Ally Bank is a popular digital bank that offers a wide range of financial products.

Although it has millions of customers, it does have some shortcomings.

For that reason, I have compiled a list of Ally Bank alternatives that offer excellent digital banking services.

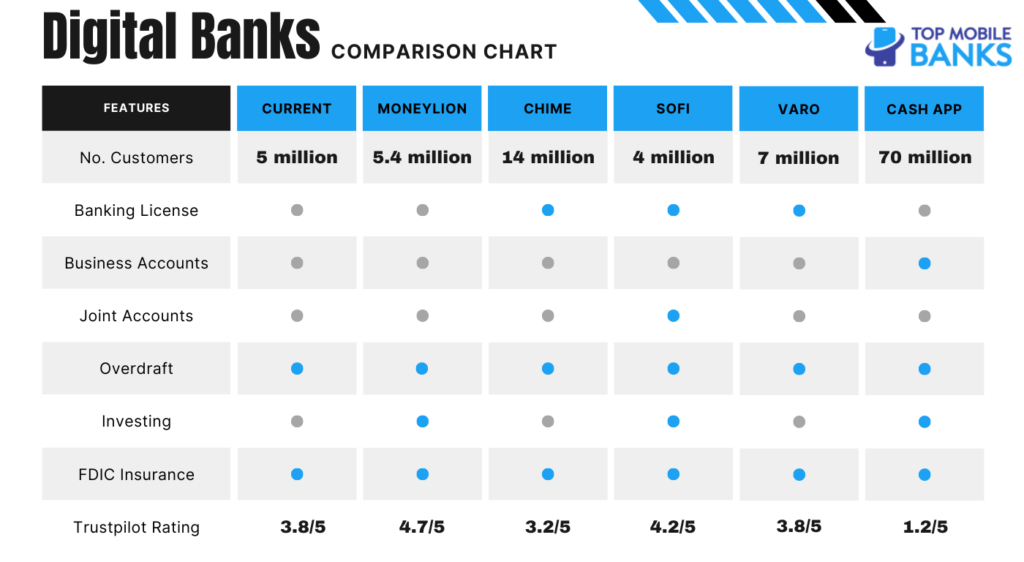

Here is table with Ally bank alternatives for your convenience.

[lasso rel=”pxf” id=”10713″]

1. MoneyLion

| What’s similar to Ally | What’s different from Ally |

|---|---|

| No minimum balance | Cash advances up to $250 |

| No ATM fees | Charges out-of-network ATM fees |

| No overdraft fees | Credit builder program |

| Excellent savings rates | Cashback and rewards on the debit card |

| Early payday | Real crypto investing |

| Price protection |

MoneyLion is a great alternative to Ally. It was founded almost ten years ago and offers great value for money as it charges a nominal fee of $1 per month to access its mostly fee-free service.

Its flagship product is the RoarMoney checking account which is similar to Ally’s but offers cashback rewards directly on the debit card, which might appeal to some people.

Some of their digital-only bank programs have other costs, like the Credit Builder Plus ($19.99/month), but MoneyLion also gives you opportunities to recoup the monthly fee. With this program, you basically apply for a loan of up to $1,000.

Once they approve your loan, you can access a portion of the money immediately. You build credit with monthly loan payments over the next year.

When you’re applying, the company doesn’t do a hard credit check that can affect your credit score.

If you’re able to make a direct deposit of $1,000 or more every month, you can get access to MoneyLion’s safety net that includes cash advances of up to $250 without interest.

Like Ally, it offers many investment products. However, unlike Ally, it also offers a crypto-investing platform.

2. Revolut

| What’s similar to Ally | What’s different from Ally |

|---|---|

| No minimum balance | Business accounts |

| Early payday | Rewards and discounts on the debit card |

| Interest on savings | No financing or financial instruments |

| No ATM fees | Kids accounts |

| Real crypto investing | |

| Personalized cards |

Revolut is one of the most used challenger banks in the world. The app has more than 25+ million users and was launched in the US in 2020.

It’s also a so-called financial super app that offers more perks and benefits than most other digital banks. You will have to opt for a paid account to access most of them.

In the US, there are three account types:

- Standard (free)

- Premium ($9.99/m)

- Metal ($16.99/m)

All three accounts offer the following:

- Fee-free ATM withdrawals at more than 55,000 ATMs,

- Personalized cards,

- 10 fee-free international transfers per month,

- Unlimited disposable virtual cards,

- Interest on savings,

- Commission-free stock and crypto trading,

- International spending at market leading exchange rates

- Kids account(s)

The Metal account is notable for its exclusive 18G solid steel metal card, one of the first on the market.

All in all, you really can’t go wrong by choosing Revolut.

3. SoFi

| What’s similar to Ally | What’s different from Ally |

|---|---|

| No minimum balance | SoFi at Work |

| No ATM fees | Insurance products |

| No overdraft fees | Student loans and refinancing |

| Excellent savings rates | Referral program |

| Early payday | Career coaching |

| A wide variety of financial products | Estate planning |

| Signup bonus |

SoFi is another excellent alternative to Ally as it offers a wide range of financial products, even more so than Ally.

This fintech was granted a conditional national banking license and for that reason, your funds of up to $250,000 in your checking and savings accounts are FDIC insured.

The bank offers everything from checking and savings accounts to personal and student loans, mortgages, refinancing, credit cards, and insurance. It’s basically your one-stop shop for all things finance.

The no-fee online bank account offers a high APY of up to 3.25% and comes with no overdraft fees and a cash bonus of up to $250, depending on how high your direct deposits are.

To clarify, the checking account has an APY of 2.50%, and the savings account and Vaults come with a 3.25% APY. However, you can keep all your funds in the savings account if you want and the funds needed for paying bills, for example, will be automatically moved to the checking account to cover the amount.

READ ALSO: 5 Possible Reasons Why Your Zelle Transfer Failed (Resolved)

4. Current

| What’s similar to Ally | What’s different from Ally |

|---|---|

| No minimum balance | A teen checking account |

| No ATM fees | Account maximum ($10,000) |

| No overdraft fees | Cash deposits with a fee |

| Excellent savings rates | Cashback offers and discounts on the debit card |

| Early payday | Instant gas hold refunds |

Current was launched in 2015 as a mobile-only digital bank founded in the United States by Stuart Sopp.

Like many others, it isn’t a bank but a fintech company. It has however partnered with Choice Financial Group, Member FDIC, so your money is insured and safe.

For those who want high-value accounts, Current might prove disappointing. The maximum account balance is “only” $10,000.

Current sets itself apart from many online banks like Ally with its teen banking option. It’s free to set up a checking account for your teenager(s) to help them learn to manage money and get paid for things like chores and odd jobs.

The instant gas hold refund is a handy feature Current offers its members. Gas stations often put a hold on your debit card for much more than the amount of gas you end up purchasing.

Instead of a hold locking up the extra $10-$50 for a few days, Current immediately releases the amount beyond your gas purchase.

The Current checking account is free, just like Ally and while some challenger banks don’t even have cash depositing options available, Current allows cash deposits but charges $3.50 per deposit.

On the other side, it has one of the highest APY on the market – 4.00%. This will help you stretch your money further.

5. Chime

| What’s similar to Ally | What’s different from Ally |

|---|---|

| No monthly maintenance fees | Checking account doesn’t earn interest |

| Easy online sign-up | Charges out-of-network ATM fees |

| No overdraft fees | No foreign transaction fees |

| No minimum balance requirements | Offers cash deposit options in limited locations |

| Early payday | Limited customer service, unlike Ally’s 24/7 support |

Chime was founded in San Francisco in 2013 to help people from all walks of life open a bank account no matter what kind of money problems they’ve had.

Their philosophy is that any adult should be able to get an account with almost no paperwork.

Just like Ally, Chime is a digital-only bank; however, it offers a simplified product offering that should ultimately be more than enough for most people.

Although there are no loans or investments, for example, there is a solid checking and savings account, additional tools to help you manage money, and desktop and mobile access to your accounts.

The round-up savings feature is one of the most beneficial features Chime offers, particularly for people who struggle to save money. The account will automatically round withdrawals to the next dollar, leaving a surplus to build over time.

There’s also an interest rate of 2.00% that’s well above that of traditional banks, as well as 60,000 fee-free ATMs, and cash deposits at over 90,000 retail locations.

People that want to improve their low credit score can avail of the company’s credit builder program.

You can open an account if you’re at least 18 years old. Chime believes in “Second Chance Banking,” so they don’t use ChexSystems or other checking verification services.

In conclusion, anyone who can’t get a checking account at other institutions because of past financial problems should definitely look into Chime as an excellent alternative to Ally.

RELATED: Chime Vs. Aspiration (Choosing a Digital Banking App)

6. Varo

| What’s similar to Ally | What’s different from Ally |

|---|---|

| No minimum balance | First digital bank to be licensed as a full bank |

| No ATM fees | Charges out-of-network ATM fees |

| No overdraft fees | Credit builder program |

| Excellent savings rates | Cashback and rewards on the debit card |

| Early payday | Up to $100 cash advance on qualifying accounts |

| No investments, financial instruments, or financing |

Varo is the first digital bank in the United States that was granted full bank status. The bank was founded by Colin Walsh and Kolya Klymenko in California in 2015. Varo got the coveted license and bank charter in 2020. Before that, it was operating as a fintech company.

Like Ally, Varo Bank is a direct Member of FDIC, so all deposits up to $250,000 are insured.

This digital bank also doesn’t run account information through ChexSystems or run a credit check on applicants. They are firm believers in “Second Chance Banking” for those who’ve had financial issues that make getting a bank account difficult.

They offer helpful programs for people who encounter money problems while banking with them.

You can get up to $100 advanced if you meet account history and balance requirements to help when money needs to stretch to the next paycheck.

Varo has also launched a credit builder program that helps you build your credit. Simply add money to your so-called Varo Vault and set a spending limit. Once you make on-time payments, Varo reports them to the credit bureaus.

These on-time payments help you build new credit or bounce back from a bad credit history.

7. Axos Bank

| What’s similar to Ally | What’s different from Ally |

|---|---|

| No minimum balance | $50 minimum deposit on some checking accounts |

| No ATM fees | $250 minimum deposit on high-yield savings |

| No overdraft fees | No fee cash deposit |

| Early payday | Special accounts for world travelers and international access |

| A wide variety of financial products | Much lower savings rates |

Axos Bank is the most similar to Ally Bank out of all the digital banks on our list. That may or may not be a good thing for you.

This fully-fledged national digital bank has a similar structure and similar financial products. However, it also offers business accounts to small businesses but also offers commercial banking services.

The bank was founded more than 20 years ago by Jerry Englert and Gary Lewis Evans and is one of the oldest online banks.

Axos offers three checking accounts:

- Essential Checking

- Rewards Checking

- Cashback Checking

The Essential Checking account is suitable for direct deposits and comes without fees, just like the other two accounts.

The Rewards account is aimed towards those with high account balances because it has a 1.25% APY.

And lastly, the Cashback account is suited for people that frequently use their debit cards as it offers 1.00% cash back.

Axos Bank’s High Yield Money Market and High Yield Savings account can’t really hold a candle to Ally Bank’s 3% APY savings account.

Namely, it only offers savings rates of 0.61% APY for Savings and 0.25% for Money Market accounts.

8. Cash App

| What’s similar to Ally | What’s different from Ally |

|---|---|

| No minimum balance | No savings accounts |

| No ATM fees | Rewards and discounts on the debit card |

| No overdraft fees | Spending and withdrawal limits |

| Early payday | Tax filing |

| Real crypto investing | |

| No financing or financial instruments |

Cash App was founded almost ten years ago by well-known Jack Dorsey and his friend and entrepreneur Jim McKelvey. Although it works like many other digital banks in that it’s a fintech company, Cash App is actually considered a mobile payment platform.

It appeals to people who want a no-frills spending account and an inexpensive way to receive and make transfers and payments.

Although Cash App isn’t a bank, it partnered with Member FDIC banks to hold your funds, and therefore, your money is indeed insured up to $250,000.

Cash App offers you instant payments to anyone, a free debit card, free ATM withdrawals, free tax filing, and an easy way to buy and sell stocks and even Bitcoin.

It doesn’t offer credit cards, savings accounts, or other financial products. It’s also worth noting that the app already has more than 14 million users in the US and the UK.