Last Updated on November 21, 2022 by TMB

KOHO and Tangerine are both popular for their financial products with no monthly fees or minimum balance. As some of the best digital banks in Canada, how different are they? All that, and more, after this short verdict.

Although both KOHO and Tangerine are digital banks, they are quite different and will appeal to different types of people. KOHO offers a simple account that will suffice for most folks. Tangerine offers a full suite of financial products and will appeal to those looking for a traditional bank but without the traditional fees.

Let’s dive a bit deeper and see the reasons for choosing KOHO or Tangerine.

About KOHO

KOHO is a Canadian fintech company founded in 2014 and headquartered in Toronto, Ontario. While it is not exactly a bank, the company offers a variety of innovative financial products to help Canadians build their financial lives and save money.

The company’s belief is rooted in providing better financial solutions for all Canadians. They offer secure accounts and debit cards via a partnership with Visa and People Trust Company, a partner bank that holds the funds.

They are also backed by established investors like TTV Capital, Drive Capital, Power Group, and Portag3.

How to Open a KOHO Account

Opening a KOHO account is easy. All you have to do is head to Koho.ca, enter your email and a password, review the accounts they offer and choose the one you want. Provide all the necessary details, and you can be done in five minutes.

READ ALSO: KOHO Vs. EQ Bank (The 7 Key Differences)

About Tangerine

Tangerine is one of the most popular online banks in Canada and a subsidiary of Scotiabank. This bank was launched in April 1997 as ING DIRECT. In 2012, ING Bank of Canada was acquired by Scotiabank, and the bank changed its name to Tangerine.

The bank’s mission was to offer an alternative to traditional banking by providing safe, secure, and innovative banking systems.

Today, Tangerine is one of the leading banks in Canada, which offers a simplified and innovative way of banking. They don’t charge exorbitant fees like traditional banks and offer sign-on bonuses.

How to Open a Tangerine Account

As is the case with KOHO, you can open an account online or by downloading the app. Simply choose ‘Sign up digitally’ and:

- Scan your Canadian Driver’s Licence

- Take a selfie

- Enter additional information

- Give your digital signature

If you don’t have a driver’s license, any of the following will do:

- Canadian Passport

- Provincial or Territorial Photo ID Card

- Canadian Secure Certificate of Indian Status

- Canadian Permanent Resident Card

- Quebec Health Card with picture and signature

Pros & Cons

Pros

| KOHO | Tangerine |

| Early payroll | Wide range of accounts |

| Budgeting tools | Many options for savings accounts |

| A choice of different card designs | Credit cards are available with perks |

| Cashback | Options for investment portfolios are available for any level of investor |

| Credit builder | Mortgage and loan services with good interest rates |

| Free ATM withdrawals |

Cons

| KOHO | Tangerine |

| Unresponsive customer support | Interest rates vary |

| Expensive metal card | Overdraft fees can add up if you aren’t in the opt-in overdraft protection program |

| Deposits aren’t CDIC insured | Investment portfolios are hands-off for the customer, so if you like to be involved, this may not be right for you |

Accounts & Cards

KOHO

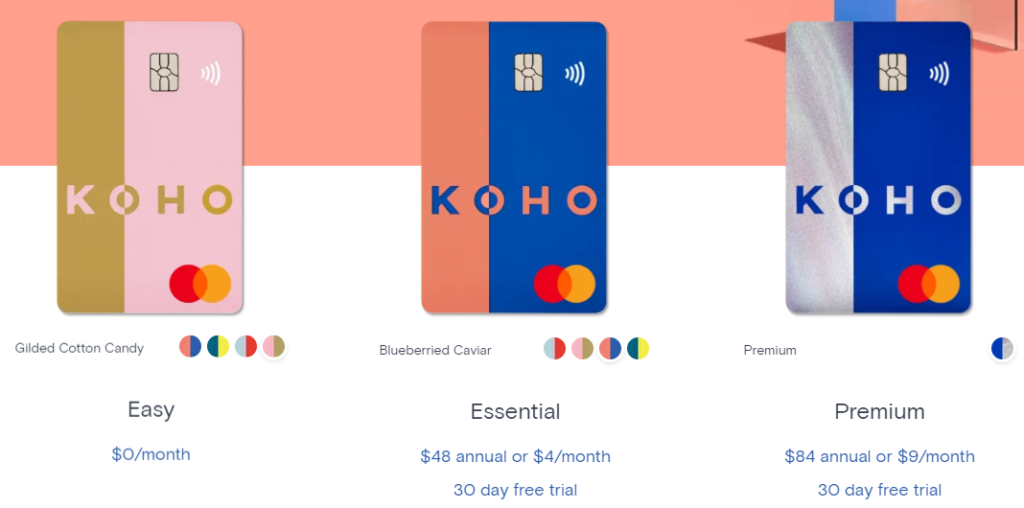

There are three different account types:

- Easy (free)

- Essential ($4/m)

- Premium ($$9/m)

Differences between the accounts are mainly in the percentage of cashback you’re getting, as well as how much interest you’re earning.

The free account nets you 1% cash back on all purchases, 0.5% interest on your balance, no account fees, roundups, and access to credit building for $10/m.

The Essential account offers 1% cash back for groceries, bills, services, eating, and drinking and 0.25% back on all other purchases. Plus, a 1.5% interest on the entire balance and credit building for $7/m.

If you upgrade to a premium card, you get 2% cash back on transportation, groceries, restaurants, financial coaching, 0.5% on everything else, 1.2% interest, no fx fees, and one free international ATM withdrawal per month.

KOHO Credit Builder is an optional service that helps you build your credit history. You can subscribe to this service and ensure that your spending account has the amount needed for repayment every month. KOHO also sends your reports to the three major credit bureaus.

There are four different card designs that, include Sunkissed Skinny Dip, Frozen Cherry Soda, Gilded Cotton Candy, and Bluberried Caviar, as well as one card design reserved for premium accounts.

The company also offers unique KOHO metal cards.

Tangerine

Tangerine’s chequing account earns a 0.10% interest. There are no fees for daily transactions, and customers can enjoy free Interac e-Transfer transactions.

Once you sign up for this account, you also have access to 3,500 ABMs and a network of Scotiabank ATMs across the globe.

If you are more into savings, the Tangerine free savings account pays 0.10% interest. It is also available for TFSA, RRSP, and RRIF plans.

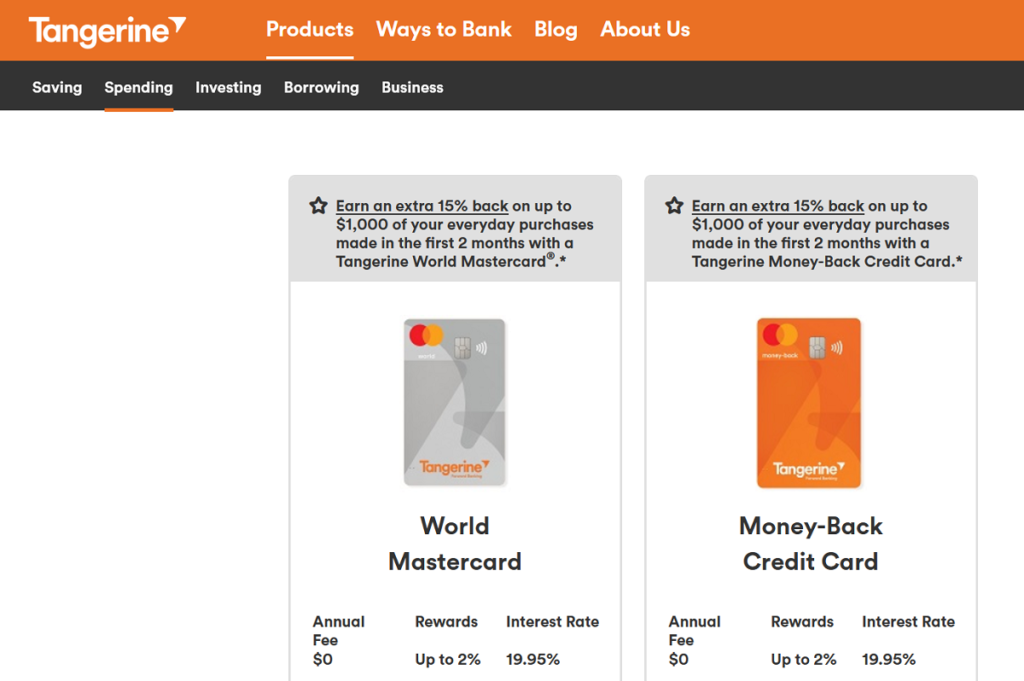

The Tangerine credit cards, Tangerine Money-Back Credit Card, and World Mastercard have cash back rewards of 2%.

Customers can earn Money-Back Rewards on all everyday purchases. In addition, the cards have no annual fees making them ideal for paying bills and making purchases.

Tangerine is ideal for people who want to invest. Some of the funds available are the non-Registered Investment Fund, Tax-Free Investment Fund, RSP Investment Fund, and RIF Investment Fund.

If you want a mortgage, Tangerine offers a great rate and flexible payment options. They have a dedicated account manager to guide you through the best alternatives.

The bank often runs promotions where you can earn 20% cash back for two months, and 4.50% interest in the savings account for 5 months.

READ NEXT: 6 Best Digital Banks in Canada (Digital Banking in Canada)

Credibility & Security

KOHO

As is the case with all digital banks that don’t hold a banking license, the funds you deposit into the account aren’t insured by the Canada Deposit Insurance Corporation (CDIC).

However, your funds will be returned to you by the partnering bank that actually holds your funds – Peoples Trust Company.

Tangerine

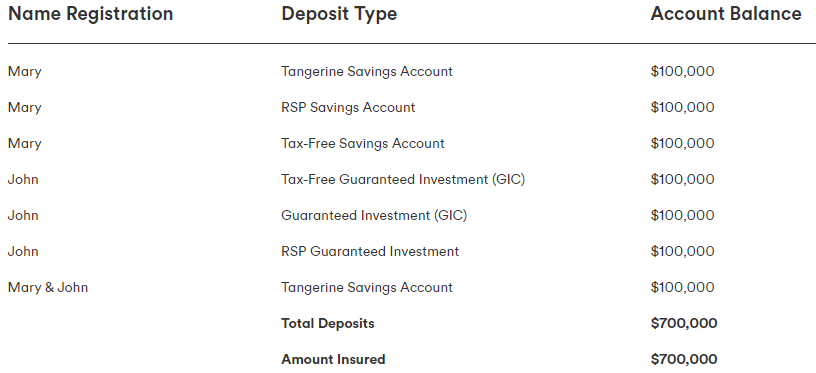

As we already mentioned, Tangerine is a subsidiary of the Bank of Nova Scotia and a CDIC member because it has a banking license. So what does that mean to you and your money?

It means that your deposits are insured for up to $100,000 per category or type of account.

Additionally, Scotiabank is one of Canada’s Big Five banks and the third-largest Canadian bank by deposits and market capitalization.

Savings Accounts

KOHO

KOHO doesn’t have a separate savings account. However, you can still earn interest, even on the free account plan. The free account gives you a 0.5% rate, Essential 1.5%, and Premium, for some reason, only 1.2%.

There are also features like round-ups that save your spare change at each purchase, savings goals, Spendables (suggested amount you have available to spend), and more.

Tangerine

Tangerine, on the other hand, has five different savings account types:

- Savings Account

- Tax-Free Savings Account

- RSP Savings Account

- RIF Savings Account

- US$ Savings Account

The regular savings account offers only 1.00% but without fees and no minimum balance.

The Tax-Free Savings Account (TFSA) has the same rate of 1.00%, but you won’t be taxed on the interest earned or on withdrawals as long as you’re within contribution limits ($6,000/year).

The Retirement Savings Plan (RSP) comes with an interest rate of 1.00% as well and lets you move your money at any time to other investment choices. This account is different from the TFSA because it is not tax-free but rather tax-deferred.

Next, the Retirement Income Fund (RIF) Savings Account lets you draw the retirement income you need while having the benefits of the regular Savings Account. The interest rate is just a little bit higher at 1.05% and is tax-sheltered.

And lastly, the US Dollar Savings Account lets you save your US funds at an interest rate of (only) 0.10%.

Business Accounts

KOHO doesn’t have a business account, and it isn’t known whether they’ll even offer one in the future.

Tangerine offers business savings accounts with no fees and good savings interest rates. There are four types of Tangerine business accounts:

- Business Savings

- Business US$ Savings Account

- Business Guaranteed Investment

- Business US$ Guaranteed Investment

The Business Savings account complements your existing business chequing account with a fantastic interest rate of up to 2.50%. From $0 – $100k, the rate is 2%, $100k-$500k, 2.25%, and $500k+, it’s 2.5%

The US Dollar Business Savings Account has an interest rate of 1.60% and two prerequisites:

- You need a Tangerine Business Savings Account

- You need a US dollar business chequing account at another financial institution

The Business Guaranteed Investment (GIC) account offers savings rates from 1.50% to 5.10%.

And lastly, the US Dollar Business Guaranteed Investment (GIC) account has the same prerequisites as the other US$ Savings Accounts and offers rates from 1.50% to 4.75%.

Investing

Again, KOHO doesn’t have any investing options. On the other side, Tangerine has varied investment options:

- Non-Registered Investment

- Core Portfolios

- Global ETF Portfolios

- Socially Responsible Global Portfolios

Core Portfolios, for instance, have five types of portfolios as well, depending on the type of ETFs, bonds, or stocks they’re investing in.

Customer Reviews

KOHO

KOHO has a great score of 4.8/5 on the App Store and 4.6/5 on the Google Play Store. However, on Trustpilot, things aren’t looking that great, with a score of 1.6/5 from 100 or so reviews.

People mostly complain about bad customer service experiences and locked accounts.

Tangerine

Tangerine also has great scores of 4.7/5 on the App Store and 4.5/5 on the Google Play Store. On Trustpilot, the bank has an appalling score of 1.2/5 from more than 1,000 reviews.

The complaints cover bad customer service, long wait times, and closed accounts.

Why You Should Choose KOHO

Here are the reasons why you should choose KOHO for your bank.

High-Interest Rate

KOHO offers a hybrid account with up to a 1.5% interest rate on the entire account. This is among the highest interest rate on a savings account among the top banks in Canada. If you are saving up some cash, you can grow your savings much faster.

Credit Builder Feature

KOHO lets you rebuild your credit score for only $7 per month. If your credit score is poor, you’ll just need to subscribe to this feature by ensuring that there’s $7 in your spendable account each month.

Mobile Application

As a digital bank, KOHO has one of the best mobile apps. The banking application gives you access to all your accounts, and you can easily track all your transactions from anywhere.

Why You Should Choose Tangerine

Tangerine has the best of traditional banking and digital features. Here are some of the benefits.

Variety of Financial Products

Tangerine is a digital bank with a wide array of banking services and products. Apart from the typical chequing and savings accounts, Tangerine also has credit cards, tax-free savings accounts, GICs, mortgages, business accounts, and investment funds. That’s way more features than other digital banks.

Credit Cards

The Tangerine Money-Back Credit Card and World Mastercard offer cash back rewards of 2%. What’s more, the cards have no annual fees.

Investment Options

Tangerine helps its customers to build their future by providing investment options. They have core portfolios and global ETF portfolios that customers can sign up for and grow their money.

Conclusion

KOHO and Tangerine have similar features that define a modern-day digital bank account, however, customers will appreciate KOHO for their hybrid account with no fees and a high-interest rate.

On the other hand, Tangerine is an excellent option for a digital bank with no fees, competitive interest rates, and a high-quality and wide range of financial services and products. It’s a perfect mix of traditional and digital banking systems.