Last Updated on September 14, 2022 by TMB

There are many types of bank cards, and each one has a purpose and a place in the banking and financial space. Here are all the bank card types on the market today.

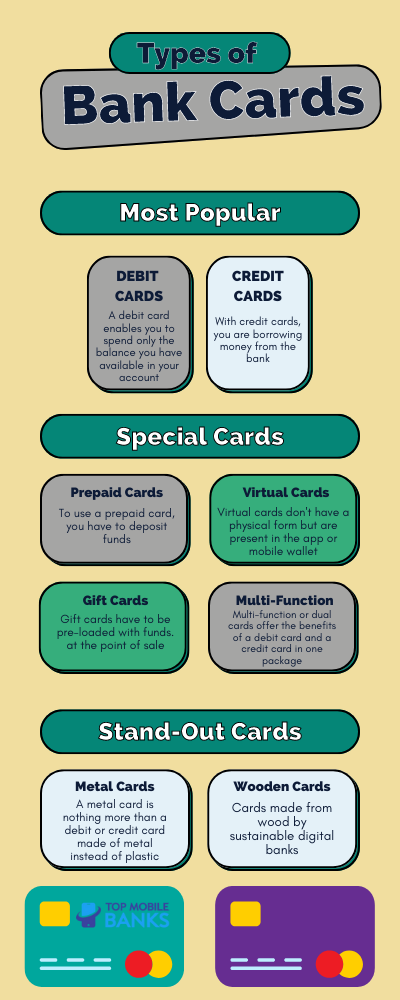

Debit Cards

Debit cards are one of the simplest forms of bank cards. They are the default type of card when you open a checking account. A debit card enables you to spend only the balance you have available in your account.

They are issued by a bank and are co-branded with a card network such as Visa or Mastercard.

You can use them to spend money online or in-store, pay bills, as well as withdraw and deposit cash to your account via an ATM. The amount you spend is immediately taken from your balance and put on hold, but the actual money could take days to come off your account.

They are very versatile and often don’t have an annual fee. Most digital banks offer debit cards with no monthly fee as part of their account.

Debit cards also have no fees when using an ATM (depending on the bank or card issuer) or when you use them to purchase something. The card issuer and your bank charge the merchant or retailer, and not you, and split the fee between them.

Unlike credit cards, you also don’t have to pay interest on what you spend. They are a great choice to keep you from going into debt because you can’t spend more than you have in your account.

You should be aware that some banks allow you to go into overdraft (negative balance). If you intentionally or by accident go into overdraft, you could be paying around $35 (in the US) per transaction.

That means that in a single day, you could rack up a couple of hundred dollars in expenses if you go about your day unaware that you’re in a negative balance.

By using only debit cards, you also aren’t building up your credit score, at least in the US.

READ ALSO: 6 Reasons Why Buy Now, Pay Later Services Ar So Popular

Credit Cards (12 Types)

Credit cards are extremely popular type of cards because to use them, you don’t actually have to have any money in your bank account. The purchase amount gets deducted from your line of credit.

This is the biggest difference between debit cards and credit cards. In the US, credit cards are as common as apple pies or hot dogs. However, worldwide, people aren’t that dependent on credit cards and often never get one.

With credit cards, you are basically borrowing money from the bank. The money you spend has to be repaid on the date and under the conditions agreed with the card issuer (bank, credit union…).

You can choose to pay that amount in full inside the deadline that was set. In that case, you won’t have to pay any interest. This is the optimal usage of credit cards where you get all the benefits at a minimum or even no additional cost to you.

If you only pay a partial amount, you will have to pay interest. According to the Federal Reserve’s data from the end of 2021, the average interest rate is 14.51%.

Interest rates depend on your credit score. When you’re signing up for a credit card, you can see the proposed interest rate that you will have to pay.

For example, if you have a bad credit score of 579 or worse, you could get offered an interest rate of around 25%, which is very, very bad and could get you into debt you won’t be able to get out of.

On the other side, someone with a score of 720 or higher would get an average interest rate of 17%.

There are many types of credit cards:

- Business credit cards

- Student credit cards

- Secured credit cards

- Cash back credit cards

- Travel credit cards

- Rewards credit cards

- Balance transfer credit cards

- Revolving credit cards

- Co-branded credit cards

- Zero percent APR credit cards

- Store credit cards

- Crypto credit cards

As you can see, most credit cards bring something to the table. It could be travel miles, more cash back, rewards, or revolving credit.

There are also new types of cards that support cryptocurrency. They can be debit, credit, or prepaid cards. You can use them to spend your crypto in-store or online, just like you would with a normal card.

READ ALSO: 6 Ways Insurtech is Different from Traditional Insurance

Prepaid Cards

Prepaid cards are more similar to debit cards than they are to credit cards. To use a prepaid card, you have to deposit funds, often manually. Until the funds are added or after they are spent, the card is unusable. They are not to be confused with gift cards.

Although they look similar to debit and credit cards, in the sense that they have a card number and expiration date printed on them, they usually aren’t connected to a bank account.

For that reason, you can easily buy them in stores or order them online without worrying about your credit score or other eligibility requirements.

Prepaid cards are notorious for having excessive fees associated with them, including activation, reloading, withdrawals, purchases, etc. Some merchants also don’t accept them, so it’s better to read the reviews online before getting one.

They are valid until the end of the expiration date printed on the card and can be reloaded as many times as you want.

People usually use them for their everyday purchases but are also used by those that, for some reason, can’t open a proper bank account, and therefore as an alternative to keeping cash under the mattress.

Virtual Cards

Virtual cards are a relatively new product and are mostly associated with digital banks. They have all the characteristics of normal debit or credit cards, such as card number, expiration date, and CVV, yet they are only digital and don’t have a physical form.

Nowadays, there are many banks, digital or traditional, that issue them. Some virtual cards are disposable and can be used for one purchase only, while others have a normal expiration date of five years.

They are typically used with mobile wallets such as Apple, Google, and Samsung Pay so that they can be used online or in-store. However, the card information can also be manually typed into the online form to pay for goods and services.

Some banks issue a virtual card for free, but they charge for a physical debit card. That way, by adding the virtual card to your payment wallet, you can save some money.

Other use cases include paying with a disposable virtual card when you don’t trust an online merchant, but you still want to buy from them. That way, if your card details are shared with a third party, the card will be non-existent, and your money can’t be stolen.

Some subscriptions can also be hard to cancel, or the company in question is notorious for charging money even after you cancel your membership. In these cases, a virtual card can be of help as well.

Gift Cards

Gift cards are also popular and are issued by card companies and are often co-branded with a retailer, merchant, or financial company. Examples would be Amazon or Walmart gift cards, Playstation or Xbox Store gift cards, iTunes and Steam gift cards, etc.

Gift cards have to be pre-loaded with funds. That’s done at the point of sale, as you can’t reload them any further in the future. Unlike prepaid cards, what you load the first time onto the card is final. They also have a much shorter use-by date.

There are two types of gift cards:

- Closed loop

- Open loop

Closed loop gift cards are the ones we mentioned above. They are tied to a certain store or brand and can’t be used anywhere else.

Open loop gift cards are newer and are issued by major card issuers like Visa, Mastercard, and American Express and can be used almost anywhere. However, just as is the case with prepaid cards, there are some exceptions to this rule.

Gift cards are widespread and are usually, as their name says, gifted to family members or friends, but also to employees by their companies.

READ NEXT: 7 Virtual Banking Assistants in the US Banks (What Are They?)

Multi-Function Cards

A debit card can be used to solely spend the money in your bank account. A credit card allows you to spend money you don’t have from a credit approved by your bank or financial institution.

Multi-function or dual cards offer the benefits of a debit card and a credit card in one package. You can choose which function you can use when you want to use it.

These types of cards aren’t as common. In fact, I’m yet to meet a person that has one.

Fifth Third Bank was the first card issuer in the US to offer a combined credit and debit card. It was called Duo Card and was introduced in 2011.

A dual card would be appealing to people that don’t regularly need a credit card, don’t like carrying an extra card in their wallets, or struggle with debt/credit but still need some flexibility for emergencies.

A digital bank is offering a smart payment card that combines ALL your bank cards into one smart card. The company is called Curve, and its card is available in Europe.

By adding all your cards to this one app and card, you can see all your account balances in one place, quickly switch transactions from one card to another (even retroactively), spend abroad without fees, split payments into installments, and more.

Stand-Out Cards (3 Types)

There are also some card types that fall under some categories mentioned above but are a bit different, nevertheless. Some companies offer them free of charge, but more likely as a part of a paid or premium plan.

Metal Cards

Metal cards have been around for more than 20 years. However, some digital banks, like Revolut, bunq, and KOHO, have popularized them and made them affordable to everyday people.

A metal card is nothing more than a debit or credit card made of metal instead of plastic. Because they usually come only with a premium account, they offer some additional perks, such as more cashback, travel insurance or lounge access, and similar.

Other than that, they mostly exist as a vanity item that you can show off in front of others.

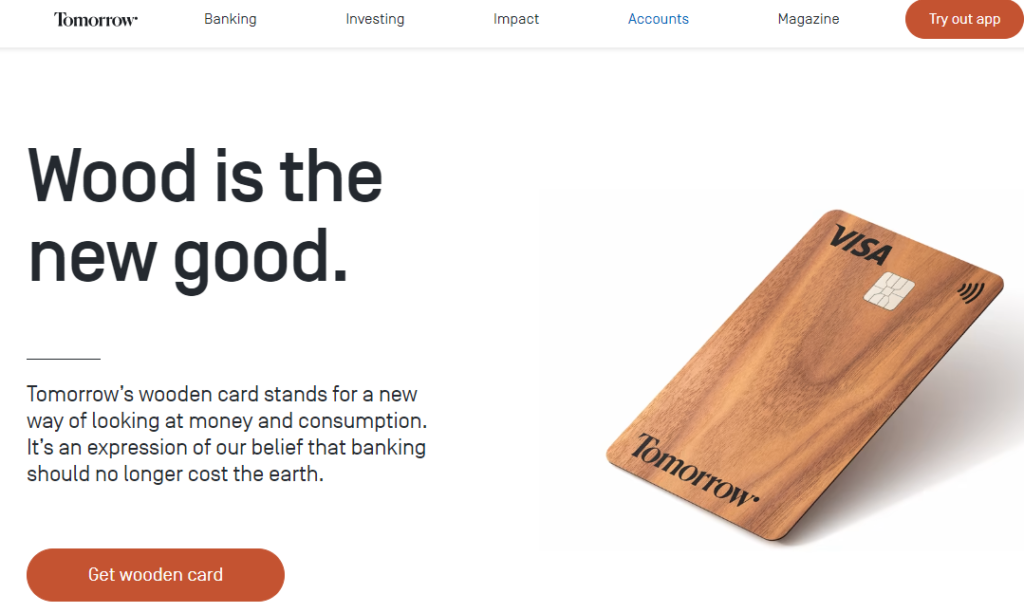

Wooden Cards

On the opposite side of metal cards are bank cards made of wood. That’s right. Digital banks like Treecard and Tomorrow have decided to offer debit cards made of wood. One single sustainably grown cherry tree provides enough wood for 10,000 cards.

The goal is to cut plastic usage but also to offer customers a sustainable account from fintech companies that will invest your deposits into sustainable industries as well as plant trees with every dollar or euro you spend.

Cards Without Numbers

Increasingly, banks are issuing cards without any numbers printed on them. There are no account numbers, no expiration date, no CVV, no name – nothing.

Some banks have moved those to the back of the card for a cleaner look. However, others have opted to move this information to the mobile app. That way, if you need to know these numbers, you can simply open the app and get them.

So, why are banks doing this? Some say it’s for added security, while others do it to give their cards a cleaner look, making more space for an image, for instance, to appeal more to people.

Conclusion

There are quite a few different types of bank cards. The two main and most popular are still debit and credit cards.

Nevertheless, banks and especially fintech-led digital banks, are always on the lookout for the next big thing that will give them an edge.

More Like This

- Keep it Private: How to Pay for OnlyFans Discreetly

- 15 Best Digital Banks and Banking Accounts in the USA

- Can You Get a Chase Debit Card the Same Day? (Workarounds)

- Visa Gift Card to PayPal: Easy Way to Transfer Your Balance

- 3 Ways to Transfer Money From Green Dot Card to Cash App

- 4 Digital Banks With Credit Cards