Ontario, that was established in 2014. The mobile banking app was launched in 2017 and is a popular alternative to traditional banking accounts.

KOHO is partnering with Visa and Peoples Trust Company to issue the cards and hold the clients’ funds. This is a streamlined way for fintech companies to offer financial products without having to obtain a banking license.

How to Open a KOHO Account

Digital banks make it inherently easy to open an account, and KOHO is no different. To open your KOHO account, go to Koho.ca, enter your email and password, and sign up for a personal, joint, or both account in five minutes. Or download the app.

About EQ Bank

EQ Bank is powered by Canada’s challenger bank, Equitable Bank. Equitable was founded over 50 years ago, and it manages over $47B in assets.

Since its founding, the bank has become the seventh-largest independent Schedule I bank in the country that serves more than a quarter-million Canadians.

With years of experience, Equitable launched EQ Bank in 2016 as the first digital bank in Canada. Today, EQ has over $7 billion in deposits and continues to provide innovative banking solutions to Canadians.

How to Open an EQ Account

You can open an EQ account by going to their website or downloading their app from Google Play Store or the Apple Store. You’ll have to give all the usual personal details such as name, email, address, SIN, and you can choose a password and recovery questions.

You’ll also be able to link your other bank accounts at that point. And that’s it, basically.

Accounts & Cards

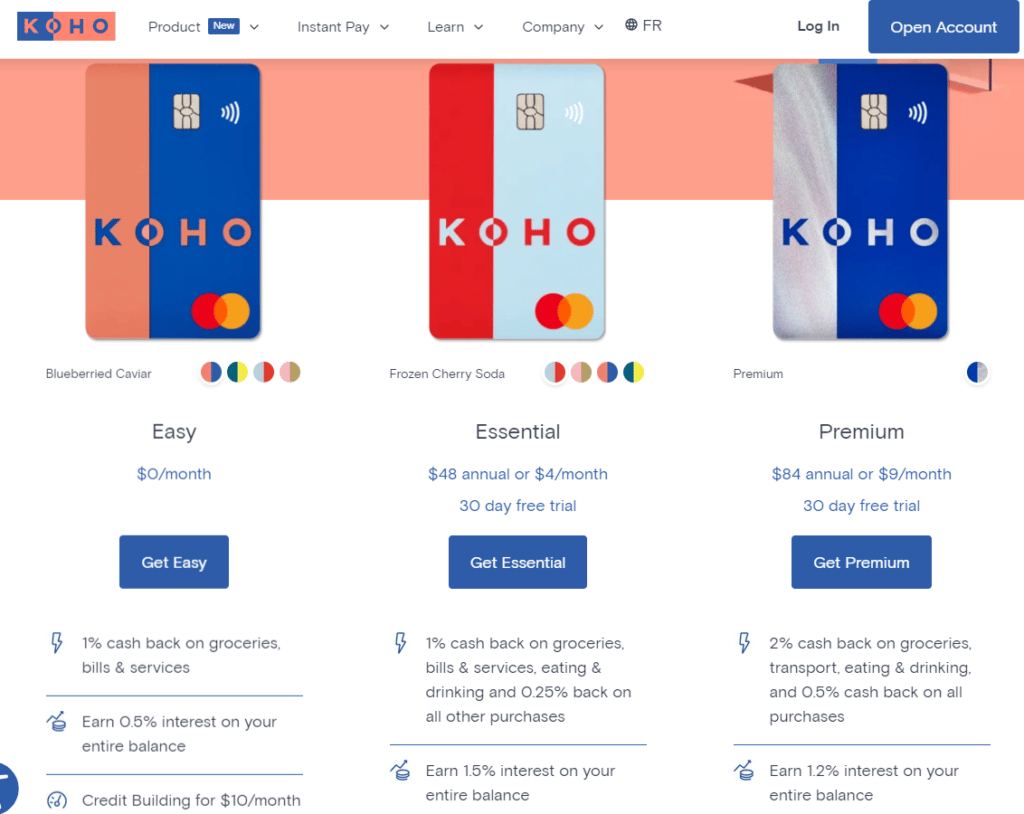

KOHO

KOHO offers three different account types:

- Easy (free)

- Essential ($4/m)

- Premium ($9/m)

To be frank, there aren’t many differences between the accounts. It’s mainly down to what percentage of cashback you’re getting, as well as how much interest you’re earning.

The so-called Easy account offers a 1% cash back on all purchases and 0.5% interest on your balance. Apart from that, there are also no account fees, roundups, and access to credit building for $10/m.

The Essential account costs $4 per month (or $48 annually) and offers the same 1% cash back for groceries, bills, services, eating, and drinking but a 0.25% back on all other purchases.

However, there’s a bigger 1.5% interest on your account balance and access to credit building for less – $7/m.

Upgrading to the Premium account and card gets you a bigger 2% cash back on transportation, groceries, and restaurants and 0.5% on all else.

Additionally, there’s a 1.2% interest rate on your balance, no fx fees, and one free international ATM withdrawal per month.

In addition to regular cards and accounts, there’s the KOHO Credit Builder, an optional service that helps build up your credit score. You can subscribe to this service for $7 or $10 per month, depending on your account.

KOHO sends your reports to the three major credit bureaus as you make or fault to make repayments each month.

Lastly, there are four different card designs:

- Sunkissed Skinny Dip,

- Frozen Cherry Soda,

- Gilded Cotton Candy,

- Bluberried Caviar,

- A premium card design

The company also sometimes offers limited edition KOHO metal cards.

READ ALSO: The Rising Problem of Gift Card Scams (How to Avoid)

EQ Bank

EQ Bank offers many savings and investing account types. There are, however, no checking accounts, no debit cards, or ATM withdrawals.

Savings Plus Account earns a 2.50% interest, which is higher than most banks in Canada. It also doesn’t have any monthly fees or minimum balance. Customers enjoy free bill payments, Interac e-Transfers, electronic fund transfers, and EQ to EQ transfers.

The Joint Savings Plus Account account has the same benefits as the Savings Plus Account, but you can have up to 3 other people. You can deposit a maximum of $500,000 at no fee. All the deposits are also CDIC insured, making your money safe.

The Tax-Free Savings Account (TFSA) enables customers to earn interest without paying any extra tax. The interest is at 2.50% at no fee. With this account, you can access the funds at any time without paying any penalties.

In addition, you can also link your account to the primary savings account or an external one.

Next, there’s a US dollar account that earns a 2.00% interest. It has a competitive exchange rate, making it easier to send dollars abroad.

There are registered and unregistered GIC options available. You can start investing in GICs with EQ Bank for as little as $100. As long as you have funds in your Savings Plus Account, you can buy GICs in seconds.

EQ Bank also offers a Mortgage Marketplace for customers to access over 2,000 mortgage products available in the market. Customers can get and compare the best rates offered by Canadian lenders just by checking the app.

EQ Bank also enables customers to send and receive money with Wise. You can transfer funds to your family abroad, which is processed within three business days. Through this partnership, customers also get the mid-market exchange rate.

Credibility & Security

KOHO

Although KOHO is a fintech company and it isn’t CDIC insured, it doesn’t mean the funds aren’t safe. On the contrary, ALL your deposits would be returned to you in case the company goes bust, not just the $100,000.

It’s because all the funds are purposely kept with Peoples Trust Company, where they aren’t being used for anything else but their intended purpose. That’s in complete opposite of what traditional banks do with your funds (i.e., invest it in other ventures that could fail).

READ NEXT: How to Deposit a Check for Someone Else (Surprisingly Easy)

EQ Bank

We already know that EQ Bank is owned by a very old and established traditional bank. It’s also a member of the CDIC, giving up to $100,000 insurance per every account you have in the bank, including joint accounts.

Business Accounts

KOHO doesn’t have a business account on offer yet and it’s not known whether they’ll start offering them in the future.

EQ Bank is the same. If you’re interested in a business account, Equitable Bank offers all sorts.

Customer Reviews

KOHO

KOHO has excellent scores of 4.8/5 on the App Store and 4.6/5 on the Google Play Store. Yet, on Trustpilot, things look a bit different, with a score of 1.6/5 from 100+ reviews.

Clients mostly aren’t satisfied with the bad customer service and have had their accounts locked.

EQ Bank

EQ Bank has a 4.7/5 star rating on the App Store and only a 2.9/5 star rating on Google Store. On Trustpilot, there are only 24 reviews giving the bank a score of 3.5/5.

READ NEXT: 6 Ways to Buy Now Pay Later on Amazon (Up to 18 Months)

Why You Should Choose KOHO

Let’s take a look at some of the reasons why you should choose KOHO.

Debit Card

KOHO provides a visa card that customers can use to withdraw cash at the ATM and to pay for products and services. The card also comes with rewards such as cash backs. In addition, the company also just introduced KOHO metal cards, which customers can order via the app.

Credit Builder

If you don’t have a good credit score, KOHO is the best choice. Customers can rebuild their credit score for only $7 per month. You’ll need to subscribe to the service by having $7 in your spendable account each month to get started.

Mobile App

The KOHO mobile app is one of the highest-rated in Canada, with excellent ratings on the App Store and Google Play. It has one of the best mobile apps with a well-functioning interface.

New users can sign up for an account via the app in five minutes. Once you get onboarded, you can also access all your accounts and transactions on the go.

Premium Benefits

Apart from the free account, KOHO also has a premium account. Although uses have to pay $84 annual or $9/month, there are benefits such as 2% cash back on transportation, groceries, and restaurants.

Why You Should Choose EQ Bank

Here are some of the reasons why you should choose EQ Bank.

High-Interest Savings Accounts

EQ Bank is the best bank if you want to save your money. They offer competitive interest rates at 2.5% on their Savings Plus, TFSA, and Joint Savings accounts. This rate is more than other digital banks in Canada.

Security

EQ Bank is backed by Equitable Bank, which has over 50 years of experience. The bank also has multiple security layers and fraud monitoring features in place.

In addition, all the deposits are CDIC-insured; therefore, customer money is safe. This, combined with their years of experience, is ideal for customers looking for a bank that provides safety.

Financial Services

Apart from the high-interest savings accounts, EQ Bank offers its customers GICs to earn more from investments.

Conclusion

Although built for different audiences, both KOHO and EQ Bank offer digital bank accounts you can count on.

KOHO has the best of both world and is geared towards the younger crowds. EQ is looking to expand your existing money with market-leading savings rates and products for every stage of your life.

Because of that, it really isn’t hard to choose between the two. It all comes down to your needs.